Fewer think entertainment and content are illogical areas that could drive service provider revenue growth.

There is one theme that underlies thinking about all those potential growth avenues. The logic is to make an information asset a “communications” asset.

The reason that is important: in an era where applications are logically separated from network access, the value of access and transport becomes something of a commodity, difficult to differentiate.

Information--especially that related to discrete individuals and firms-- as well as content, are highly differentiated and therefore much more “unique.” And uniqueness creates the foundation for value, and higher retail prices.

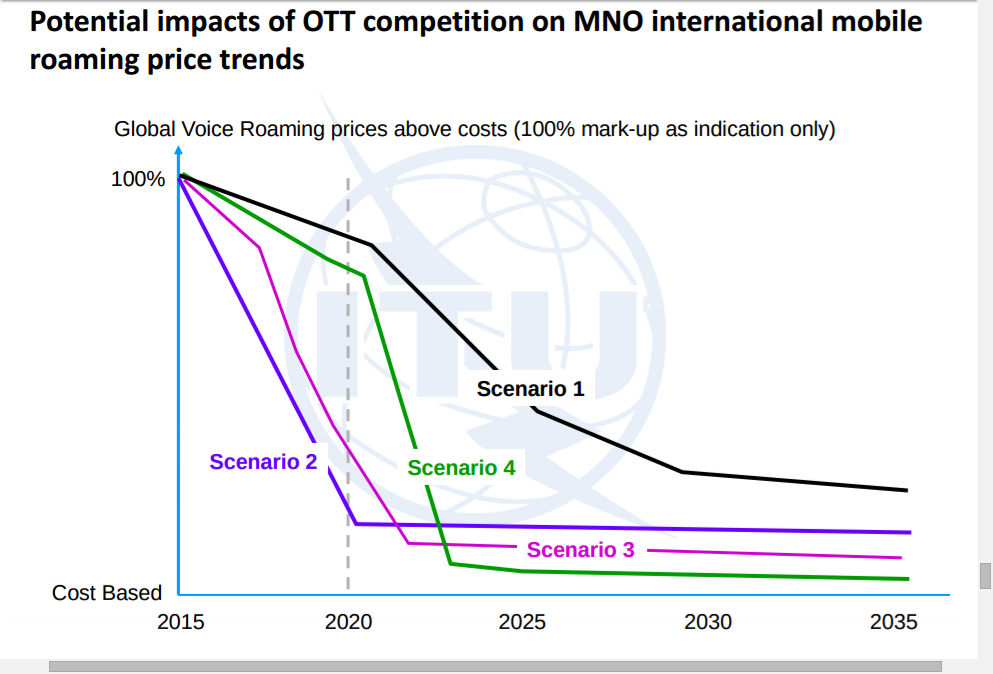

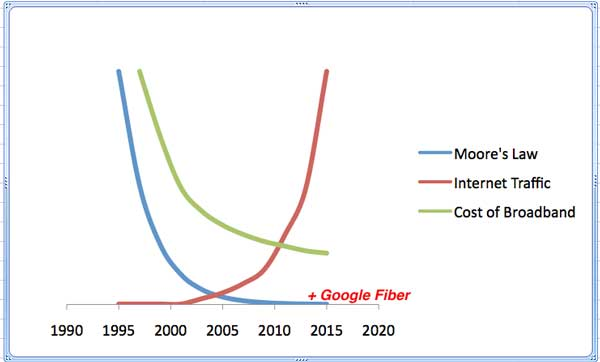

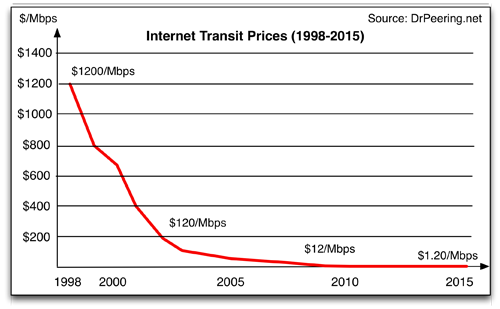

Between 1998 and 2015, for example, Internet transit prices fell about three orders of magnitude (by a factor of 1,000).

To be sure, transit prices are but one element contributing to final retail prices. But transit prices, and capacity prices more generally, suggest the direction of pricing trends.

Access networks, observers will note, are not “virtual” or as easy to replace or upgrade as chipsets or consumer devices. That suggests access costs should be sticky to the high side.

