One hears quite a lot of talk about how connectivity providers can become platforms. Telefonica, for example, has for some time deliberately tried to recast itself as a digital enabler or platform, not a connectivity supplier, and its experience illustrates just how hard that transition might be.

So what is a platform? Electricity, one might argue, is a platform. But that probably shows the weak version of “platform.” Electricity enables lots of other use cases and businesses, without any direct business relationship between the electricity provider and businesses built on the use of electricity.

In that sense, the old “dumb pipe” analogy continues to hold, even for a so-called platform.

Other analogies make more sense. Android is a better example of a platform because a business relationship actually exists, and the owner of Android gains business value from each business relationship, as did Microsoft and Apple before it. That is the latest version of the notion of platform Telefonica and others seek.

Other logical examples exist. As Amazon and Alibaba are platforms for commerce and Netflix arguably is a platform for content, the key point is that a viable platform involves a business relationship between the platform and its enabled services or products. And that business relationship generates revenue for the platform.

The digital era will place greater expectations on telecom operators as customers turn to digital service providers to support a broader range of services and use cases, says Steve Vachon, TBRI analyst. But will they?

Connectivity providers now operate in an ecosystem including content suppliers, web-scale application providers, device and computing services entities. So the hope is that Telefonica--and other connectivity suppliers--can create more value for partners using their network.

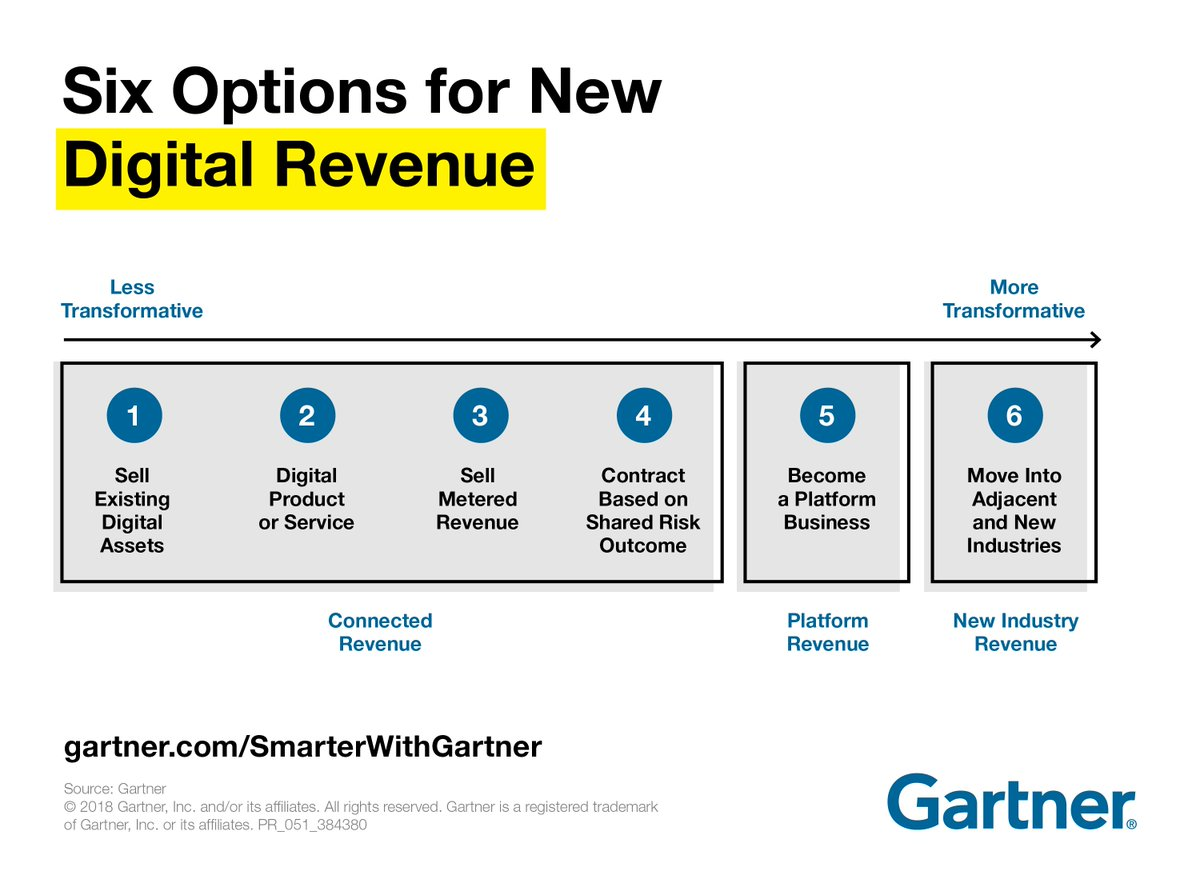

That has been true for Akamai’s content delivery network, and other CDNs, clearly. But substantial revenues from “platform” capabilities are hard to find, compared to other approaches such as moving into adjacent parts of the ecosystem.

Comcast bought NBCUniversal and became a content owner and movie studio, theme park operator and content network provider. AT&T bought TimeWarner and similarly became an owner and producer of content, provider of content networks and operator of theme parks.

If mobile edge computing (sometimes called infrastructure edge computing) succeeds, mobile operators will generate platform revenues from enterprises that buy edge computing services. But that is some ways off, it appears.

In the meantime, it remains hard to pinpoint significant revenues from “platform” operations.