PC shipments worldwide, expected to grow 4.4 percent in 2012, will grow 10 percent in 2013, according to Gartner. That is a bit of a surprise, with all the attention now focused on tablet sales.

In the first quarter of 2012, PC shipments climbed nearly two percent to 89 million units, thogh analysts had predicted a 1.2 percent drop. Those figures might suggest that tablets and PCs now are distinct products in the marketplace. Though substitution will occur in some cases, much as smart phones displace PCs in some cases, all the products will develop specific niches in the computing appliance market, one might argue.

Apple's iOS continues to be the dominant media tablet operating system, as it is projected to account for 61.4 percent of worldwide media tablet sales to end users in 2012, with Android-powered units representing about 32 percent of sales, Gartner says. By 2016, some 369 million tablets will be sold, Gartner estimates.

By way of contrast, IDC predicts that PC shipments will climb from 353.3 million to more than 500 million in 2016. However, the bulk of the growth will come from "emerging markets" not "mature markets", and from portable PCs rather than desktops, IDC forecasts.

In fact, IDC predicts that shipments of portable PCs in "emerging markets" will almost double from 110.0 million in 2011 to 214.7 million in 2016.

One might therefore infer that tablets will represent about 25 percent of “PC” sales in 2012. By 2016, one might argue, tablets will represent 42 percent of “PC” sales.

"Despite PC vendors and phone manufacturers wanting a piece of the pie and launching themselves into the media tablet market, so far, we have seen very limited success outside of Apple with its iPad," said Carolina Milanesi, research vice president at Gartner.

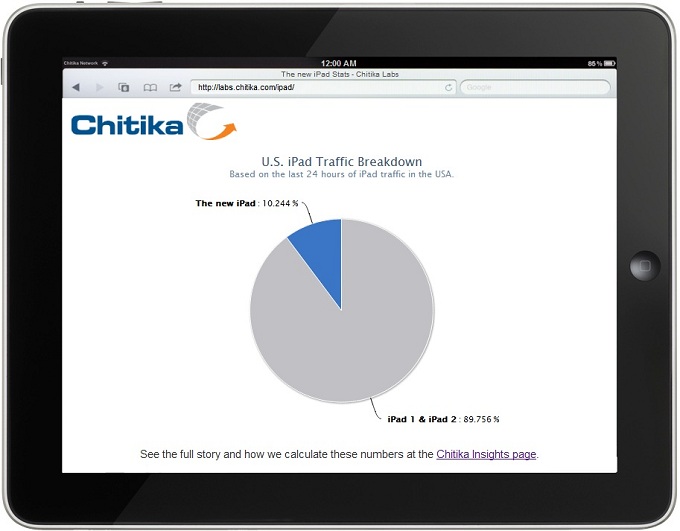

"As vendors struggled to compete on price and differentiate enough on either the hardware or ecosystem, inventories were built and only 60 million units actually reached the hands of consumers across the world. The situation has not improved in early 2012, when the arrival of the new iPad has reset the benchmark for the product to beat."

Global Tablet Sales to End Users (Thousands of Units)

| OS |

2011

|

2012

|

2013

|

2016

|

| iOS |

39,998

|

72,988

|

99,553

|

169,652

|

| Android |

17,292

|

37,878

|

61,684

|

137,657

|

| Microsoft |

0

|

4,863

|

14,547

|

43,648

|

| QNX |

807

|

2,643

|

6,036

|

17,836

|

| Other Operating Systems |

1,919

|

510

|

637

|

464

|

| Total Market |

60,017

|

118,883

|

182,457

|

369,258

|