To the extent that faster home broadband speed tiers cost more, there is a clear and compelling argument to be made that fixed network providers can increase average revenue per account as customers migrate to higher-priced tiers of service.

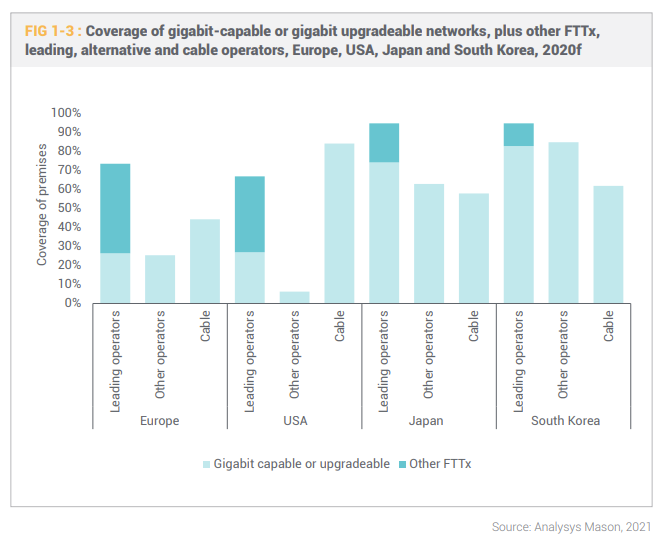

Also, we might be on the cusp of a bigger opportunity for telco gigabit services, as history suggests take rates for gigabit services has reached an inflection point.

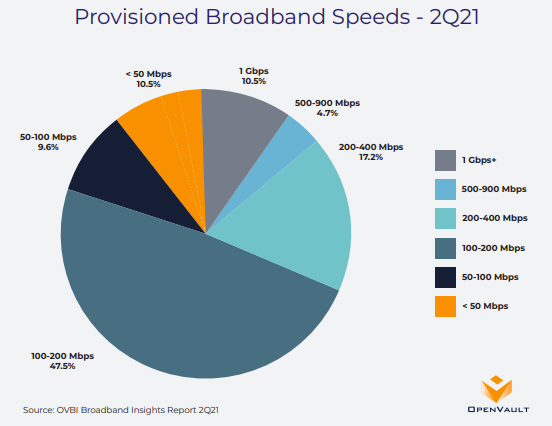

Historically, popular consumer products accelerate after adoption reaches the 10-percent of homes level, and gigabit internet access now has reached that point.

Openvault data shows that consumers are migrating to speed tiers faster than 100 Mbps.

At the same time, markets for 4G fixed wireless are likely to be centered on rural areas, as urban customers move to services operating faster than 100 Mbps. 5G fixed wireless might be competitive for significant percentages of urban market customers. In fact, 5G fixed wireless offering speeds between 100 Mbps and 200 Mbps might appeal to nearly half the market.

It is hard to quantify demand for symmetrical services. It seems clear that services with faster upstream speeds, such as telco fiber to home services, could be the near-term winners in that regard.