For what it is worth, these are some references I used when preparing to teach portions of a "change management" course to some Asian telco executives a couple of years ago.

As you clearly can see, the whole process inherently is political: executives have to overcome resistance to change, creating a sense of urgency, then building a coalition to overcome resistance, then creating and communicating the vision.

Organizational personnel then must be given authority to make the changes by acting in non-traditional ways. People with power to support and sustain the changes must be hired and promoted. Perhaps the corollary is that key obstacles have to be removed.

What business are you in?

Executives know what business they are in at present. The difficult question is what business they will be in in the future. That’s the hard part. Some organizations will eventually find themselves in different lines of business.

What is the value of the fixed network? How are fixed networks used? What is the opportunity or danger from mobile substitution? What, in fact, is your response to "mobile" competition or the mobility business?

In any event, data services are driving growth on both fixed and mobile networks. And that might always be the case. But what is the relationship between access and services?

What happens to smaller carriers? Scale always matters in the communications business. Will organic growth or acquisitions drive growth?

Many service providers will have tough choices to make, such as whether to sell the business, divest some parts of the business, or outsource parts of the business. Others will find the business context has changed.

Is your business growing, flat or declining?

Global telecom revenue tends to grow, in most years. But that doesn’t mean every segment, and every market, does so.

Your business strategy will reflect that dynamic. Some service providers face a fundamentally tougher future business climate. That is true in Europe, and could be an issue in other similar markets. Consider four years of decline in the U.K. market and other Western European markets.

That is a problem for most service providers in developed markets, less a problem for developing markets, where the decline of voice revenue is not yet a problem. Some think additional markets are approaching a peak. Even mobile messaging is becoming mature.

But the Asia-Pacific region is generally seeing high rates of revenue growth. So, in general, does most of the developing world. But growth will not be universal.

Regulatory action also will affect your strategy. In some cases, regulators will take action to decrease your revenue. Regulators also powerfully affect your business model, prices, revenue opportunities and therefore strategy.

What business should you be in?

What is the foundation for your business? what is the lead offer? How much must you supply? How will that change, over time?

How much should you rely on organic growth, versus acquisitions. Can you, and should you, enter the mobile business, if you are not already in that business? Is such a move even feasible?

Is unified communications the answer? How about machine to machine services such as home automation? How big will that business be in the Asia-Pacific region?

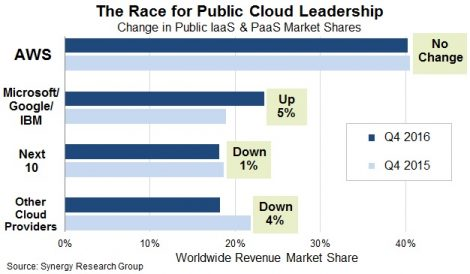

What about cloud computing? What is the role of entertainment video? What about connected car opportunities? How much can service providers make from the connected car business?

What are the relative values of business and consumer customer segments? What do those customers want to do? How big will product transitions be? In any case, business models must change, many would argue. If there is good news, it is that such transitions are possible.

Who are your competitors?

Who are the logical, and unexpected, potential mobile service providers? Can mobile compete with fixed networks for broadband access? Even the most stable markets can be upset by new competition.

The switch to IP networks automatically allows new competitors into any business, especially non-traditional providers. That means new competition is coming. Look at France, where Illiad has disrupted the market.

Who are your customers?

Do you serve consumer and business customers, wholesale or retail customers? What do they want from you? How might your customer base change in the future?

What are you doing now?

It is important to contain cost. That might not be so easy. But in competitive markets, the lowest cost competitor tends to win.

And customer demand is changing. Keep in mind that big changes in the communications business tend to have a long gestation period, where it doesn’t seem much is happening. But then we hit an inflection point and everything changes quickly. Because change is slow at first, many will move too slowly to meet coming challenges.

Market competitive Internet access offers provide one example. In some markets, change now has become non-linear.

