National telecom infrastructure policy in big countries is an example of turning a huge ship in a new direction: it takes time. Consider Australia’s NBN. Over the last decade the national broadband network--designed as a single wholesale network--has faced acrimony, slower than expected build rates and potential policy reversals.

Only now there are moves toward facilities-based competition that tend to raise the question of whether the plan to build a wholesale network was the right choice.

On the face of it, the NBN’s new plan to lower prices for business customer connections in suburban areas is a simple reflection of growing competition from facilities-based firms.

The move likely is a response to growing facilities-based competition, from municipal broadband to 5G offers from Telstra. After a seemingly endless struggle to get the NBN designed, funded and built, at least some officials believe facilities-based competition should be reintroduced.

Traditionally, wholesale facilities have made sense where there is no easy way to enable rival physical networks, for whatever reason. Under such circumstances, regulators often have opted for one physical network that sells wholesale service to any telecom services retailer.

The stated advantages include lower overall capital investment and possibly faster time to deployment. The downside, some of us would note, is a loss of innovation and differentiation possible when different facilities-based networks compete with each other.

Perhaps the best examples so far are the role of cable operators in the broadband business. In the U.S. market, for example, cable operators have 70 percent of the installed base and get virtually all the new net additions in the fixed network broadband business, and have done so for years.

Possibly the next examples are entry by mobile operators, in the 5G era, into the home broadband business, using fixed wireless for higher-bandwidth use cases but even standard 5G for many users.

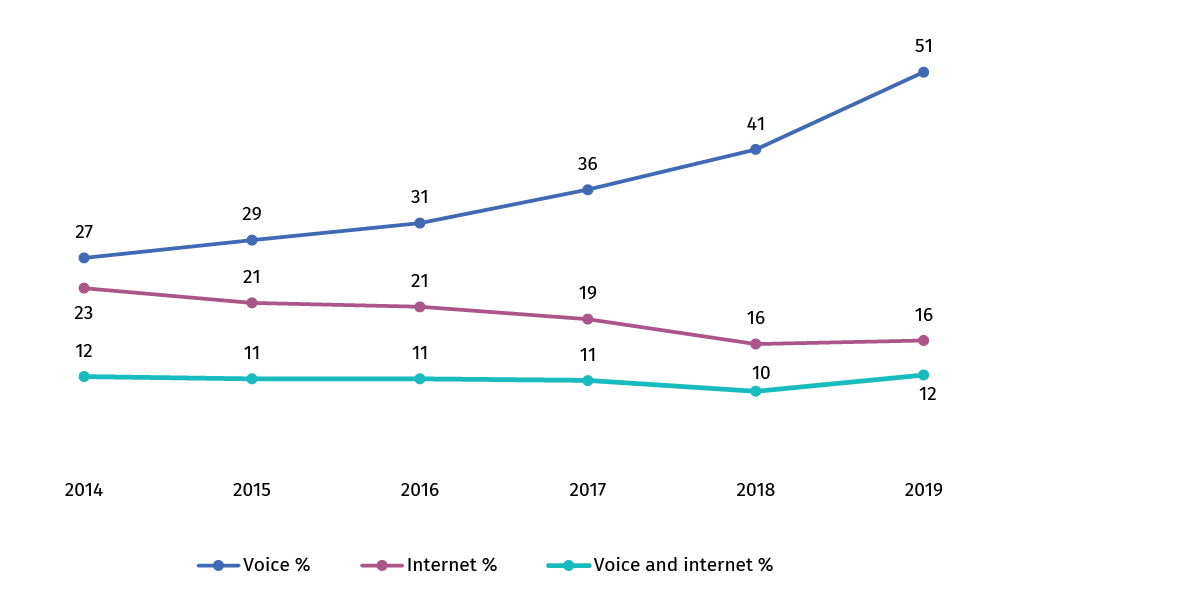

In 2019, about 19 percent of customers were mobile-only for internet access, for example, according to the Australian Communications and Media Authority. That percentage is expected, in some quarters, to increase over time as 5G and following mobile networks increasingly are able to supply bandwidth enough to substitute for a fixed connection in a growing number of use cases.

As part of the new plan, NBN says it will invest up to $700 million to create up to 240 NBN Business Fiber Zones across Australia, in 85 regional areas. The effort includes financial incentives for its retail partners, in the form of waiving the typical charges to build out an access lateral.

NBN says that all businesses within these zones will have access to Enterprise Ethernet, at significantly reduced wholesale prices. In total, these zones are expected to cover more than 700,000 businesses, NBN says.

Businesses in Business Fiber Zones also will see Enterprise Ethernet pricing reduced, some by up to 67 percent.

Enterprise Ethernet is NBN’s fastest symmetrical wholesale product and premium-grade business offering. It has options for prioritised traffic, high capacity and symmetrical upload and download wholesale speeds from 10Mbps to close to 1Gbps.

NBN also says that when an internet retailer places an order for Enterprise Ethernet, for an estimated 90 per cent of business premises in the national NBN network footprint, NBN will not charge the retailer for building the connection to the customer, it seems.

If an internet retailer signs up for a three-year Enterprise Ethernet plan, NBN will not charge the retailer an up-front connection cost.