SpaceX successfully landed a Falcon 9 rocket booster at sea, the second such successful landing, and a major step on the way to commercializing reusable booster rocket technology.

That, in turn, will help lower launch costs, an important development for lowering the cost of satellite communications and earth-orbiting manned space stations.

Lower costs are important for suppliers of satellite high-bandwidth Internet access services, since coming market demand will require cost-per-bit performance orders of magnitude beyond what has been required in the past.

Friday, May 6, 2016

SpaceX Successfully Lands Rocket Booster at Sea

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

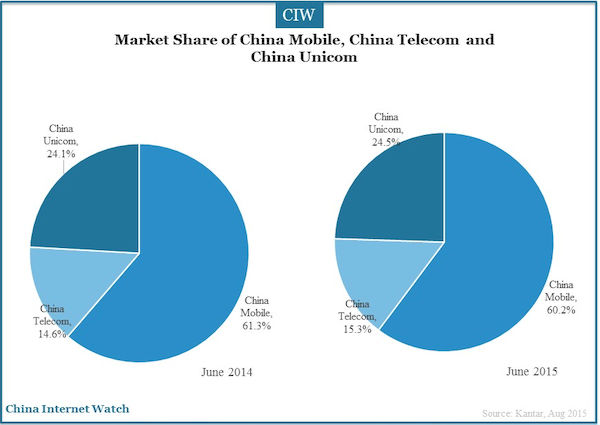

China Authorizes 4th Mobile Operator

China has authorized a fourth mobile operator, allowing state-owned China Broadcasting Network--which was created in 2014 to consolidate cable TV and broadcast operations in China--to enter the mobile services market.

Two angles are noteworthy. First, CBN marks the entry of the cable TV industry in China into the mobility business. Second, the move illustrates a continuing divide among communications regulatory authorities about the “best” market structure for mobile communications.

Given a choice, most seem to believe “four” providers a better structure (at least in terms of competition) than “three.” French regulators are foremost among proponents of a “three supplier” structure, largely to bolster the climate for more-robust investment.

The tension illustrates the problem regulators face. On one hand, they would likely prefer both vigorous competition and robust investment. On the other hand, excessive amounts of competition will choke off appetite to invest.

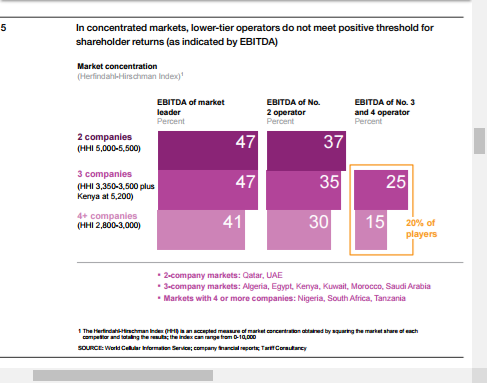

On a long term basis, some argue any structure with two suppliers, though not generally considered to be as good in terms of innovation, is the most stable market structure, the reason being that it is difficult for three providers each to maintain a minimum market share of about 30 percent.

That is a level many believe correlates with a minimum cash flow capability required to sustain long-term viability. By that test, China’s mobile operator market already is unstable, as only China Mobile has at least 30 percent market share.

Globally, profitability of operations for individual players correlates strongly with in-market scale measured by achieved revenue market share, McKinsey consultants have noted.

Sustaining an EBITDA margin of 30 percent can be considered a minimum proxy value for achieving capital returns above the weighted cost of capital, McKinsey says.

Entrants unable to capture a significant revenue share of their market--more than 25 percent-- will be unlikely to achieve EBITDA margins above 30 percent.

That implies a sustainable long-term structure featuring just two providers.

There is an important caveat, however. If, somehow, the average cost of creating a mobile business should change in an important way, reducing especially infrastructure capital investment and operating costs, then it is possible sustainable market structures could change.

It might be possible, long term, for more than two major suppliers to be profitable. But that might hinge on major changes in capital requirements and operating cost. That is why all developments in network virtualization, access to shared and unlicensed spectrum, and networks based on use of unlicensed and shared spectrum, are important.

Such developments can change the industry cost profile.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Thursday, May 5, 2016

