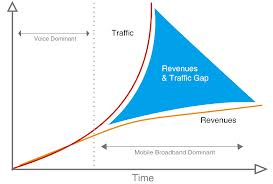

It is easy enough to explain why video entertainment consumption poses a huge--some would say nearly fatal--challenge to mobile operators: there if a fundamental mismatch between revenue and bandwidth required to deliver narrowband services (voice, messaging) and that required to support full-motion video.

Simply, revenue per bit for messaging and voice can be as much as two or more orders of magnitude higher than for full-motion video or Internet apps.

The revenue per bit problem is easy to describe. Assume a fixed network ISP sells a triple-play package for a $130 a month retail price, where each component--voice, Internet access and entertainment video--is priced equally (an implied price of $43 for each component).

How much bandwidth is required to earn those $43 revenue components? Almost too little to measure in the case of voice; gigabytes for Internet content consumption and possibly scores of gigabytes for video.

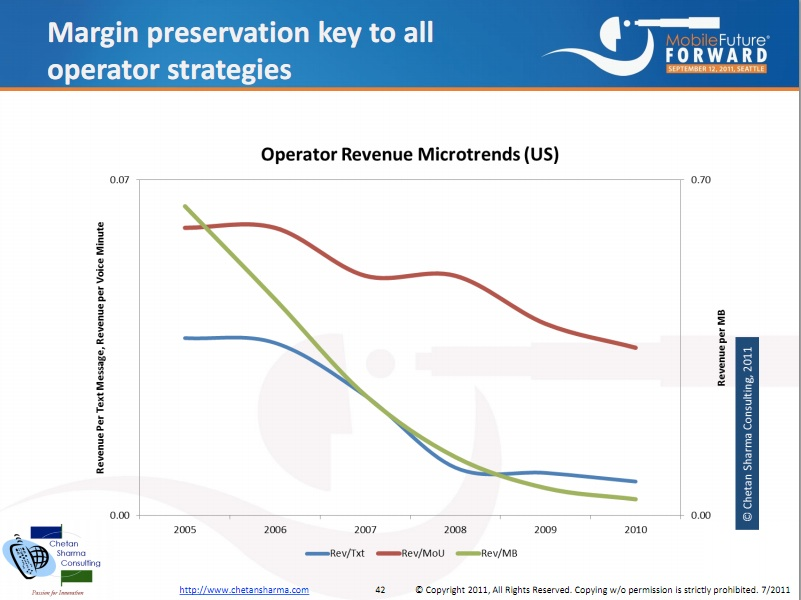

By some estimates, where voice might earn 35 cents per megabyte, revenue per Internet app might generate a few cents per megabyte. At one level, a network engineer might argue that such fine distinctions do not matter. The network has to be sized to handle the expected load.

McKinsey analysts have argued in the past that a 3G network costs about one U.S. cent per megabyte. The problem, in many developing markets, is that revenue could drop to as little as 0.2 cents to 0.4 cents per megabyte, for any mobile Internet usage.

That implies a strategic need to reduce mobile Internet costs to as little as 0.1 cent per megabyte, or an order of magnitude. Tellabs similarly has warned about revenues per bit dipping below cost per megabyte, leading to an "end of profit" for the mobile business.

Of course, all of that analysis occurred under conditions where it was web browsing that largely represented Internet bandwidth demand. Streaming video is another order of magnitude or two orders of magnitude sort of problem, though, in part because it is so hugely bandwidth intensive and because it will represent as much as 70 percent of all Internet bandwidth consumption, in a few short years.

Consider the wide variance in revenue per bit represented by a few different potential mobile Internet use cases.

One use case is a $20 a month smartphone data plan and 2GB of usage, representing retail revenue of $10 per gigabyte.

A Netflix subscription generates no direct revenue but could represent network consumption of between a few gigabytes and 30GB of traffic, if usage approaches fixed network levels. Revenue arguably is zero dollars per gigabyte.

A Netflix subscription generates no direct revenue but could represent network consumption of between a few gigabytes and 30GB of traffic, if usage approaches fixed network levels. Revenue arguably is zero dollars per gigabyte.

A work environment might represent $100 a month revenue and consumption of between 10 GB and 50GB. So revenue might range between $2 to $10 per gigabyte.

And that’s the problem with video: much of it does not actually represent revenue for the ISP. But even if it does, what is the revenue and cost per gigabyte? Even if one assume use of one hour of standard definition video, and that product is owned by the ISP, revenue might be $1 to $2 per gigabyte.

Some would argue the cost per gigabyte for a mobile ISP is higher than that. And it is almost nonsensical to think that a standard linear video service, representing perhaps $40 to $80 a month of revenue, will fare well if viewing habits in the mobile realm are what they are in the fixed network realm, where it might not be uncommon to have a single device receiving content for four to six hours a day, representing consumption of perhaps 4 GB to 6 GB per device.

And that assumes only one user, or one stream, is in use. In a multi-user household, demand could be two to three times that amount. In that case, hundreds of gigabytes would be the account load for a single month.

That will destroy revenue per bit metrics, unless you believe consumers really will pay $200 to $400 a month--or more--in mobile Internet access charges, to say nothing of the actual retail price of the content service.

Marketers might argue that revenue per account is what matters, for a multi-product business. That is true, up to a point. An ISP might fare okay if providing a mix of products with disparate revenue per bit values.

Marketers might argue that revenue per account is what matters, for a multi-product business. That is true, up to a point. An ISP might fare okay if providing a mix of products with disparate revenue per bit values.

The revenue earned from text messaging is almost arbitrarily high, as SMS is a byproduct of using the signaling network. Voice revenue might be moderately high, if users can be coaxed or compelled into paying for access to the feature, rather than for usage.

Ericsson hs calculated the cost per bit for a mobile network at about one Euro per gigabyte. So total revenue per bit has to exceed that cost.

Heavy video consumption--especially of third party content-- is likely to exceed cost per bit under almost any scenario.