NEC is ending the development, manufacturing and sale of smart phones, a move that hardly is surprising given NEC's small market share and declining sales volumes.

NEC merged its cellphone handset operations with those of Casio Computer Co. and Hitachi Ltd. in 2010 to create NEC Casio Mobile Communications.

The three firms hoped their combined resources would allow them to make progress in the smart phone market.

But the effort has had no more success than other former leaders have had against Apple and Samsung.

A decade ago, NEC was the biggest player in the Japanese mobile phone handset market with a 23 percent share.

Wednesday, July 31, 2013

NEC is Getting Out of the Smart Phone Business

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Tuesday, July 30, 2013

Which is the Better Mobile Revenue Model, Advertising or E-Commerce?

As Google had built the first big technology company driven by ad revenues, you might argue Amazon is striving to build the first big mobile company driven by e-commerce, even if right now it arguably is focusing not on mobile devices but only tablets.

As Google had built the first big technology company driven by ad revenues, you might argue Amazon is striving to build the first big mobile company driven by e-commerce, even if right now it arguably is focusing not on mobile devices but only tablets.

Part of the challenge, as with any other would-be mobile platform, is creating a sizable appstore and developer community. On that score, some note that the Amazon Appstore earns developers almost as much revenue per active user as they do on Apple’s platform.

The importance of the Appstore success is that it also puts into place the very app ecosystem that would be necessary for any future success of an Amazon smart phone.

For the moment, though, the Kindle Fire is an e-commerce platform for sales of all sorts of Amazon products, ranging from ebooks and music; movies and TV shows and apps. In fact, Amazon aims to convert mobile convert users into buyers in about 30 seconds, as a goal, and boost the percentage of mobile sales from the current eight percent of total transactions that in 2012 were about $61 billion.

In the second quarter of 2013, Amazon booked $15.7 billion in revenue. In the same quarter, Google booked $14.11 billion in revenue.

The conclusion has to be that either can work, though the profit picture is more mixed. Amazon tradtionally has been willing to invest in growing its business, irrespective of quarterly impact on earnings. Google has been less willing to do so.

Mobile advertising might generate about nine billion in mobile ad sales for Google for all of 2013. Amazon might earn about $5 billion in mobile sales in 2013.

Mobile advertising might generate about nine billion in mobile ad sales for Google for all of 2013. Amazon might earn about $5 billion in mobile sales in 2013.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Netflix Does Not Cannibalize Linear TV, Study Suggests

A study by TiVo Research and Analytics suggests Netflix does not actually cannibalize linear TV. To wit, there seems to be no significant difference between the amount of reported television viewing in Netflix and non-Netflix households.

About eight percent of respondents subscribe to all three over the top services.

In a sense, the study might be considered good news for incumbent service providers. Netflix, though arguably a potential rival for consumer spending on video entertainment, does not yet seem to have had much impact on overall demand for video entertainment subscriptions.

But few observers think that will always be the case.

In other words, "Netflix is not currently a substitute for traditional television,” according to Mark Lieberman, TRA CEO.

But Lieberman quickly added that “the future of television may tell a different story,” leaving open the possibility that, at some point in the future, Netflix subscribers just might watch less traditional TV, in most cases TV that has been delivered by a video entertainment provider.

So video entertainment providers are likely not to be surprised by the findings about current behavior, nor mollified about the safety of their business models in the future.

As there continue to be some debates about the ways use of digital video recorders could affect the quantity of linear TV watched, and ongoing worries about ad skipping that endangers the advertising revenue model, so the study will not reassure incumbents that over the top alternatives to linear TV actually pose no threat.

DVRs have arguably not proven to be a disaster for the ad business model. But few would suggest that it has had no impact on the amount of advertising seen by end users. And features such as Dish Network’s Hopper do pose a much more significant amount of danger.

Likewise, though perhaps not a present danger, Netflix could in the future lead to serious amount of viewer behavior and buying shifts.

