My favorite Easter song, sung by the choir at St. John Neumann, in Reston, Virginia

Tuesday, April 13, 2021

Roll Away The Stone

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Monday, April 12, 2021

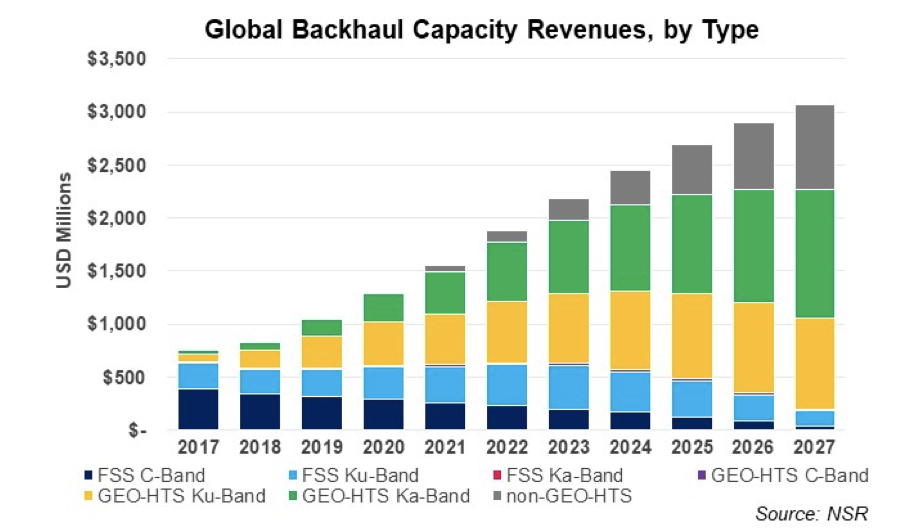

Huge Revision of Satellite Service Revenues Based on Mobile Backhaul

Some rules of thumb related to connectivity service provider revenue exist simply because use cases are fairly stable over time. In other cases future use cases are not predictable, leading to sometimes wild fluctuations in revenue forecasts.

The global connectivity service provider market, for example, is relatively stable, growing slowly to about $1.2 trillion euro in annual revenue (about $1.4 trillion) in the 2020s, adding about one percent a year. Satellite service revenues were about $123 billion in 2029, or roughly nine percent of fixed service provider revenues.

That does not seem to change much, from decade to decade, so the latest forecast of as much as $25 billion for backhaul implicitly includes attrition of other revenues, such as video entertainment distribution revenues.

Some estimate satellite backhaul revenues will grow to about $25 billion by about 2030, according to Northern Sky Research. That is a dramatic upward revision since about 2018, when satellite backhaul was estimated to reach something closer to $3 billion in annual revenues by 2027.

If that happens, it will be because of satellite backhaul for remote mobile network cell towers, it is safe to say. Earlier forecasts had suggested a maximum of cumulative revenues as high as $39 billion between 2019 and 2029.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Saturday, April 10, 2021

Will Common Carrier Precedent Might be Applied in New Ways?

Though the notion stands regulation on its head, we might be nearing a point in U.S. regulation of online media and communications--especially the regulation of platforms--that borrows concepts from common carrier regulation.

It will not be easy, and might require some new developments in legal thinking. But that happens, from time to time, even in a profession that relies so heavily on precedent.

Past actions that apply free speech obligations to private actors have used an analogy to a public square, though rarely with much success. The issue now is whether the digital public square argument gains currency.

Simply, most people might agree that the essence of “free speech” on any major platform for social media, content or even search is that anyone may publish at will, as was among the founding principles of the internet itself.

We might also agree that competition is a better framework than regulation, but also might agree that regulation is an option if all other frameworks prove problematic.

For perhaps a century, “free speech” and “common carrier” regulation of industries have been defined largely in terms of the rights of “speakers.” For media, free speech has been viewed as a right possessed by owners of printing presses, TV or radio stations, content studios, other print media, cable TV systems and now internet platforms for search, social media and commerce.

Customers of “utility” services, on the other hand, have generally been seen as the possessors of the “free speech” right, to the extent political speech is involved at all. “Common carrier regulation” has been the rule for railroad, electricity, gas, water and telecom firms, for example.

