It is easy to overlook the huge change in mobile industry economics as video becomes the chief bandwidth generator on mobile networks. It is hard enough to maintain profit margins for a service created and sold by an access provider; harder still when an access provider does not derive any direct revenue at all from an application.

It is easy to overlook the huge change in mobile industry economics as video becomes the chief bandwidth generator on mobile networks. It is hard enough to maintain profit margins for a service created and sold by an access provider; harder still when an access provider does not derive any direct revenue at all from an application.

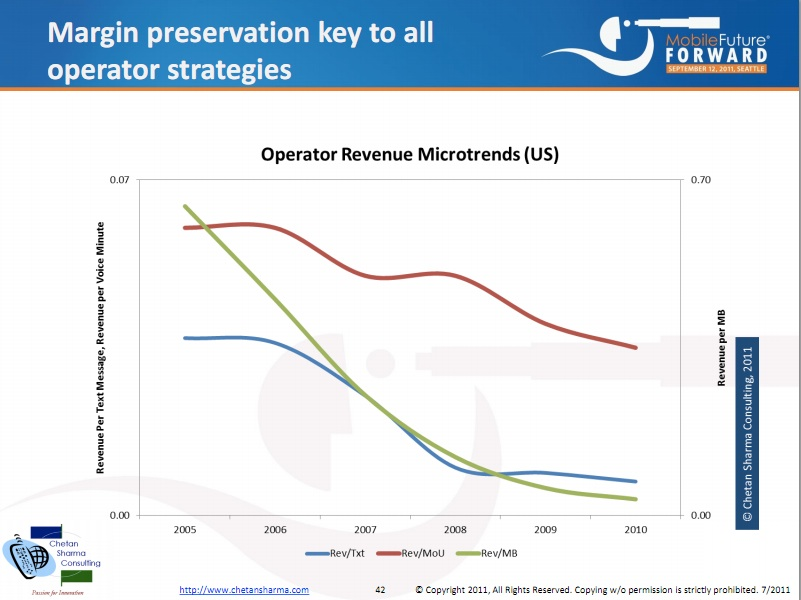

And that latter problem is precisely why over the top video poses such a challenge for mobile service providers. Even ignoring for the moment the lack of any direct revenue model for over the top video, revenue per bit always has been an issue for broadband services, compared to narrowband services.

In fact, even if mobile service providers might prefer to price according to value, that is difficult for video services, since the perceived price per bit for video is so low, relative to other types of apps.

To be sure, even some thoughtful analysts have been wrong about profit margins. Despite some claims to the contrary, mobile broadband service is profitable. Still, video poses a problem because it is so hugely different, in terms of bandwidth consumption, than any other media type.

Even though McKinsey analysts have argued in the past that a 3G network costs about one U.S. cent per megabyte, the growing problem is video consumption per megabyte, even when a service provider gets paid to provide it.

Consider over the top video, which might be supported by retail mobile Internet plans costing about $10 per gigabyte.

Assume a user is consuming an hour of Netflix, at “best quality,” representing about a gigabyte per hour, or perhaps 2.3 GB an hour. That earns $10 for supplying a gigabyte of usage.

Assume a user is consuming an hour of Netflix, at “best quality,” representing about a gigabyte per hour, or perhaps 2.3 GB an hour. That earns $10 for supplying a gigabyte of usage.

That, in itself, is not a problem, so long as users agree to pay for what they use. But that is the potential problem: it is unlikely users will continue to behave the same way as consumption grows.

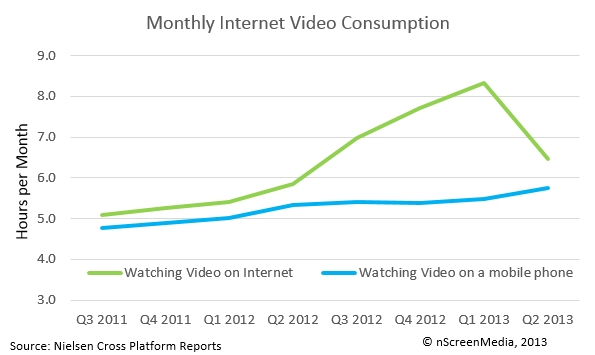

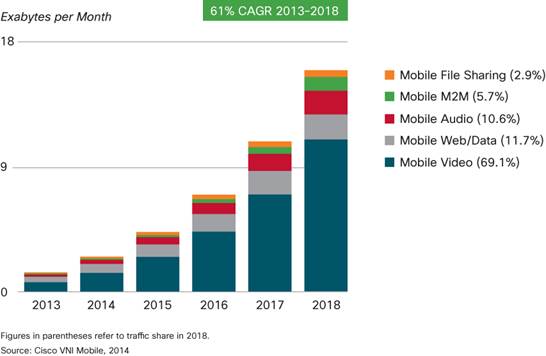

According to Ericsson, video traffic on mobile networks grows about 60 percent annually. According to Cisco, mobile video consumption is growing at a compound annual growth rate of 69 percent between 2013 and 2018.

Already on some networks, video consumption is on average 2.6 GB per user per month. At some point, most consumers will reach a point where they either stop consuming more, stop buying bigger plans, or both.

Of the 15.9 exabytes per month crossing the mobile network by 2018, 11 exabytes will be due to video, Cisco says. In 2012, mobile video represented more than half of global mobile data traffic, Cisco says.

Of the 15.9 exabytes per month crossing the mobile network by 2018, 11 exabytes will be due to video, Cisco says. In 2012, mobile video represented more than half of global mobile data traffic, Cisco says.

If mobile service providers become providers of mobile entertainment services, the basic problem remains. Assume a mobile service provider offers a Netflix style service, and earns $8 a month, while consumers watch five hours a month.

Total revenue might be as high as $58 a month, including the $8 video subscription fee, plus $50 in Internet access fees. The issue is where consumer resistance, or reduced app usage, or offloading, comes into play.

But assume people watch five hours each day of mobile video, the same amount U.S. residents watch. That implies as much as 150 hours of video a month, per subscriber. There simply is no way a subscriber pays $1500 a month in data charges, simply to watch video.

So the practical issue is how much any typical consumer will pay to watch video. And there the economics get tricky. A household of three, for example, might watch as much as 450 hours of video, if there is no shared viewing.

Assume a monthly video subscription price of $90 a month. That implies a cost of about 20 cents an hour. Mobile data charges are $10 per gigabyte, which is roughly an hour of viewing. The economics will break down quickly.

A mobile network designed to handle mostly video has to be designed and operated differently--and at far lower cost--than a network designed for narrowband services. That has been obvious for some time. It now will become a most-practical issue.

Without dramatic cost reductions, video will crush mobile service provider networks and profit margins.