And there are some findings that could be problematic. Some people are heavy TV viewers and some are not. Typically, heavy viewers buy more of all video entertainment products and services, so viewing is not so much a zero-sum game.

That might, some would say, explain the “no cannibalization” findings. But what will be much more potentially troublesome are lighter viewers, who might not want to watch more TV, or multiple services and features.

Greater market share shifts are likely to happen among the lighter users, because they do not value the experience as much as heavier users.

TiVo’s research confirmed that Netflix households tend to be heavier TV viewers. For example, Netflix households are heavier viewers of premium dramas.

Households that reported viewing "House of Cards" watched 85 percent more HBO than non-Netflix households.

"House of Cards" households watched Showtime's "Homeland" 125 percent more than those who don't use Netflix.

Netflix households viewed Showtime's "Homeland" 26 percent more than those who don't use Netflix.

Of the survey respondents 57 percent reported they subscribe to Netflix, About 50 percent also reported they subscribe to Amazon Prime and 18 percent said they buy Hulu Plus.

About eight percent of respondents subscribe to all three over the top services.

In a sense, the study might be considered good news for incumbent service providers. Netflix, though arguably a potential rival for consumer spending on video entertainment, does not yet seem to have had much impact on overall demand for video entertainment subscriptions.

But few observers think that will always be the case.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Monday, July 29, 2013

AT&T Home Base is a Facilities-Based Assault on Verizon

AT&T Home Base is a service supplying voice and Internet access using AT&T’s mobile network, instead of its fixed line network. The catch is that AT&T is doing so “out of market,” in Verizon fixed network territories.

AT&T Home Base now is available in Delaware, Kentucky, Maryland, New Jersey, Pennsylvania, Virginia, West Virginia and Washington, D.C., all except Kentucky being areas served by Verizon’s fixed line networks.

In other words, AT&T’s third generation and fourth generation networks are the platform for what in an earlier time would have been called an “out of market” assault on Verizon, even though the traditional structure of the landline business, since the AT&T divestiture in 1984, has been based on “exclusive” local service territories.

Critics will argue, with some justification, that mobile broadband, used as a fixed service platform, is not an equivalent offering, especially in terms of price per gigabyte or size of the usage bucket. But customers are smart enough to choose the service that makes most sense, given the actual circumstances of each household’s usage pattern.

The significance is that Long Term Evolution now is being promoted by AT&T as an Internet access enabler, and that LTE also is becoming a way for AT&T to attack Verizon's fixed networks business, on a facilities basis.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Add America Movil to Catalysts for Europe Consolidation

Telefonica’s move to buy KPN-owned E-Plus and vault itself up into the top ranks of the German mobile market will face several challenges, including regulatory approval and possibly a challenge from KPN investor America Movil, which owns 29.8 percent of KPN, and might not want a major rival to acquire a stronger position in the German market America Movil itself has wanted.

America Movil had invested in KPN in the first place to get a foothold in the German market. If E-Plus is sold, America Movil will have to rethink its ability to enter the German market, and possibly its investment in KPN as well. One might also argue America Movil could consider its own rival bid for E-Plus, with a partner.

Up to this point, America Movil had pledged not to acquire more than 30 percent of KPN. But America Movil now has said it will not abide by that agreement, clearing the way for either a larger investment in KPN, a bid to acquire all of KPN or even a sale of its stake, if America Movil is unable to dissuade KPN from selling its German assets.

It is not clear whether America Movil members of KPN’s board will vote to support the E-Plus sale. "We will evaluate the terms and conditions of the transaction," Daniel Hajj told analysts in a conference call to discuss America Movil's second-quarter results.

Should América Móvil want to block the sale of E-Plus in Germany to Telefónica, acquiring a majority in KPN may be its only option, though.

America Movil sees Telefonica as a primary competitor in American Movil’s core Latin American markets, and America Movil also has an investment of 29.8 percent in KPN, which owns E-Plus and wants to sell that asset to Telefonica.

