Minimum prices set for an auction of 700-MHz spectrum in India are so high (two to four times higher than prior auctions) that many of the leading mobile companies will not bid. And, according to Fitch Ratings, the eventual spectrum winners might well regret having won. That “winner’s curse” has happened before, often with 3G spectrum auctions.

India's telecom regulator recommended a reserve price of INR115bn (US$1.7 billion) per MHz for nationwide 700MHz spectrum.

Fitch Ratings “believes that efficiency gains from deploying 4G services on 700MHz will be insufficient to offset the relatively high price.”

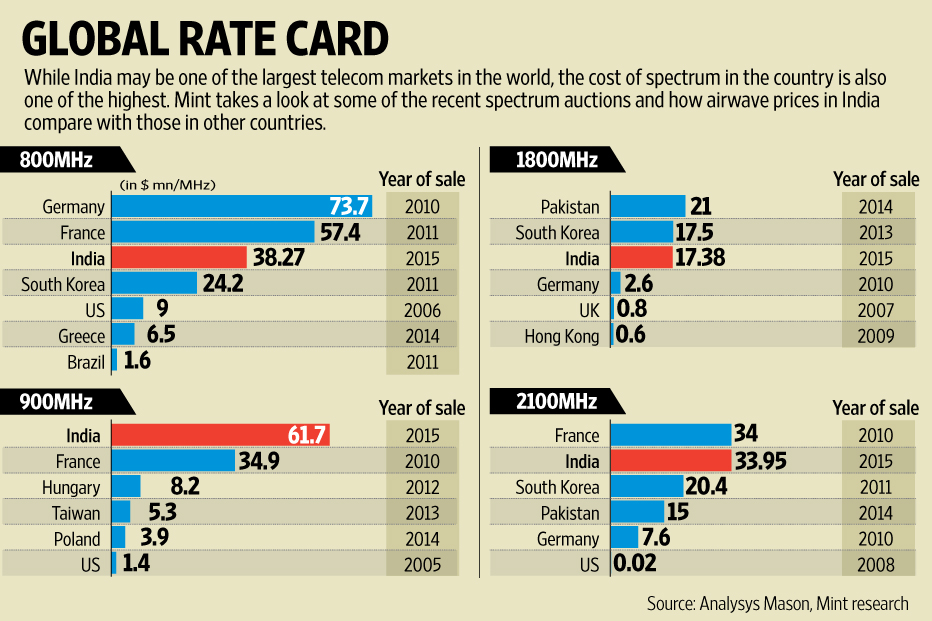

The reserve price is about twice the price set for 800-MHz spectrum, 3.4 times the reserve price for 900-MHz spectrum and four times the minimum prices set for 1.8 GHz spectrum.

Winning therefore “could exert further pressure on participating telcos' balance sheets and cash flow, and limit their ability to invest in capex over the medium term,” say Fitch Ratings analysts.

In fact, the top four telcos, including Bharti Airtel, Vodafone, Idea Cellular and Reliance Communications may hesitate to bid, as balance sheets already are “stretched,” while available cash is expected to become an issue once Reliance Jio enters the mobile market in the spring of 2016.

Instead, the leaders might choose to rely on spectrum they already have acquired. Bharti Airtel will use 900 MHz, 1.8 GHz and 2.3 GHz.

Reliance Jio, after having invested about US$15 billion on spectrum and networks, will use 800MHz and 850MHz spectrum.

Every single cost in any telecommunications or other ecosystem ultimately is paid for by customers or business partners, it goes without saying.

That is true of all infrastructure costs, including the cost of spectrum, which is why many observers favor increased use of shared spectrum and unlicensed spectrum as a way of expanding capabilities while minimizing end user cost.

The cost of licensed spectrum, typically a major expense, now is an issue in India, which is preparing to issue licenses for 700-MHz spectrum. High costs were an issue in earlier spectrum auctions as well.

After a massive auction where incumbents essentially had to pay whatever was required to retain use of frequencies they already were using, “the industry simply does not earn enough to support the bids,” some have argued.

In that spring 2015 auction, India’s mobile companies bid Rs 1,10,000 crore for spectrum across four bands that were substantially above the reserve (minimum) prices.

Buyers paid 1.79 times the reserve price for 800MHz spectrum and 1.95 times the reserve prices for 900 MHz.

Operators paid less of a premium for higher-frequency spectrum, just 1.16 times the reserve price for 1800 MHz spectrum and 1.05 times the minimum for 2100 MHz spectrum.

John Giusti, Chief Regulatory Officer, GSMA, is among observers urging the Indian government to lower minimum prices for the 700-MHz auction.

“The GSMA is very concerned by TRAI’s recommendation to set a starting price of US $1.7 billion per MHz for pan-Indian 700MHz spectrum,” said Giusti.

India has one of the lowest average revenue per user (ARPU) metrics globally (US $2.45 at the end of 2015).

High spectrum costs, combined with limited revenue contribution from data services, new competitive pressures and high capital investments to upgrade to 4G, mean it will be difficult to sustain business models, if high spectrum prices hold, Giusti argued.

“The more mobile operators have to pay for a spectrum licence, the less capital is available to roll out new mobile networks,” Giusti said. “We encourage greater focus on the long-term benefits of connecting more people in India to affordable mobile broadband, rather than on short-term financial gain.”

“High reserve prices and an unrealistic predetermination of spectrum value could also reduce the willingness of potential bidders to buy the spectrum,” he noted. “For example, in Australia, an unrealistically high reserve price resulted in a valuable portion of the 700MHz spectrum left unsold and unused.”

“Setting reserve prices at reasonable levels will be key to achieving the Digital India objectives, allowing operators to focus their resources on building the necessary infrastructure to deliver high-quality mobile services for Indian citizens,” Giusti said.