Though the roster of contestants within any industry changes over time, few entire industries actually disappear.

Much depends on how one defines "industry." One might argue that the computing industry has gotten bigger over time, even though the "mainframe," minicomputer" and now "personal computer" segments have declined.

One might ask the same about the telecommunications industry.

In some ways, the question seems odd.

Over nearly every time period, global telecom revenue grows. The only possible exceptions were the years 1929 and 2001, but even there the dips were relatively slight.

For that reason, many consider telecommunications “recession proof,” a theory that was tested in 2000 and 2008. For the most part, aggregate revenue remained fairly stable, though there were some changes in composition of revenues.

And that generally remains the present revenue trend, where annual revenue, on a global basis, grows about 2.7 percent.

That, however, is a secular trend that was in place before the recessions, so the actual impact of specific recession-induced changes is hard to measure.

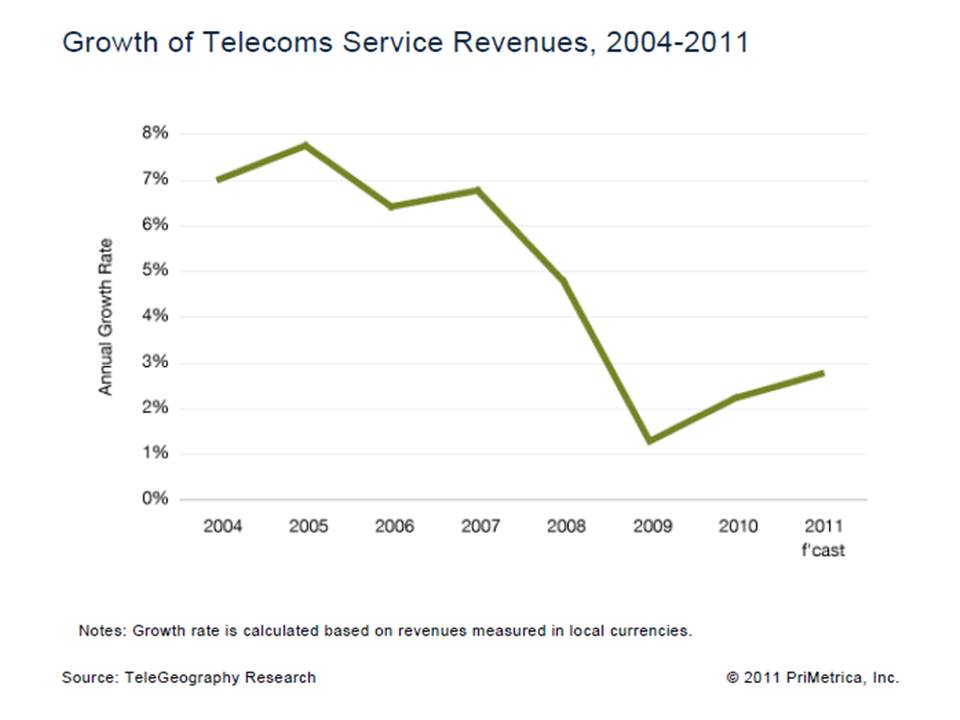

So while revenue growth might slow, the 2008 global recession did not halt revenue growth. The impact of the Great Recession beginning in 2008 is easy enough to describe. According to TeleGeography Research, revenue growth slipped from about seven percent annually to one percent in 2009, returning to about three percent globally in 2011.

To be sure, growth prospects vary between regions. In fact, growth in Western Europe has gone negative, perhaps the first time in history that communications revenue actually has seen a declining trend.

To be sure, growth prospects vary between regions. In fact, growth in Western Europe has gone negative, perhaps the first time in history that communications revenue actually has seen a declining trend.

The point is that any particular telecom product or service has a life cycle. The bigger question is whether telecommunications, as an industry, also has a life cycle. That does not necessarily require that people “stop communicating.”

The issue is whether the presently-constituted communications industry represents the way people do those things, in the future, or to the same magnitude.

Glimmers can be seen in the role cable TV companies now have assumed in the communications business.

Whether “communications revenue” earned by the cable TV industry has shifted to “another industry,” or whether cable TV providers simply have become part of the communications industry, is a judgment call.

From a telecom service provider’s perspective, it does not really matter how one classifies the revenue and market share. Telecom providers have lost revenue and market share to new providers, across the consumer and business segments, and across the voice and data services markets.

To be sure, telcos have compensated by earning new video entertainment revenues and by making the formerly distinct “mobile communications” business a core part of the telecommunications business.

So the question of industry life cycle is no mere speculation. Can a telco go bankrupt? A few already have, though so far no former incumbent telco has literally disappeared altogether.

But it remains an open question, albeit not a major issue, whether the way communications services and access will be provided exclusively by today’s telcos, cable TV companies and other access providers in the future.

Google Fiber poses the challenge in somewhat concrete terms. Again, one can argue that revenues earned by Google Fiber are simply “communications revenues” earned by a new provider in the traditional business.

Google Fiber poses the challenge in somewhat concrete terms. Again, one can argue that revenues earned by Google Fiber are simply “communications revenues” earned by a new provider in the traditional business.

But one might also argue that Google Fiber might eventually be something else, namely part of a shift of the traditional access business to a new industry.

It’s a bit of a stretch to label Google Fiber access or video entertainment revenues as “application” revenues. Google’s advertising revenues generally are measured as a distinct business from that of communications access.

But the boundaries are getting porous, as Google manufactures and sells mobile devices and Internet access as supports for its application and ad revenues business.

The first prototype of a modular smart phone, likely including the exoskeleton and at least a few module variations that can be assembled to create a working smart phone with various features, is almost ready.

The first prototype of a modular smart phone, likely including the exoskeleton and at least a few module variations that can be assembled to create a working smart phone with various features, is almost ready.