A common carrier. must provide its service to anyone willing to pay its fee, but has not generally applied to the media.

New communication or media formats tend to be regulated using older and existing models. That almost always poses big issues, as new media and communications formats often cannot--or should not--be regulated using older models.

Live performance, movie theaters, broadcast television and radio, cable TV and streaming video might provide one set of examples.

Pamphlets, newspapers and magazines, online media and social networks might provide additional examples. Regarding free speech protections, there are several important distinctions. Jurists must decide whether the “right of free speech” is for the speaker or the listener.

It is complicated. First, the First Amendment protects “owners of publishing assets,” not citizens, from government prohibitions. What is new in the internet era is the power of private entities (platforms) to silence speech, when historically this problem was seen as a potential problem caused only by government entities.

Among the new questions is which form of regulation best protects political free speech. Ironically, our older notions may be out of date.

Historically, the right of free speech belongs to the owners of publishing or communication assets: printing presses, content creation entities such as magazines or movie studios, broadcast stations, cable companies and social media, search or other online media firms.

Other entities--viewed as platforms--have not been held to have “free speech rights” and have been regulated as common carriers. Railroads, electrical utilities, water supply companies and telecommunications firms come to mind. In other words, “communication” or “public utility” networks have not been considered “speakers with First Amendment rights.”

“Federal law dictates that companies cannot ‘be treated as the publisher or speaker’ of information that they merely distribute,” Thomas says. To be sure, legal precedent does not regard a digital platform as a “common carrier.” But it remains unclear whether this would remain the case if Congress were to pass laws applying some common carrier principles on digital platforms.

Even when looking solely at the rights of “speakers,” there is a distinction between the rights of business owners “as business owners” and the rights of “speakers on platforms.” In other words, Facebook has the right to advocate in its own interests.

That, however, is arguably a different matter from the rights of users of its social media platform to express ideas.

“If part of the problem is private, concentrated control over online content and platforms available to the public, then part of the solution may be found in doctrines that limit the right of a private company to exclude,” says a ruling by Supreme Court Justice Clarence Thomas.

“Historically, at least two legal doctrines limited a company’s right to exclude,” he says. “First, our legal system and its British predecessor have long subjected certain businesses, known as common carriers, to special regulations, including a general requirement to serve all comers.”

“Second, governments have limited a company’s right to exclude when that company is a public accommodation,” Thomas notes. “There is a fair argument that some digital platforms are sufficiently akin to common carriers or places of accommodation to be regulated in this manner.”

Historically, that argument has been tough to apply; tougher to extend. But precedents sometimes aer overturned. We might be heading that direction.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Thursday, April 8, 2021

