It is easy to be too optimistic about how fast, and how well, former telcos can adapt their revenue and business models.

It is clear enough that both fixed and mobile access suppliers increasingly rely on Internet access revenues and content-related services.

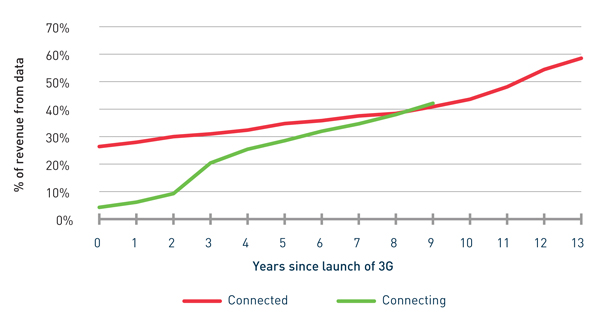

Mobile operators in Asia tend to generate between 30 percent and 60 percent of revenue from data services, the former generally typical of less developed markets, the latter typical of more developed Asian markets.

In Australia, New Zealand, Japan, Hong Kong, Singapore, South Korea and Taiwan (“‘connected’ markets), data now drives 60 percent of telco revenues.

Malaysia, Thailand, the Philippines, Indonesia, Brunei, Vietnam, Cambodia and Sri Lanka (“connecting” markets) tend to see mobile operators earning 30 percent of revenue from data services.

Sometimes that content might be packaged directly by some of the larger access providers. In most cases, involvement is more likely to revolve around content delivery, caching or other services supporting content providers.

Still, data services and Internet access, in particular, “are rapidly replacing more traditional telecoms services such as telephony as a driver of revenue,” Analysys Mason analysts argue.

The issue is how access providers can create additional services in the “content” domain.

In developed markets, partnerships between access and content and application providers might take the form of deep caching and content delivery network services, Analysys Mason argues.

In emerging markets, it is more likely marketing, billing and customer care, as well as a content provider role, are possible, says Andrew Kloeden, Analysys Mason principal.