When AT&T outlined its market focus at its recent investor day, three priorities were named: broadband connectivity; software-based entertainment and “fantastic storytelling.” Many opposed the acquisitions of DirecTV and TimeWarner, preferring that AT&T remain focused on its connectivity business.

In the wake of the spinoff of DirecTV into a separate asset 70 percent owned by AT&T, it would be tempting to say AT&T is unwinding its move into content ownership and media revenue models. That does not seem to be the case.

Of the three areas of focus, connectivity represents one. Content distribution represents one. Content creation adds one. To be sure, AT&T generates a majority of its gross revenue from mobility alone.

Still, video distribution generated 14 percent of gross revenue in 2020 and 4.4 percent of free cash flow, with the balance starting to shift away from linear and to streaming. That will change in 2021 as the DirecTV assets are moved outside of AT&T. The move still will produce about $1 billion in free cash flow for 2021, though.

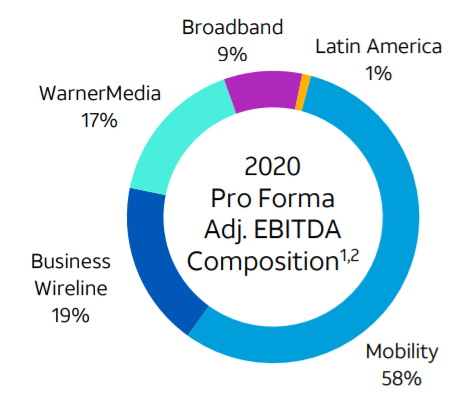

Moving out the DirecTV results, as shown in the following chart, mobility generated 58 percent of free cash flow in 2020. Video content production generated 17 percent of free cash flow, just a bit behind the business wireline segment.

One way of describing matters is that AT&T free cash flow generation is led by mobility, with significant contributions from business fixed network customers and the WarnerMedia assets. Fixed network consumer operations generate about nine percent of free cash flow.

Perhaps a key insight is that overall revenue growth is projected to be in the one-percent range. That is consistent with external estimates made for the global connectivity business as well.

For a firm the size of AT&T, operating in mature fixed and mobile markets, long-term growth arguably has to come from lines of business outside the traditional core. The impact on cash flow generation could be even greater, as AT&T says the incremental profit margin for each HBO Max streaming customer is extremely high.

“We currently earn 90 percent in margin from each retail subscriber that we add,” said Jason

Kilar, WarnerMedia CEO. That is akin to what other hyperscale application providers add when gaining an additional user.

Software as a service margins might be in the 72 percent range. Facebook gross margins are in excess of 80 percent. So the HBO Max streaming service has free cash flow implications far higher than the linear DirecTV service, which might be in the 11-percent range.

The point is that incumbent tier-one service providers (attackers are the exception) will have to create new lines of business, of some size, to fuel revenue growth. They simply are running out of runway to do so on the strength of their core connectivity businesses.

So far, content ownership and video distribution have had the most immediate impact on gross revenues and free cash flow, though hopes are substantial for additional growth in business services related to edge computing and internet of things. So far, those businesses are young enough that they are not materially contributing to revenue or free cash flow.

So critics might be underestimating AT&T’s commitment to content services.