It is no secret that mobile broadband features now drive mobile service provider revenue growth in developed economies.

It is no secret that mobile broadband features now drive mobile service provider revenue growth in developed economies.

And even if sheer growth of subscribers continues to drive growth in developing markets, revenue from Internet access is becoming more crucial there as well.

Global mobile broadband subscriptions are predicted to grow 400 percent by 2019, reaching eight billion accounts, up from about two billion in service in 2013, according to Ericsson.

While mobile subscriptions globally grew seven percent, year over year, in the third quarter of 2013, mobile broadband subscriptions grew at a rate of 40 percent year over year.

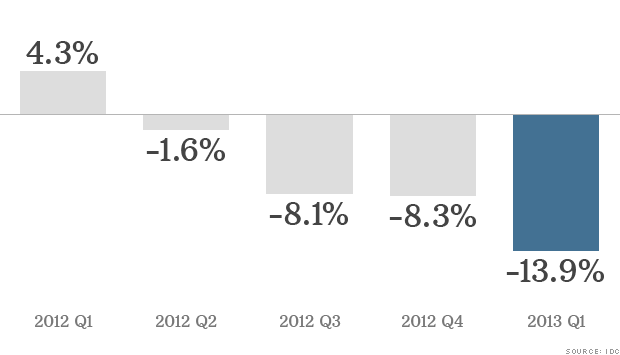

That trend is fueled by a changing mix of device sales. About 55 percent of all mobile phones sold in the quarter were smart phones, according to the Ericsson Mobility Report. And that in turn drives demand for mobile Internet access.

As a result, mobile data traffic is expected to grow at a compound annual growth rate of around 45 percent (2013-2019). This will result in an increase of around 10 times by the end of 2019.

The number of mobile subscriptions for mobile PCs, tablets and mobile routers is expected to grow from 300 million in 2013 to around 800 million in 2019, as well.

Between 2013 and 2019, mobile data traffic will grow seven times in North America, 11 times in Latin America, nine times in Western Europe, 11 times in Central Europe and Middle East and Africa, as well as in the Asia Pacific region.

Fixed data traffic will grow about 25 percent between 2013 and 2019, on a compound annual growth rate basis, and will remain the dominant way most data is transferred to end users.

Mobile data traffic represents five percent of total Internet end user traffic in 2013, and will grow to 12 percent in 2019.

That, one might suggest, shows the long term value of fixed network access, which will continue to account for most of the total volume of access traffic.

The largest and fastest growing mobile data traffic segment is video, as you have come to expect, expected to increase by around 55 percent annually up until the end of 2019, by which point it is forecasted to account for more than 50 percent of global mobile traffic.

Use of streaming on-demand and time-shifted content, including YouTube, is ubiquitous.

About 41 percent of people aged between 65 and 69 stream video content over mobile and fixed networks on at least a weekly basis, the Ericsson Mobility Report says.

By the end of 2019, total mobile subscriptions will reach around 9.3 billion.

Total global mobile subscriptions, including subscriber information modules and full prepaid or postpaid accounts, numbered 6.6 billion in the third quarter of 2013.

By 2019, almost all handsets in Western Europe and North America will be smart phones, compared to 50 percent of handset subscriptions in the Middle East and Africa.

Mobile phones account for around 50 percent of total mobile data traffic volume in the measured networks. In many European networks, mobile PCs represent 10 percent to 30 percent of the

subscription base and generate 50 percent to 80 percent of the traffic.

In contrast, North America is typically dominated by smart phone traffic, with mobile

PC subscriptions only representing a small share of traffic. Fixed network access, using routers ranges between usage of 1 GB to 42 GB each month.

Mobile PCs represent usage of 0.5 GB to 8 GB while tablets represent monthly usage between 150 MB and 2,200 MB. The largest average traffic volumes for smart phones were measured on Android devices, using up to an average of 2.2 GB per month.