Bruce Henderson, founder of the Boston Consulting Group is credited with a couple of foundational ideas about business, including the notion of the experience curve, which explains how the cost of products decreases with volume.

“Costs characteristically decline by 20 percent to 30 percent in real terms each time accumulated experience doubles," Henderson posited in 1968.

Among the ideas some may deem most important relates to market structure under conditions of competition.

"A stable competitive market never has more than three significant competitors, the largest of which has no more than four times the market share of the smallest,” Henderson argued.

Sometimes known as “the rule of three,” he argued that stable and competitive industries will have no more than three significant competitors, with market share ratios around 4:2:1.

There are important implications. We may decry “bigness.” We may prefer that a plethora of firms exist. But the rule of three suggests a robustly competitive market will, over time, assume a stable form where three firms dominate, with market shares have a specific structure.

To wit, the leader will have market share double that of company number two, while company number two has twice the market share of the third firm. Empirical studies tend to confirm the pattern.

In most markets, argue Bain consultants, two firms have 80 percent of the profit. In other words, market share also often is a proxy for profitability. “On average, 80 percent of the economic profit pool was concentrated in the hands of just one or two players in each market,” say Bain and Company consultants. In other words, it really matters if a firm is number three in any market.

That virtually perfectly corresponds to a market share pattern of 4:2:1, as the number-three provider tends to have less than 10 percent share, in that pattern.

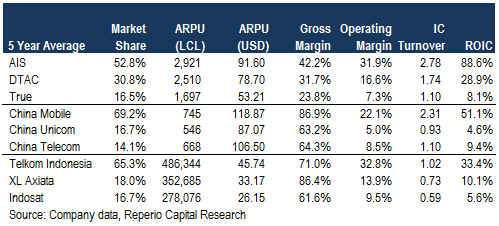

One sees this pattern in some telecom markets. Looking at market share and return on invested capital for the three largest telecom providers in Thailand, China, and Indonesia since 2015, you can see that financial return and market share tend to be directly related.

The real-world structure does not precisely match the rule of three prediction, of course, with Thailand having the almost-perfect correspondence between predicted results and actual results.

In many other markets, two observations are apt: where the 4:2:1 pattern does not exist, markets either are not competitive, or not stable, or both. And though we might be tempted to think such patterns exist mostly for capital-intensive industries, the pattern seems to hold in most industries.

Source: Reperio Capital

My rule of thumb incorporating the “rule of three” is that the leader has twice the share of number two, which in turn has twice the share of provider number three. In Thailand, China and Indonesia, the general pattern holds.

In Thailand the pattern holds well. The leader has 53 percent share, number two has 31 percent and number three has 17 percent share.

Applying the rule of three in consumer telecom markets is complicated, however, since the “markets” include segments such as video entertainment, internet access, voice and mobility where specific players have distinct market share profiles.

The broad conclusion is that telecom markets are not yet stable.