It has been the case for a decade that access provider executives believe they compete with Google even more than with other service providers, as a 2011 survey of telco executives found.

That thesis will be tested as the U.S. Department of Justice evaluates the AT&T acquisition of

Time Warner. Not only is the acquisition a vertical merger, but the larger marketplace battle is between firms such as AT&T and application providers.

Time Warner. Not only is the acquisition a vertical merger, but the larger marketplace battle is between firms such as AT&T and application providers.

One argument AT&T makes is that the video entertainment business now operates

globally. Where Netflix has 100 million accounts globally, AT&T might have about 24.4 million U.S. subscribers and about 12.45 million video subs in Latin America.

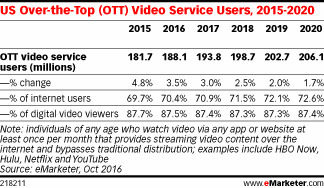

Beyond that, the linear video business is shrinking, replaced by growing over the top alternatives. There already are about 194 million over the top video subscriptions in service in the U.S. market.

The point is that consumer markets are changing fast, with new internet-delivered products displacing traditional linear TV.

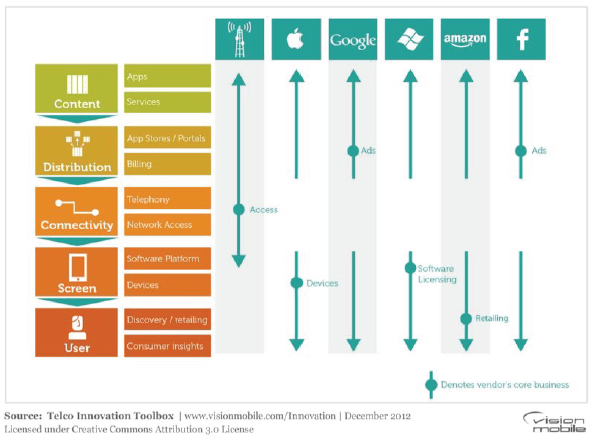

Though most of the competition involves product substitution--over the top displacing carrier services--Google has become an actual internet service provider and mobile services provider.

The big change, though, is the shift in value from vertically-integrated carrier services--voice, messaging, linear video--to over the top applications that work on any access connection.

The business implications are stark: access providers increasingly become “dumb pipes” offering lowish value, where differentiation is quite difficult, unless mobile carrier access can be recrafted as an application platform. That is easy to say, hard to achieve.

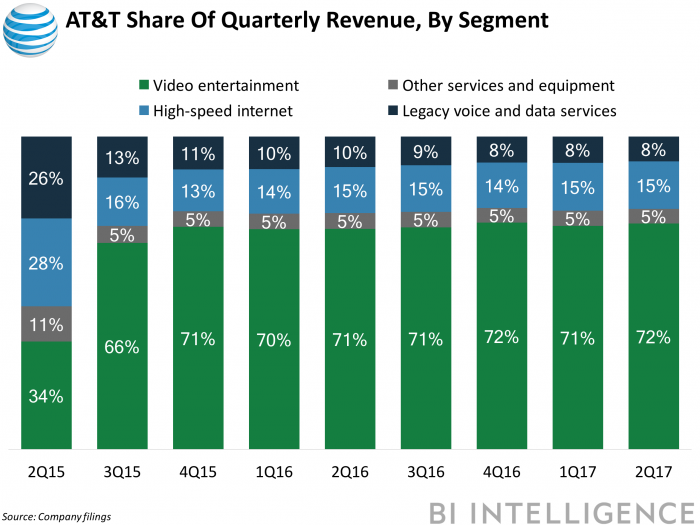

That shift is illustrated by revenue composition at AT&T’s landline business, where it comes to consumer revenue. About 72 percent of that revenue now is earned supplying video entertainment (an app), just about 15 percent selling internet access (the “dumb pipe”).