Some believe hybrid fiber coax networks will not be able to deliver gigabit speeds, or even 100 Mbps, symmetrically.

Others might argue those claims are correct, in one sense: since HFC networks are designed to be asymmetrical, even at bandwidths that do hit a gigabit per customer location, HFC does not deliver bandwidth symmetrically.

Some might argue that is not the point. The claims about symmetrical bandwidth are largely correct, but irrelevant. After all, the claim of technological superiority of fiber to the home has been made for three decades, going on four decades.

But that is not the point. The point is which platform helps an ISP best match the twin goals of being the low cost provider of the services customers want to buy, with suitable profit margins.

The fundamental test is going to be whether HFC, fiber to the home or some other platform, in the relevant time period (a decade or more) best matches market cost, revenue and performance requirements.

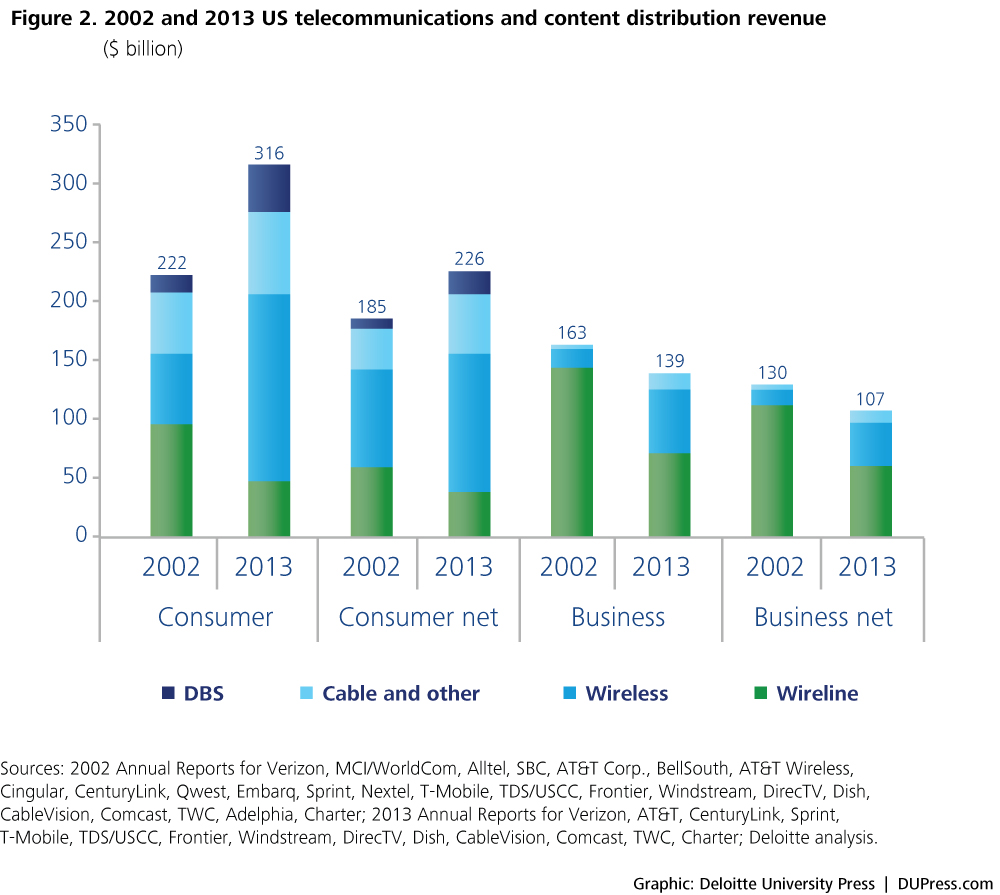

In markets where HFC is widespread, such as the United States, the formal technological superiority of fiber to the home has not clearly helped most of its practitioners to dominate the supposedly inferior HFC platform in terms of market share or profitability.

So far, as a business platform, HFC has more than held its own. In fact, as Comcast is the largest U.S. Internet service provider, and since cable TV has the largest market share in most local markets, with the overwhelming majority of net new additions, the technical merits of the platform--however one wishes to evaluate them--do not seem to matter.

What has mattered is the ability to translate platform features into revenue, market share and profit. On that score, cable has outperformed nearly all telcos.

The new wrinkle, as fiber to home physical media costs have declined, is whether new providers, with different cost structures or business models, can use FTTH to support their business models, typically based solely on selling Internet access; sometimes Internet access and entertainment video, and sometimes a triple play.

That applies to Google Fiber and the dozens of gigabit fiber operations springing up around the United States, for example.

The cost of physical media and construction are important parts of a cost model. But, so far, physical media cost arguably has not determined business success.