Also, Telefonica had interest in buying KPN, or making an investment, on its own, prior to the America Movil move.

America Movil originally invested in KPN for the larger reason of diversifying outside Latin America. It might now see a tactical reason for trying to break up the Telefonica move by attempting to convince KPN to reverse the decision to sell the E-Plus stake.

No matter how the proposed acquisition of E-Plus is finally resolved, the move is the tip of the iceberg for further consolidation in the European mobile and broader telecom market.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Can Google Become a Force in Enterprise Computing?

Though Microsoft long has had a huge presence in business and enterprise computing environments, Apple, which traditionally has eschewed designing for business users, nevertheless has gained traction in enterprise computing environments. The big issue for Google is whether the Android ecosystem can become a significant provider in enterprise environments as well.

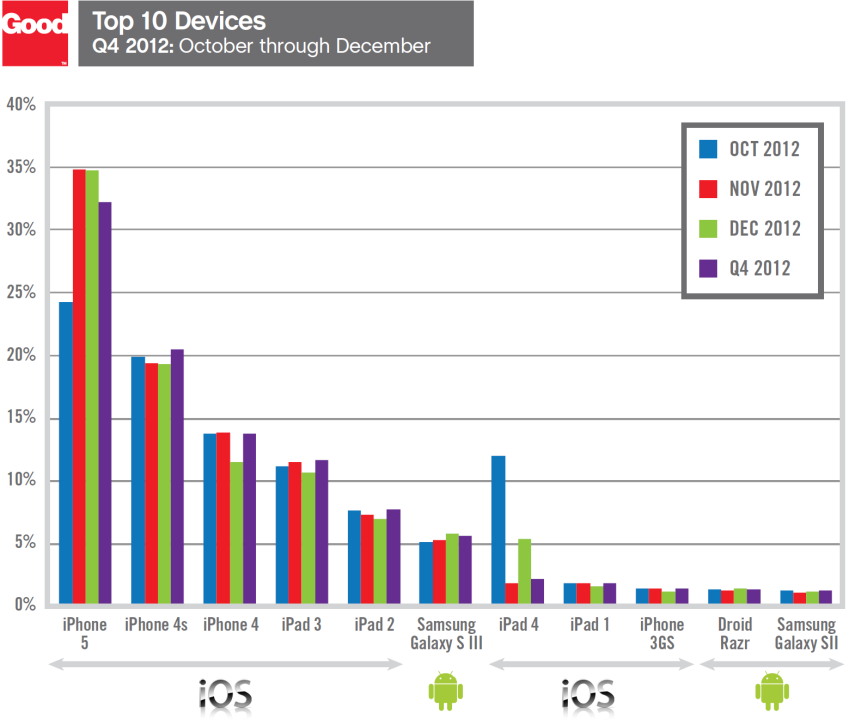

By most accounts, Apple is making the most gains in business user environments. A fourth quarter 2012 analysis by Good Technology shows the strides Apple has made in corporate environments.

Looking at new smart phone and tablet activations, Apple devices show the greatest share. Good Technology’s report showed a clear preference for iOS devices, which accounted for 77 percent of all activations and captured eight of the top ten spots on the most popular device list.

But Android activations accounted for 22.7 percent of all activations for the quarter, which were primarily driven by Android tablets. Windows Phone devices came in a distant third for the quarter, capturing just 0.5 percent of overall activations, Good Technology says.

That has some bearing on a larger question, namely whether Google is making inroads into the enterprise space, something it is attacking on an array of fronts, ranging from cloud computing infrastructure to productivity suites to devices and applications.

Consider one formerly overlooked approach, namely Chromebooks. Few would claim Google yet has gained significant traction for its Chromebooks in the personal computer market, much less enterprise environments. But some think that could change.

Infrastructure and operations professionals with responsibility for end user computing and device portfolios should look to Chromebooks in the enterprise environment, says J. P. Gownder, Forrester Research VP and principal analyst.