Still, managers will do best, financially, by protecting existing revenue streams, even as new lines of business are grown. The reason is revenue magnitude. The legacy business normally is large; the new businesses small. So small changes in the legacy business represent much more revenue impact that big changes in new lines of business.

What must you do tomorrow?

Over the medium and longer term, new revenue sources must be found. In many cases, there will be serious gross revenue implications. The saying “exchanging analog dollars for digital dimes ” captures the dilemma.

But even legacy services require more investment. And nobody likes being thought of as a dumb pipe. But “access” is a foundation for the rest of the business. Untethered might be as important as “mobile.” Can you use new spectrum?

But in many cases, major change will be necessary. But the timing of your moves will be crucial. And what drives growth is a question.

Much also depends on the future competitive environment, including mobile bandwidth capabilities that challenge fixed networks.

What are your unique sources of advantage?

Does your firm possess unique sources of value? If so, what are they, and how do you know? How much value will your network provide in the future? Is innovation one of those strengths?

How do you create value? What should your core revenue strategy be? If you are a fixed services provider, what is the strategic value of your network?

Are your people ready for change?

Skills need to change, and that can be difficult to manage. Change will be easier for mobile service providers, harder for fixed network service providers.

Reinvention is risky and hard, but there are some examples of success. The bad news is such success normally happens for larger carriers, not smaller carriers.

Are you making the right investment choices?

What is your network?

Wi-Fi hotspots now are part of the carrier infrastructure, even when those facilities are not owned. What is your strategy about mixed private and public access? Consumers are rational about the value those options represent. Can you match your services to those expectations? How does Wi-Fi figure into your strategy?

How must you run your network to accommodate higher Internet access demand? In many cases, gigabit networks will become a market reality.

If you run a fixed network, and must upgrade, which network do you choose? Can you use unlicensed spectrum? Can you use mobile networks?

Industry Issues

Net neutrality will have impact on revenue models and innovation. But investment is a bigger issue. So is intensified competition. That also means more mergers. Over the top competition is a fact of life.

Mobile services are a strategic factor globally. So is the Internet. How fast use of the Interent is growing likewise is a major investment issue.

Disruption is a major industry concern. Sometimes, that disruption can be unintentional. Often, the attacks use unconventional approaches.

Where is the revenue growth?

Mobile services drive growth, globally, but the role of fixed networks will vary from market to market. Public access will provide a niche opportunity. In many instances, mobile networks will be the primary way people buy high speed Internet access.

One reason so many service providers now bundle products is that the old “one product” model is broken. There is just too much competition to support a business that way.

How do you respond to over the top services?

In some specific instances, OTT could help service providers. Also, software or application services might grow faster than hardware based solutions. Unified communications might be one example of that trend.

Sometimes the revenue models are not completely clear. And every larger service provider must decide to get into OTT apps themselves, or not. That requires an assessment of whether OTT messaging cannibalizes text messaging.

That could unlock some Internet ecosystem revenue for service providers. The point is that service providers have choices.

But that doesn’t necessarily mean service providers always should respond to new offers by matching them, as logical as that seems. Can you compete? Should you?

How do you price and package services?

Bundling works, which is why most service providers are striving to be multi-product providers.

Crafting retail offers entails some science, some art. The challenge of pricing Internet access will become more difficult in the future.

In many cases, adding small incremental charges can add more revenue than big new services initiatives. But packaging tactics can make a big difference.

Mobile service providers are counting on 4G networks to boost revenue. Just how impact that will have is unclear. There is hope, over the long term, but new revenue opportunities often emerge only after some time has passed. Tablets might be an exception to that rule.

How offers are constructed might also become important. Today, service providers price by the minute or by the megabyte. Someday we might price by the value of an application. That will require retail packaging that is both simple and sophisticated.

One growing problem is that people have choices. There simply are other ways any consumer can solve a problem. Many of those choices have revenue implications.

Price anchoring will be important.