Maybe Covid Will Not Have Lasting Significant Impact on Connectivity

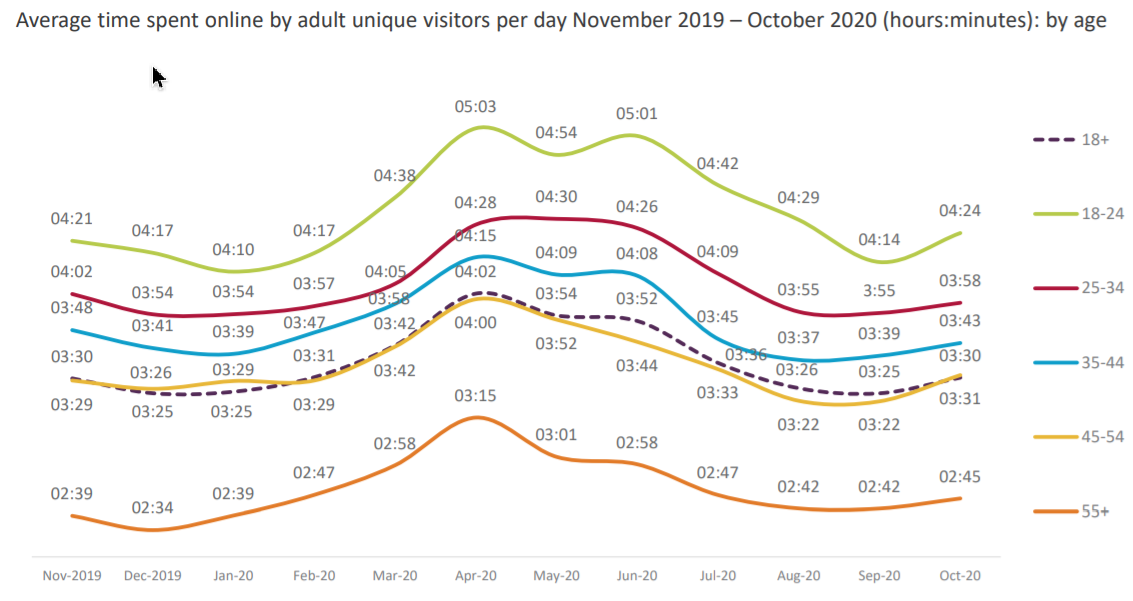

One hears much casual talk about permanent changes caused by Covid-19 lockdowns or work from home policies. Where it comes to use of communications capabilities, however, there is some evidence that the impact was quite transitory.

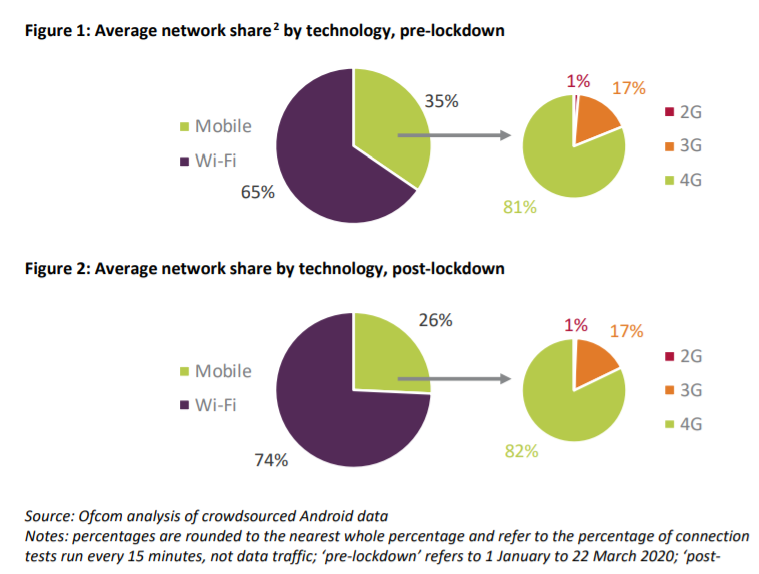

Data gathered by Ofcom shows that use of the internet climbed in February 2020, but by October 2020 was down to pre-pandemic levels. Most casual statements note the sudden surge in demand as the lockdowns began. Few seem to note that demand has returned to pre-pandemic patterns.

Some argue that mobility usage climbed during the pandemic. Ofcom data suggests quite the opposite. As you might expect, people confined largely to their homes spent less time connected to the mobile network.

People were not traveling outside their home areas so much. That is why roaming revenues dropped for virtually all mobile operators.

In other ways, mobile phone behavior was, in fact, not changed by the pandemic. Many casually make the argument that the pandemic “proves” the value of connectivity. It was important; it is important. But it might not be significantly more important, post-Covid.

Demand in urban office areas is likely to drop, as more people spend more time working from home, on a permanent basis. There will be some upgrading of connections in suburban or rural areas. But internet access was vital before the pandemic. It did not suddenly become more important because of the pandemic, though the places people used the internet did shift (from office to home; from school to home).

There was less use of mobile phones on the mobile network between March and October of 2020, as more people were confined largely to home, and used Wi-Fi connectivity.

Nor did calling behavior change. “Our crowdsourced data showed that 75 percent of panellists made a call in the first 11 weeks of the year, and 78 percent of panellists made or received a call,” Ofcom says. “There was no significant change in these proportions between pre- and post-lockdown.”

The impressionistic sense that “communications must be more important” is not necessarily borne out by the facts. It is similar to the anecdotal comments all of us have heard about “communications proving its value,” along with a belief that “communications firms must be making more money because of that.” In fact, most service providers saw revenue dip during the March to December 2020 period, for obvious reasons.

