Are telcos still dominant providers of consumer communications services, requiring heavy regulation historically applied to such providers?

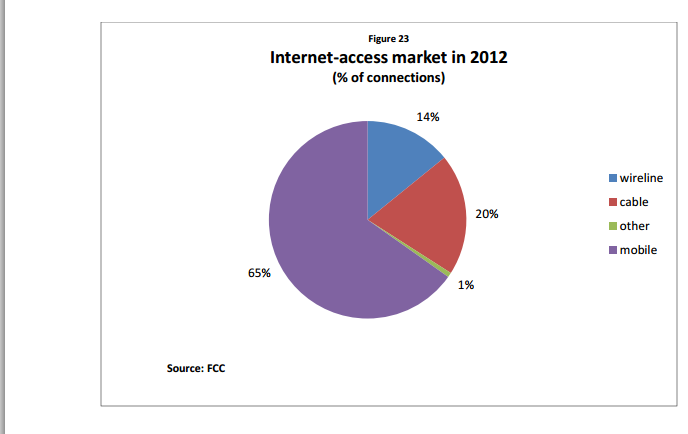

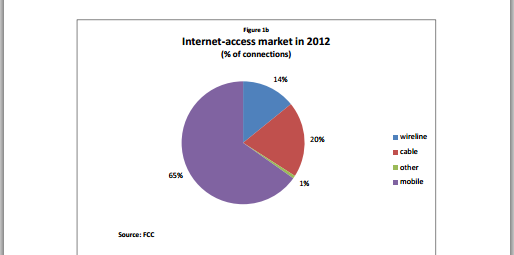

At the end of 2012, incumbent local exchange carriers (telcos) had 34 percent share of the consumer voice market, 14 percent of the high speed access market and 10 percent of the video subscription market.

And yet there is persistent thinking that firms including AT&T and Verizon need to be highly regulated as “dominant” providers.

If Comcast succeeds in buying Time Warner Cable, it will have 40 percent share of the U.S. high speed access market. Who is the “dominant” provider, for purposes of determining market power?

And with the caveat that traffic is not identical to revenue, The overwhelming majority of network traffic now is Internet Protocol, not legacy time division multiplex voice.

Consumer traffic now represents most of that IP traffic, according to Cisco. In 2012, total U.S. IP traffic was 157 exabytes and that is expected to triple in the next five years, so that total U.S. IP traffic in 2017 will be 445 exabytes.

Consumer U.S. IP traffic in 2012 was 136 exabytes and by 2017 is expected to increase

to 387 exabytes, roughly 86 percent of total IP traffic in each year.

And in a big shift, most of that consumer IP traffic is entertainment video, either

over the open Internet or managed video services.

In 2012, IP video accounted for 120 exabytes of traffic and by 2017 it is expected to grow to 359 exabytes, at which point video would represent roughly 80 percent of all U.S. IP traffic.

That traffic pattern shows why revenue models now have become such an issue for access providers. Voice, a managed service that traditionally drove revenues, is shrinking, while most of the video traffic does not have any direct revenue implications for access providers.

U.S. traditional switched traffic, which consists primarily of voice traffic, constituted less than one exabyte in 2012.

At the same time, because the TDM network carries less and less traffic, it becomes increasingly inefficient over time. That is why there are growing calls to prepare for a shutdown of the PSTN network.

Doing so would allow access providers to deploy capital and operating funds to support the single network that now carries the overwhelming majority of traffic.

While total voice lines in service are supplied by cable TV companies and other firms, telco consumer switched access lines have decreased by 66 percent since 1999, the

earliest period for which the FCC reports such numbers.

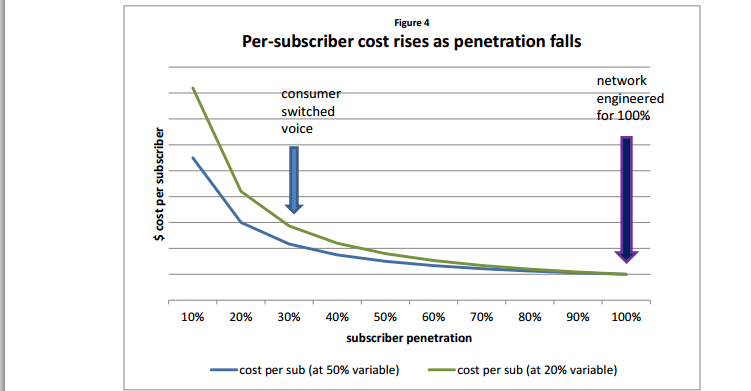

The clear implication is that is uneconomic to continue to support the TDM network. “Even if network operators are efficient and manage to make 50 percent of their cost variable, cost per subscriber at 30 percent penetration is more than twice what it was at 100 percent penetration, the study by Anna-Maria Kovacs, visiting senior policy scholar at Georgetown University’s Center for Business and Public Policy, indicates.

