It is fair to say there remains much skepticism about the ability of 5G providers to take fixed network internet access market share. But count AT&T among those who believe this will be a material development.

“I do think, three to five years out, there is a crossover point where 5G passses home broadband, and 5G has better performance than fiber,” Randall Stephenson, AT&T CEO, has said.

Stephenson believes AT&T will have a truly nationwide “fiber speed” network, using either 5G or fiber, across the entire United States.

That would be historically unprecedented. The old monopoly AT&T had a nearly-ubiquitous copper network. But in the post-divestiture market, no tier-one service provider has been able to sell broadband to “nearly every U.S. household” at speeds representing optical fiber performance.

With AT&T, Verizon and also T-Mobile US all planning 5G fixed wireless efforts, the potential for disruption exists. It already appears that some optimistic forecasts of cable TV market share already are falling short, with telcos--especially AT&T and Verizon, already gaining share again.

The telco erosion is not completely over. But equilibrium is approaching. Fixed wireless could be quite destabilizing, in that regard.

It often is quite hard to envision fundamental changes in the connectivity business. Few of us really understood what it would mean when the internet emerged.

Few might have really understood what it meant to adopt internet protocol as the next-generation network of choice, and not the proposed asynchronous transfer mode (ATM) alternative.

Nor, prior to mobility’s transformative adoption globally, would most of us have imagined that mobile networks would succeed where all prior attempts to provide communications to everyone globally could actually be accomplished.

In perhaps similar ways, it is hard to imagine any future time when Wi-Fi is not the choice for local area network connectivity, or when fixed networks are not the best choice for high-bandwidth communications.

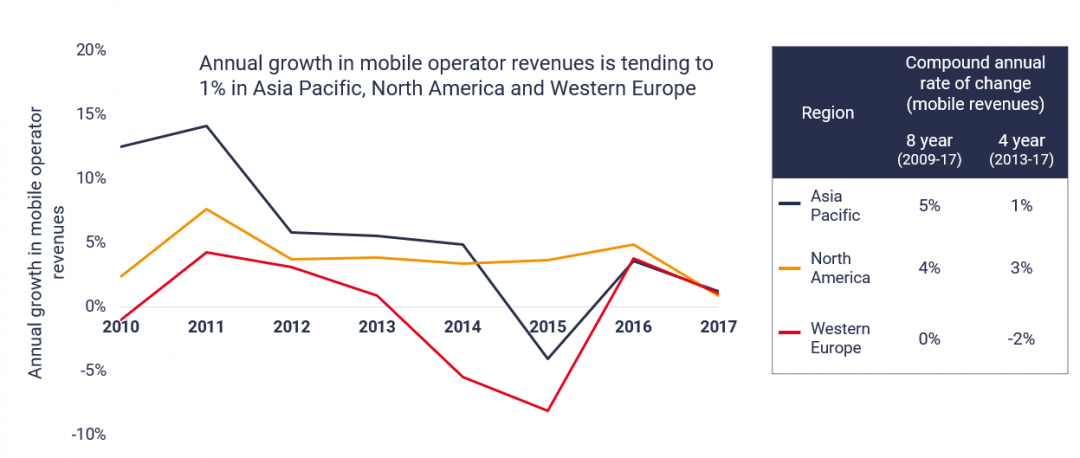

But it also is clear that mobile revenue growth is slowing. It is fair enough to note that big revenue growth slowdowns can lead to huge shifts of business strategy, as mobility once shifted global service provider attention from fixed to mobile services, and from long distance revenues to mobile subscriptions.

Likewise, fixed network revenue opportunities also shifted from subscriptions for voice to internet access.

The traditional response always has been to try and take market share away from other providers. That accounts for cable TV operator attacks on business connectivity market share, and the earlier entry into voice services.

“Taking market share” also accounts for telco movement into entertainment video distribution and content asset ownership.

Among the new battlegrounds is internet access, for consumers and businesses, which could see a shift of share from fixed to mobile providers.