Economic activity was suppressed by government orders. And less economic activity, as in any recession, stifles communications revenues.

There are likely to be permanent changes because of the pandemic. But a dramatic and permanent leap in communications industry revenues or growth rates is unlikely.

In fact, there will be some downward pressure on demand, as urban office space begins to go unused. Fewer people working “downtown” means less bandwidth demand. Fewer people at work also means less demand for all surrounding merchants. Those merchants are also likely to require less bandwidth or connectivity demand.

Bandwidth demand overall will likely keep growing, at past rates. But the pressure is not all “up.” There will be some redistribution of “work” demand to residential areas. But the key driver of residential broadband demand is entertainment video, not use of work apps.

That will ripple through network planning assumptions, at the very least, even if revenue impact is relatively neutral. What seems to be developing is a rather temporary Covid impact on capacity demand and user behavior. In other words, Covid might, in the end, not have very much impact on connectivity revenue or demand.

Usage grows every year, irrespective of temporary events. More people watching more video streaming is going to affect usage more than did Covid.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Lumen Analyst Day 2021

It is long, but provides more color on Lumen's strategy than there is time to present at a quarterly earnings call. Useful is what one can glean from the mix of lines of business that are being harvested, versus the lines that are getting investment.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Saturday, April 3, 2021

Big Firms Benefitted from Covid-19, Small Firms Did Not

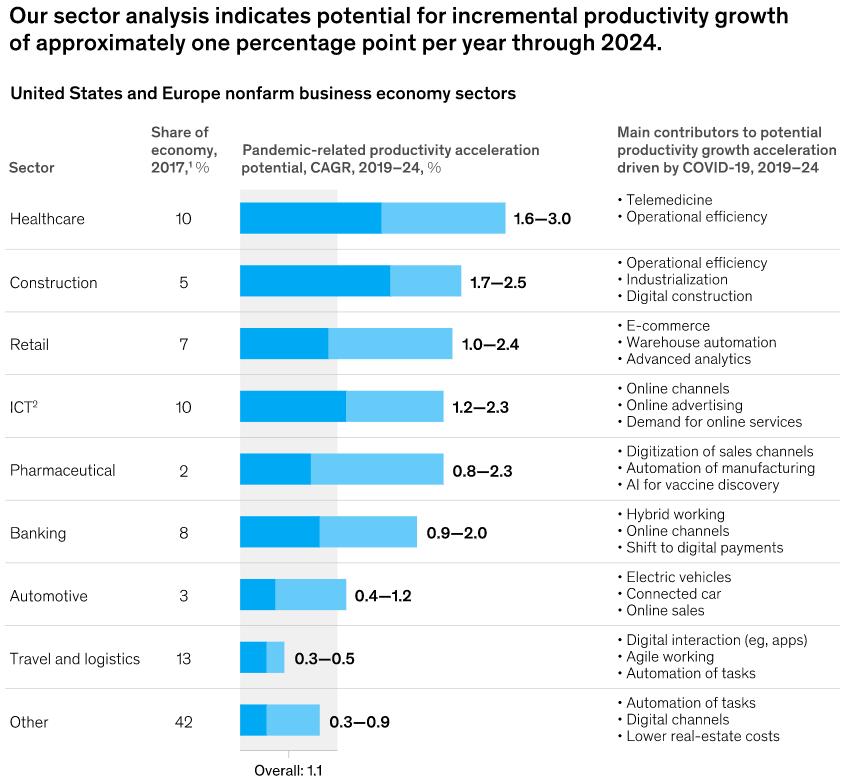

The Covid-19 pandemic has battered small firms much more than hyperscalers or “large, superstar firms,” McKinsey data suggests. Between the third quarters of 2019 and 2020, “large superstar firms lost no revenue” while competitors experienced a decline of 11 percent, McKinsey says.

Looking at a range of revenue-related metrics and information technology investment, McKinsey researchers found that “advances appeared concentrated among large superstar firms, particularly in the United States.”

“This was true across many sectors, but particularly pronounced in professional, scientific, and technical services, IT, electronic manufacturing and healthcare,” McKinsey notes.