If only 20 percent of the cost is variable, then cost per subscriber is nearly tripled at 30 percent penetration. At 15 percent penetration, the level AT&T is approaching in some of its states, cost per subscriber quintuples for a network that has 20 percent variable cost and quadruples even for a network that has 50 percent variable cost.

By the end of 2012 only 34 percent of U.S. households purchased traditional switched

telephony service and only five percent of households relied on it exclusively.

The other 29 percent of households combined fixed voice with wireless services, while 28 percent of households used VOIP service, while four percent used VoIP exclusively.

In contrast, mobile phones have become the primary way people use voice services. About 90 percent of households in 2012 had mobile service, while 38 percent had no fixed network voice service.

About 16 percent of households mostly used mobile service. By the end of 2013, it is likely that more than 60 percent of households will be mobile-only or mobile-mostly.

The study also suggests why fiber-to-home upgrades have become more important. When relatively few consumers wanted to buy access at speeds of 50 Mbps or 100 Mbps, and when those services cost $100 or more, fiber-to-neighborhood access networks would work.

That no longer is the case for symmetrical gigabit networks selling for $70 or $80 a month. At such speeds, only a fiber-to-home works.

Whatever real concerns telcos have had about the business case for fiber-to-home networks, end user demand and competition have changed thinking.

A Nomura report of July 2014 shows that where ILECs have upgraded their networks with fiber to the home or to nodes close to the home, telcos gained high speed access share over cable TV suppliers.

From January 2011 to June 2013, ILEC fiber (primarily FIOS and U-verse) gained 7.3

million subscribers, while cable broadband gained only 5 million customers. And in positioning against Google Fiber, rather than cable operators, might have clear impact on market share.

Cable operators have had 57 percent to 59 percent share of the high speed access market since 2007. If telcos upgrade to gigabit speeds and fiber-to-home architectures, they likely will, where such services are available, be able to make market share gains.

Ironically, cable operator choices hinge largely on how much video share is lost, and how buyer preferences change.

At some point, as cable operators were able to do in converting analog TV signals to digital format, they might be able to allocate more bandwidth over the hybrid fiber coax networks to high speed access, and less bandwidth to video services.

It is not a trivial exercise, but reducing the amount of linear programming delivered will free up more bandwidth for high speed access.

Home broadband subscription is highest among non-Hispanic Whites, 74% of whom have home broadband. Among non-Hispanic Blacks, only 64% have home broadband and among Hispanics, only 53% have home broadband.

But when mobile Internet access is considered, some 80 percent of non-Hispanic Whites, 70 percent of non-Hispanic Blacks and 75 percent of Hispanics buy Internet access.

Among those who use a mobile phone to access the Internet, 60 percent of Hispanics describe themselves as mostly going online using their mobile phone, 43 percent of non-Hispanic

Blacks do so, while 29 percent of non-Hispanic Whites do so.

source: Internet Innovation Alliance

The point, argues Anna-Maria Kovacs, visiting senior policy scholar at Georgetown University’s Center for Business and Public Policy, is that mobile Internet access plays an important role in the overall Internet access supply.

Under many circumstances, mobile access supplies most of the value of such access, even if the fastest speeds will be provided by the fixed networks.

As always, there are two fundamentally-different ways of harmonizing regulations in markets that have crossed industry lines: apply the heaviest forms of regulation to the new providers, or free up former highly-regulated providers to the standard of the less-regulated new suppliers.

The answer matters in large part because investment implications follow.

A team led by Robert C. Atkinson of CITI estimated that from 2006 through 2011, 53 percent of the capital investment made by the three largest incumbent local exchange carriers was allocated to their legacy networks, while just 47 percent was spent on broadband infrastructure.

Assuming that ratio is typical of the industry during those six years, and given that the ILEC industry spent $154 billion in capex during those years, the ILECs spent $81 billion on legacy networks, while just $73 billion was spent on modern broadband infrastructure, argues Kovacs.

You likely would expect an industry-focused group to call for a lighter regulatory touch But that doesn't mean the position is incorrect, where it comes to incentives for robust investment in future networks.