That is the recommendation even if Chromebooks cannot or will not displace most Windows PCs, Macs, and tablets used within enterprises. But for companies that are willing to segment their workforces (offering Chromebooks to specific classes of workers in a mixed environment with PCs and tablets), or adopting Gmail or Google Apps, or who are deploying the devices in a customer-facing (think kiosk) scenario, Chromebooks are “definitely worth investigating,” says Gownder.

Chromebooks offer the prospect of radically reducing the amount of time IT staff spends “keeping the lights on” for devices, Gownder says. Chromebooks might also in many cases get enterprises out of much of the overhead of supporting notebooks.

“I want to get out of the laptop business,” one CIO told Gownder. Chromebooks offer high uptime, low service costs, and scalable deployment of new web-based applications and content, Gownder says.

A move to corporate Gmail remains pretty much a prerequisite to the adoption of Chromebooks, Gownder also notes, however.

Some might argue Chromebooks are a tool for enterprise collaboration. One CIO told Gownder that workers at his company started to use Google Drive and other collaboration tools “organically and automatically” after the adoption of Gmail. So Chromebooks are a p[altform for collaboration.

“t’s time to take the Google enterprise proposition seriously,” Gownder says.

This

This Android is making gains in the overall market, to be sure. And since enteprise computing these days increasingly is affected by consumer computing, that will matter.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

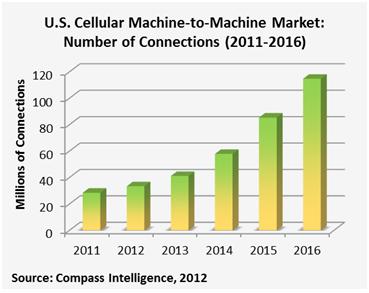

460 Million M2M Connections by 2018?

Mobile machine to machine (M2M) connections are set to reach over 450 million by 2018, according to ABI Research. That likely will be important for mobile service providers anxious to drive revenue and connection growth once sales to people saturates.

Other analysts have M2M forecasts in the same general range. Juniper Research, for example, a year ago forecast 400 million M2M connections in service by about 2017.

In the United States, The mobile M2M market will reach 114.7 million connections by 2016 with a compound annual growth rate of over 36 percent.

The largest business-to-business vertical market (most of the revenue likely will be B2B, some would argue) is the transportation vertical, with over 40 percent market share.

By 2015 more than 40 percent of M2M connections in the United States could be running on 3G, 3.5G or 4G networks. That also suggests that much of the demand for M2M connections will not rely much bandwidth, as 60 percent of M2M connections will use 2G networks.

Europe dragged down worldwide connection growth in 2011 and 2012, but connection growth will accelerate to a CAGR of 26 percent through 2018, ABI Research forecasts.

M2M average revenue per user connection ARPUs frequently are much lower than for human communications accounts, and ABI Research says competition is putting even more pressure on ARPU.

As do other analysts, ABI Research notes the importance of relatively bandwidth-limited 2G network connections. Some 70 percent of mobile M2M connections were on 2G networks in 2012, ABI Research estimates.

ABI Research also suggests that the cost of M2M transponders is one reason for the heavier reliance on 2G networks, even though it also is true many M2M apps do not require lots of bandwidth.

In fact, the firm argues 3G transponders are more than twice as expensive as 2G transponders, while 4G transponders are six times more expensive than 2G versions.

As with many other communication services, much of the potential revenue will be earned by providers of apps and services other than the basic connections.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Subscribe to:

Posts (Atom)

CIOs Believe AI Investments Won't Generate ROI for 2 to 3 Years

According to Lenovo's third annual study of global CIOs surveyed 750 leaders across 10 global markets, CIOs do not expect to see clear a...

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

Who gets to use spectrum, and concerns about interference from other users, now appears to be an issue for Google’s Project Loon in India. ...