The McKinsey analysis included items such as spending on research and development, investment, mergers and acquisitions activity as short-term proxies for the range of potential drivers that could accelerate productivity.

The issue is what happens longer term as applied technology either does, or does not, positively affect revenue growth. A productivity paradox has existed in the past, where increased information technology spending does not produce a measurable increase in productivity.

“Before the pandemic, productivity growth had not always fully translated into broad-based growth in wages and consumption,” McKinsey notes.

Beyond that, the impact of “technology for labor” shifts “could, over the longer term, dampen employment and incomes, and hasten labor-market polarization and propensity to spend,” McKinsey says.

The point is that after a short-term economic rebound driven by economic reopening, longer term economic growth is not so clear. We should see growth, but how much is less clear. Many ICT investments operate on the cost side of the business model, not necessarily the revenues side of the model.

But cost for one entity always is revenue for another. Substituting machines for labor often is good for firms, but bad for employees and therefore reduces aggregate demand. Higher productivity is seen as a good thing.

Whether recent investments produce higher productivity remains to be seen. Whether such gains outweigh potential negative changes in demand is another question.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Implications of GDP Damage Worse than Great Depression, Far Worse than Internet Bubble or Great Recession

For those of you who lived through the internet bubble burst in 2001 and the Great Recession of 2008, the Covid-19 pandemic exceeds the economic damage by quite some scale, surpassing the carnage of the 1929 Great Depression.

We all seem to sense that many changes in business and personal life will be permanent, post-Covid. Enterprise executives indicate big changes are coming.

