“Screens” are important to Internet service providers, telcos, cable TV companies and satellite video and Internet providers for one simple reason: ownership and use of various screens is a precondition for service demand.

For decades, the primary screen used by most consumers was the television. Then followed the PC, then the mobile phone, MP-3 player and now the tablet. Whole industries, ranging from broadcast TV and cable TV to DVD rentals and sales and the Web were created by use of those screens.

So changes in device preferences should shape demand for services provided to those devices.

And though the data remains fragmentary, it appears younger consumers see less need to own and use desktop or notebook PCs and televisions, and more often substitute a mobile device for both TVs and PCs.

Nearly half of all people 18 to 34 in the United Kingdom, for example, consider mobile a more important screen than television for media consumption, a study by Weve has found.

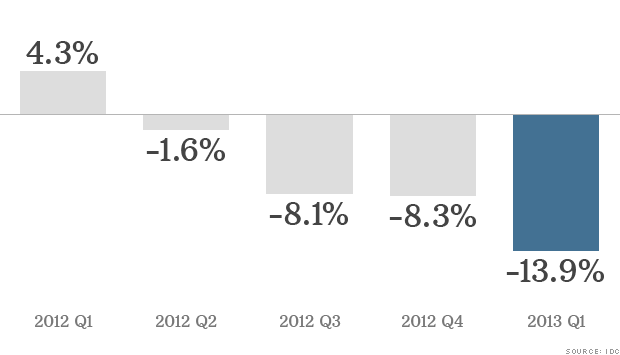

Separately, Gartner estimates PC shipments in Western Europe declined 12.8 percent from the same period in 2012. PC sales have been dropping since at least 2011.

"The PC market in Western Europe continued to shrink, declining faster than expected," said Meike Escherich, principal research analyst at Gartner. To be sure, demand has shifted to tablets, so even if mobile and desktop PC shipments declined by 14.5 percent and 9.8 percent, respectively, users can use tablets as functional substitutes.

Those trends bear watching. If people don’t own and use TVs, they don’t need a video subscription service aimed at TVs. If people don’t own and use PCs and the Internet, they will have no need for Internet access. If people do not want to use landline phones, they don’t need landline phone service.

On the other hand, demand could be shaped in new ways. In the past the primary reason for buying Internet access was access to email (dial-up era) and in the broadband era has morphed into access to the Web.

In the future there could be multiple reasons for buying Internet access, ranging from offload of mobile device data usage to the fixed connection, support of in-home Wi-Fi for tablets and PCs, as well as video consumption on all devices, including TVs.

Historically, device penetration created a ceiling for service adoption. In any given market, if 15 percent of households find no reason to use the Internet or PCs, those households are not going to be prospects for buying Internet access.

Roughly the same argument applies to ownership of televisions, with the caveat that televisions can be used without video subscriptions, as displays for non-connected game players, DVD and Blu-ray devices.

What is new is that widespread use of a variety of connected devices changes the demand driver for Internet access, even if use of some dedicated (TV) or general purpose (PC) devices is lessening, to some extent, in some demographic groups.

What is new is that widespread use of a variety of connected devices changes the demand driver for Internet access, even if use of some dedicated (TV) or general purpose (PC) devices is lessening, to some extent, in some demographic groups.

One wild card is the suitability of mobile and fixed networks to support the range of devices and use cases many users will have.

The data also suggests mobile devices now are firmly established as competitors to conventional media channels in the United Kingdom, Weve argues. Assuming people prefer to use their mobiles as content consumption devices on the Wi-Fi connection, rather than the mobile network, while in the home,

When including screens used for work or personal purposes, 40 percent of respondents surveyed consider the PC the most important screen, especially for work activity,

But 28 percent of respondents say that mobile devices are now their first screen for media consumption, ahead of TV at 27 percent.

And demographics matter, as 46 percent of respondents 18 to 34 year consider their mobile device as their first and most important screen.

Over a quarter of surveyed consumers turn to their mobile first to interact with online content, rising to 45 percent among 18-34 year olds.

Nearly 10 percent of consumers turn to their mobile first to make online purchases.

The nationwide survey of 2,000 adults between the ages of 18 and 55 (or older) found that

about 39 percent say their mobile device is the screen they look at most often.

One might argue those findings could have implications beyond the advertising and media business, and affect fortunes for video entertainment providers.

Many would note that rates of television ownership among Millennials are lower than might have been expected in past decades, mirroring a trend to rent rather than own homes and cars.

Nielsen found in 2011 that U.S. television ownership actually dropped for the first time.

That is a break from past behavior, as in 2010, Nielsen estimated the typical U.S. home owned more than two TV sets each.

One might argue, impressionistically, that younger people view televisions as quite optional, when forming their own households.

One might argue, impressionistically, that younger people view televisions as quite optional, when forming their own households.

Though lack of income is an issue for some, quite often, even consumers who can afford to own televisions simply do not buy them, getting most of their video from streaming sites, viewed on tablets, PCs and phones.

Ironically, less demand for some devices might change consumption in ways that create new use cases for service provider products.

Traditional video subscription services might be supplanted, eventually, by streaming alternatives that make the Internet access connection more valuable, while devaluing the legacy service.

In some other cases, a mobile connection might supplant the fixed connection.

But all the trends mean that the historic market ceiling for PC-based Internet access, or the historic floor for video subscriptions, potentially are changing. Increasingly, even households that do not use “the Internet” might discover broadband access is useful to support their mobile device usage, supply TV and voice services.

Put simply, the way Internet access in any market potentially grows to 100 percent is not “use of PCs” or “use of the Internet” but any of those apps, plus “use of mobile phones,” “use of tablets” or “want to watch TV.”

No comments:

Post a Comment