“Cutting out the middle man” (telcos) now has emerged as a key constraint on global telecom service provider revenues and profits, and will be a huge force dictating when and how the public networks industry actually will shrink.

Some forecasters already believe the global industry is going to shrink in 2018. Peak telecom, in other words, might be at hand, the point at which the global industry, after generally growing for 150 years, starts to shrink.

“Telecommunications firms are no longer the primary interests driving submarine cable construction,” says Jim Poole, Equinix VP. “Now, it’s hyperscale cloud companies and large content providers.”

That shift by enterprises--who now own and operate their own private networks--is an example of disintermediation. So are all “over the top” apps. And you therefore see the stunning implications of the concept.

Telecommunications has been a necessary function, and it also has fueled the growth of a global industry. In the new world, communications remains an essential function, but it is not always the driver of the public networks industry.

There are some parts of the telecom ecosystem for which this shift is not a problem. If you build subsea networks, cable and optoelectronics and do construction, you do not really care who the buyer is, so long as there are lots of them.

If you operate global data centers, and your customers are enterprises and private firms, you probably do not worry about the dwindling of the public communication networks business.

But if your business is selling communication services to businesses and consumers, disintermediation means your business is shrinking.

Disintermediation means the “reduction in the use of intermediaries between producers and consumers.” In other words, cutting out the middleman, and going direct to one’s customers, without the use of other distribution channels.

So one big impact of huge content and app firms building and operating their own networks is that the size of the public communications market is reduced. In other words, a growing percentage of international bandwidth no longer moves over public networks, supplied by public carriers (telcos or capacity specialists).

Depending on the route, private bandwidth supply represents as much as 30 percent to 70 percent of total traffic on those routes.

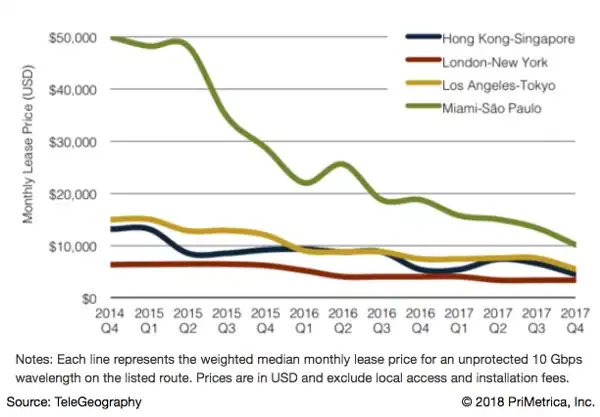

The other impact is falling prices. With some exceptions, bandwidth prices on undersea routes have fallen steadily, but not precipitously, over the last decade or so.

One issue, as noted, is that traffic now is shifting to private networks owned and operated directly by content companies, app companies and other enterprises, who no longer need to buy such long-haul capacity from commercial providers. That means fewer potential customers, and therefore more competition to secure what remains of demand for public network services.

Moore’s Law is another issue, as ever-cheaper bandwidth is possible, and therefore reflected in retail prices (more supply means lower prices).

Annual global operator-billed revenues from voice and data services will fall by over $50 billion (about six percent) over the next five years, from $837 billion in 2017 to $785 billion in 2022, according to Juniper Research.

On a global basis, the dollar value of operator-billed monthly average revenue per user fell by 62 percent between 2005 and 2017, to $9.20, Juniper Research estimates.

That decline is structural, and not caused by temporary issues such as economic slowdown.

That really should come as no surprise. Every telecom product has a product life cycle. Eventually, every potential prospect already has become a customer. Product substitution is happening, there is substantial new competition and mobile adoption in developing countries, which has driven global growth for more than a decade, is slowing.

In 2013, the dollar value of global operator-billed revenues fell for the first time.

In both West Europe and Central & East Europe, the dollar value of revenues peaked in 2008.

In 2017, three regions (Latin America, Central & East Europe and rest of Asia Pacific) saw year-over-year growth, but revenues were below peak levels, Juniper Research argues.

In 2017, operator-billed revenues had fallen to 86 percent of their 2013 peak levels; in West Europe, revenues are now just 58 percent of their 2008 high point.

New revenue sources such as internet of things apps and connectivity will help, but will not replace the lost voice and internet access revenues. Internet of Things revenues might generate some $8 billion by 2022.