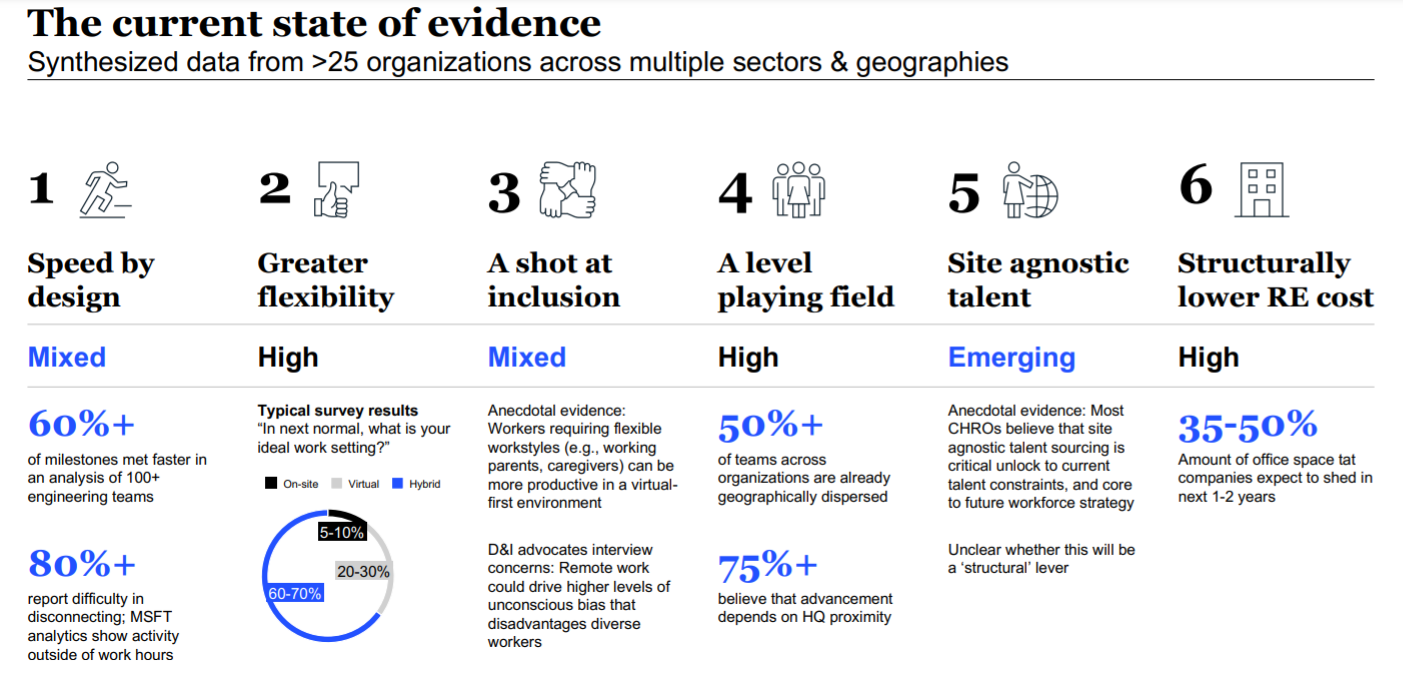

Remote work environments seem to have encouraged “output oriented” work flows and may have enabled faster decision making, McKinsey reports. Hybrid work situations are expected to become permanent, while “site agnostic” employee sourcing will increase, along with possibly 35 percent to half of all existing office space to be shed over the next two years.

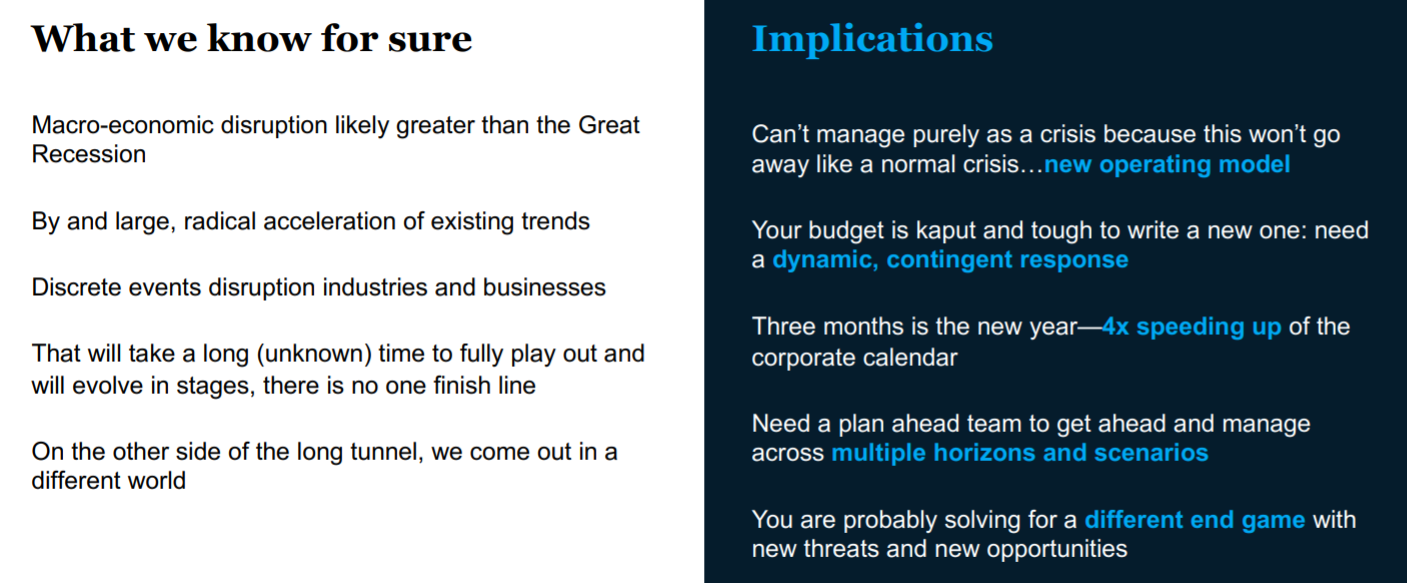

McKinsey argues that geographically “distributed work” produces more value than “remote work.” And those are not even the most important implications enterprises must consider. The “recovery” from the crisis will not follow patterns we have seen in prior economic downturns.

So a new operating model will be necessary. The need for agility no longer will be a nice to have organizational capability, but might be a requirement. Business will run about four times faster than in the past, making “three months the new year.”

New threats and opportunities might well be the new reality as well. That might well include a change of revenue sources and business models.

Lots of people talk about disruption. Not so many have actually had to face it. Many more might get their first chance to do so.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Comments (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...