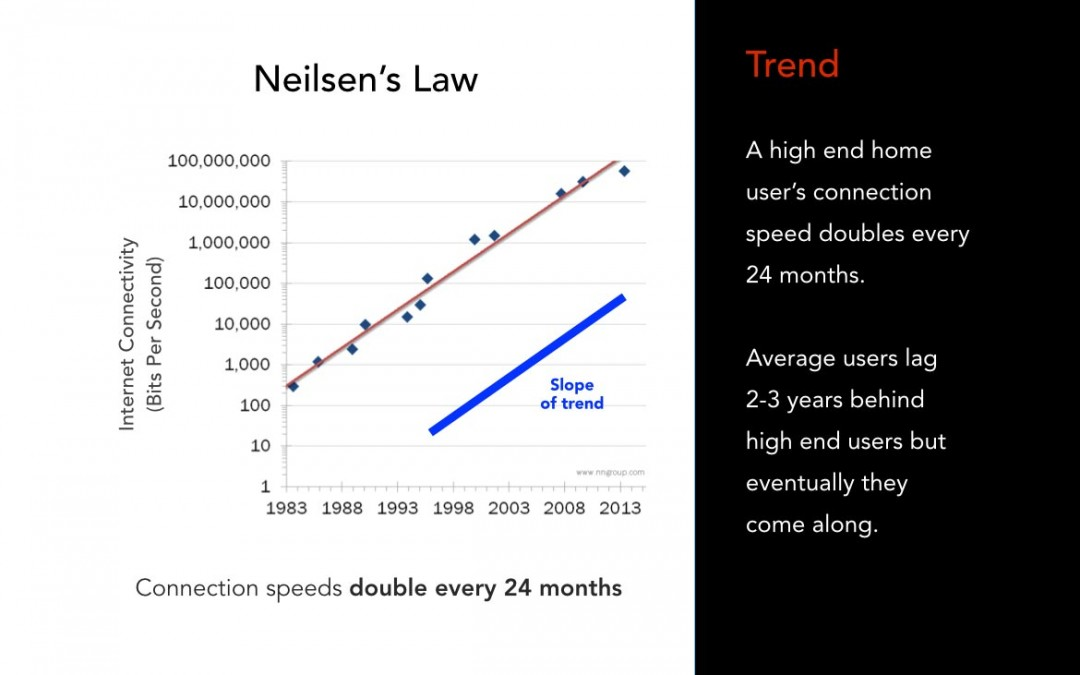

But even if “access” involves construction that cannot follow Moore’s Law, the actual trends for Internet access speeds and prices in the United States have nearly followed a path one would expect from Moore’s Law or Kryder’s Law.

In fact, if the trend continues, by about 2030, fixed networks and mobile networks will operate at the same speeds, an astonishing development, both technologically and in terms of business implications.

Since capacity increases that fast, but consumer discretionary spending power never does, the price per bit falls dramatically, even if retail prices drop marginally in developed markets, but rapidly in developing markets.

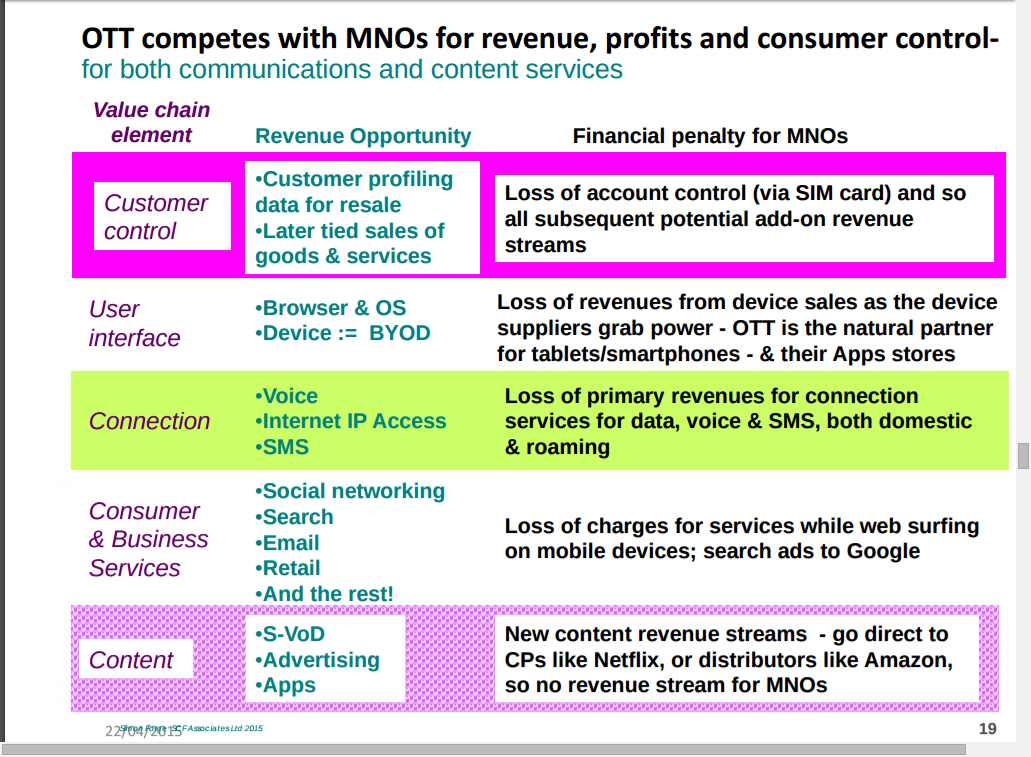

The implications are easy enough to predict: access--by itself--will become, and remain, a relative commodity, in the absence of value added other ways.

The implication, some of us would continue to argue, is that revenue growth, higher value and profit margins will require escaping the commodity-like “access and transit” function.

The threat posed by a “dumb pipe” role in the Internet ecosystem is precisely the commoditization of the function, and therefore the retail price, sales volumes and profit margins.

Content and information functions, on the other hand, remain capable of differentiation. Future winners in the service provider space likely will succeed in operationalizing that insight.