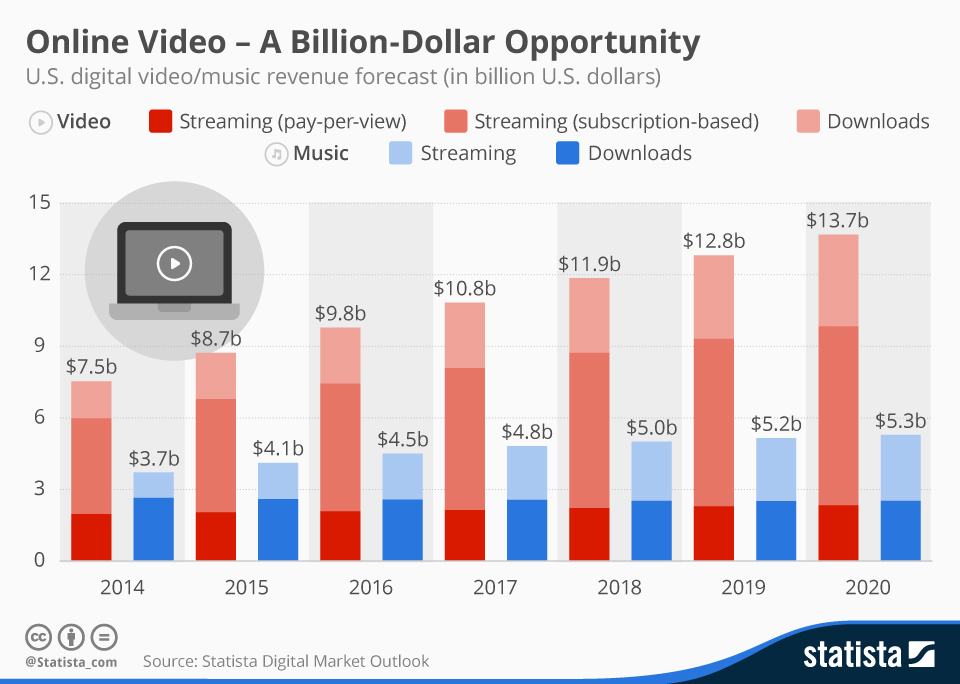

By now, nobody is surprised to hear that linear video subscriptions continue to drop or that over the top subscriptions are growing. In aggregate, there are more U.S. paid streaming accounts than linear accounts in service.

Net changes in revenue and accounts are harder to describe, as every quarter and year, some new accounts are added on both linear and streaming ledgers, partly because of churn (customers switching providers), sometimes because of moves (accounts are cancelled at one location but possibly added at another location), temporary suspensions.

In fact, linear revenue might actually be growing, even as accounts dwindle.

Netflix has some 55 million U.S. accounts, while Amazon Prime has some 90 million subscribers. All the largest linear video providers together have about 92.2 million accounts.

But since linear subscriptions represent many times more revenue than a typical linear video subscription, revenue losses are happening, even for firms such as AT&T that sell both linear and streaming video, and even when the net change in streaming accounts offsets the loss from linear accounts.

Total revenue is another story, as monthly subscription revenue earned by a linear account can be an order of magnitude greater than the revenue from any single OTT streaming account.

Among the bigger issues is the rate of decline of linear subscriptions, which seems to be accelerating. Net changes (including new accounts and customers switching providers) typically mean the gross losses are less than headline numbers might indicate.

In 2017, for example, the major U.S. providers lost about 1.5 million accounts, up from some 760,000 in 2016, according to Leichtman Research Group.

The big swing was that streaming services owned by the linear providers gained 1.5 million accounts, nearly the amount lost by the two satellite services.

In that case, the net losses by linear providers were about zero, even if the switch was from higher-revenue linear to lower-revenue streaming accounts.