Household spending (all other things being equal) is a zero-sum game: when spending in one category rises, spending in others must drop. Spending on communications varies by country.

For connectivity service providers, there are clear implications. To earn more money per account, service providers likely must add new types of products, creating enough value that consumers are willing to buy less of other goods. Shifting demand curves in that manner is quite difficult. It is not impossible, just difficult.

There is, for example, some evidence that households are spending more on communications products(devices plus connectivity and apps) than they used to spend on communications in the past.

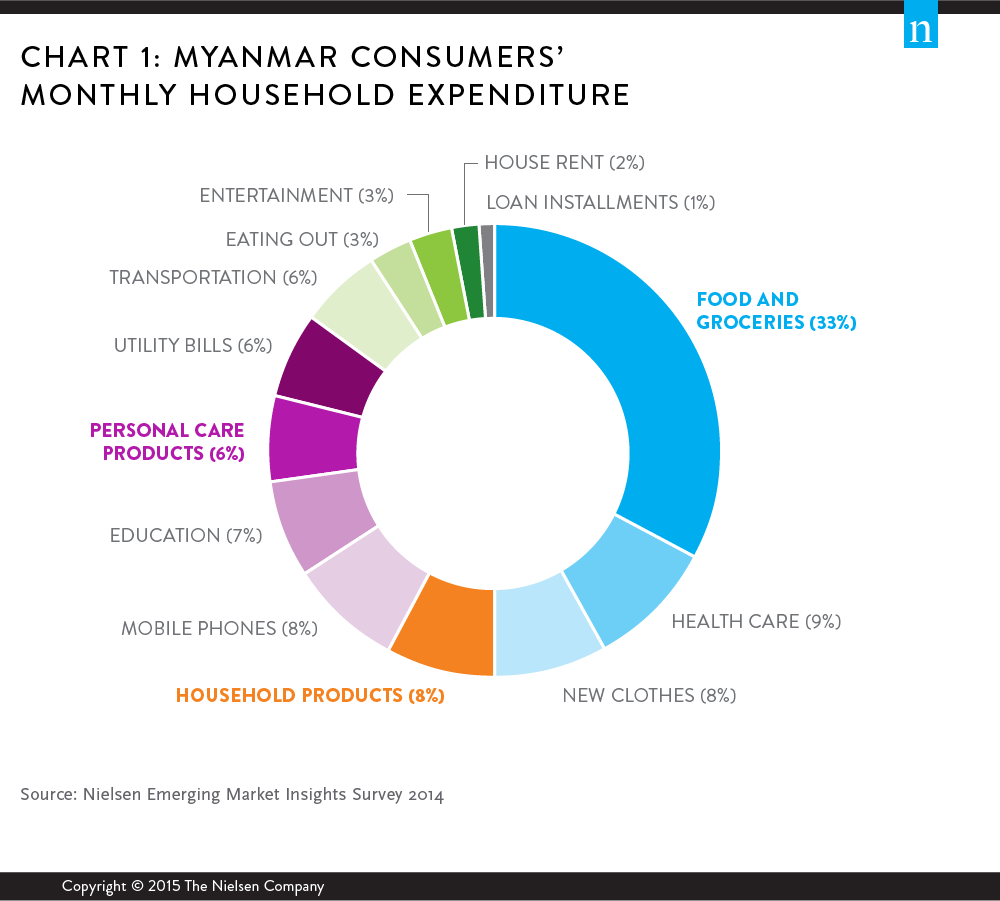

In Myanmar, a new mobile market, spending per household might be as high as eight percent of total spending. In Australia, communications spending (devices and services) might be just 1.5 percent of household spending.

In South Africa, households spend 3.4 percent of income is spent on communications (devices, software and connectivity). In Vietnam, communications spending is about 1.5 percent of total consumer spending.

In the United States, all communications spending (fixed and mobile, devices, software and connectivity, for all household residents) is perhaps 2.7 percent of total household spending.

Of course, it is entirely possible that “all things are not equal.” Incomes are rising in many parts of the world, creating more discretionary income. Prices for communications products (hardware and software) are changing: rising for top-end devices; dropping for the growing base of affordable devices.

Since subscription TV now is often considered part of the “communications” industry, both connectivity and entertainment revenues have to be considered.

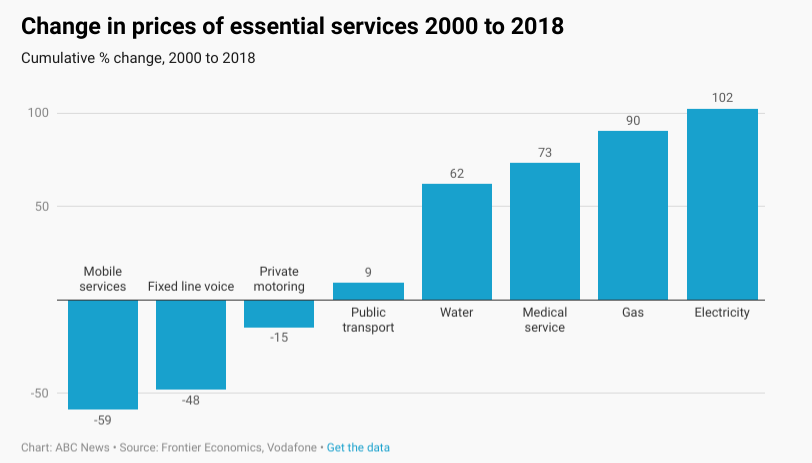

Also, prices for connectivity services are dropping. From 2000 to 2018, mobile and fixed line charges in Europe and other developed markets have dropped.

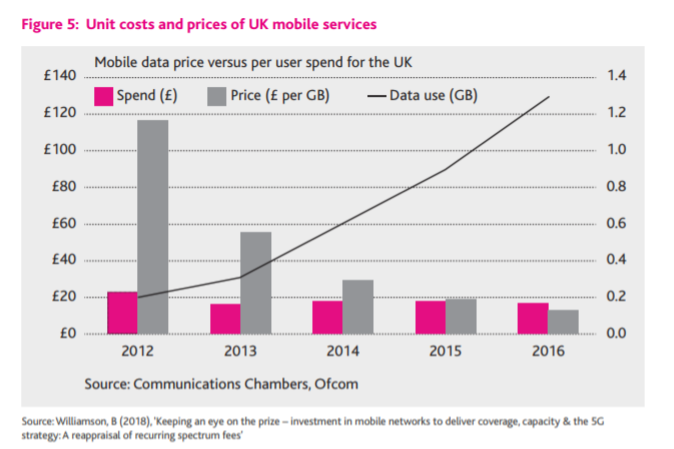

Consumer demand also is shifting. There is less demand for voice and texting services, much more demand for data services. Basically, that has shifted communications spending away from voice and messaging and towards internet access.

Up to a point, we see the same trend in mobile and data access that we earlier saw in long distance services: lower cost per unit but sales of many more units. Still, consumers only have so much money to spend on communications overall.

That does not mean the demand cannot be shifted. That is possible, but not easy. One reason service providers look to “move up the stack,” adding more value by occupying new parts of the value chain (applications and services, for example) is that doing so adds new potential revenue sources.

That is one way to shift revenue per account: create conditions where consumers spend more money, on new products, beyond the existing suite of products.