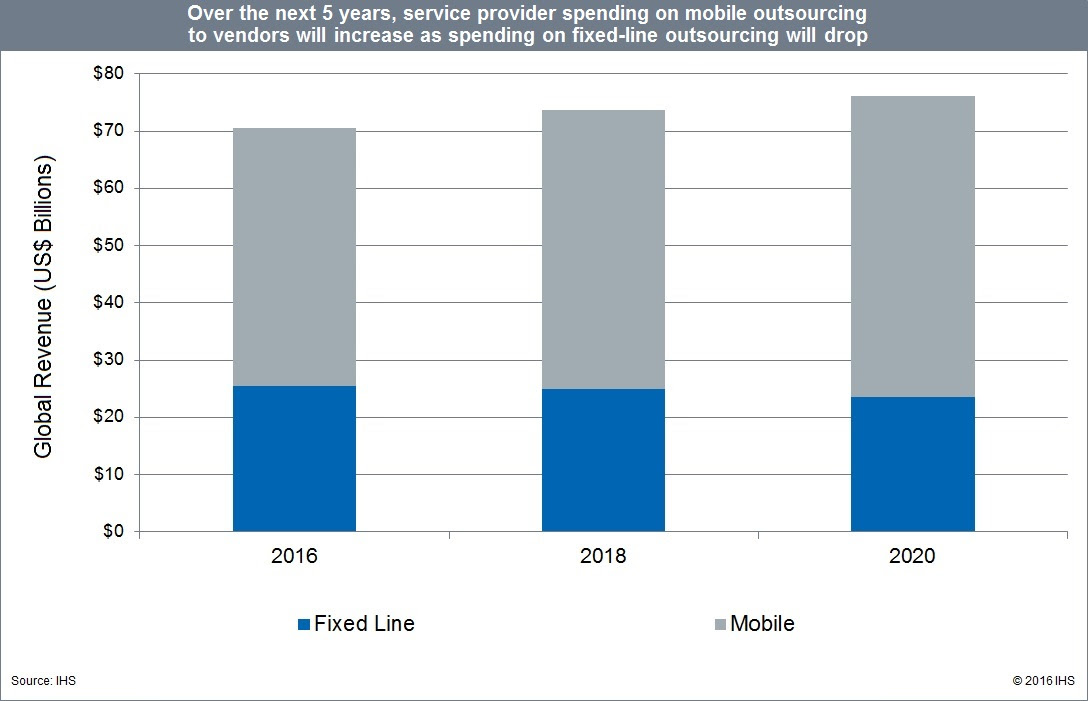

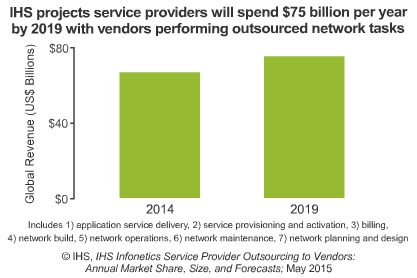

Telecom Outsourcing Will Grow 3% Annually Through 2020

It never is easy for any executive to clearly identify a company’s “core competence.” Asked to do so, most people cite a list of “things we think we do well.”

That is not core competence. To the extent a firm has such competence, and it is possible many firms do not, it is the singular capability that competitors cannot replicate. It is not “things we think we do well,” if other competitors also can make a credible claim in those areas.

As it turns out, many mobile operators find that operating access networks really is not a core competence, or at least adds little value.

Still, outsourcing is rather a subtle thing. About 52 percent of carrier outsourcing revenue in 2015 was in the areas of network maintenance, build, planning and design, not core operations.

Managed service revenues for outsourced operations, network maintenance and network planning and design s expected to grow at a three percent CAGR from 2015 to 2020, driven by a mix of full operation outsourcing and radio access network (RAN) sharing, according to Infonetics estimates.

In 2015, global outsourcing services revenue increased three percent over 2014 to reach $69 billion.

In 2014 worldwide telecom outsourcing and managed services revenue decreased 0.4 percent from 2013, falling to $66.6 billion, according to IHS Infonetics Research.

Network maintenance, build, planning and design accounted for over half of service provider outsourcing revenue in 2014.

Managed service revenue—the sum of operations, network maintenance and network planning and design—totaled $36 billion in 2014.

Telecom outsourcing services will reach $76 billion by 2020, growing at a compound annual growth rate of two percent and driven by mobile network outsourcing deals as more and more mobile operators try to keep their opex under control by removing non-core tasks.

Europe, Middle East, Africa remained the world’s largest outsourcing and managed services market in 2015 and is expected to do so through at least 2020.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Survey Shows Heavy Industry Leading IoT Deployments

In 2016, 43 percent of organizations will either already be using the Internet of Things or be implementing it within their environments, according to Gartner's survey of 465 IT and business professionals.

Some 29 percent of respondents already have deployed IoT technologies. Some 14 percent expect to do so in 2016.

"Heavy" industries, including utilities, energy suppliers and manufacturers are lead users at present, with 56 percent of businesses in those categories indicating that they will have implemented IoT by year's end.

"Up until now, the leading adopters of IoT have been more the industrial, heavy-industry-type businesses" involved in mining, manufacturing and the like, Gartner research Chet Geschickter, said.

Manufacturing and utilities are currently the top industry verticals currently driving the Internet of Things (IoT), says Jim Tully, Gartner VP.

In 2015, manufacturers had an estimated 307 million installed devices while utility companies had deployed 299 million. Those two verticals are responsible for over 600 million of the IoT devices currently in use.

"This makes intuitive sense; control systems using sensors have always been an integral part of manufacturing and automation processes, and we certainly see a lot of smart meter deployments by utilities leading to energy efficiency improvements and operations like automatic billing, energy management and monitoring," said Tully.

Geschickter noted that demand from consumer- and service-oriented companies in "light" industries is picking up. By the end of the current year, 36 percent of these businesses will have implemented IoT technologies.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

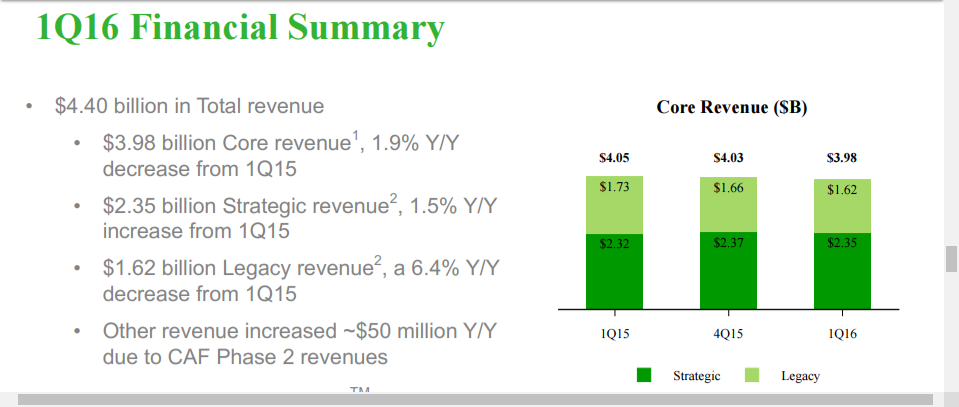

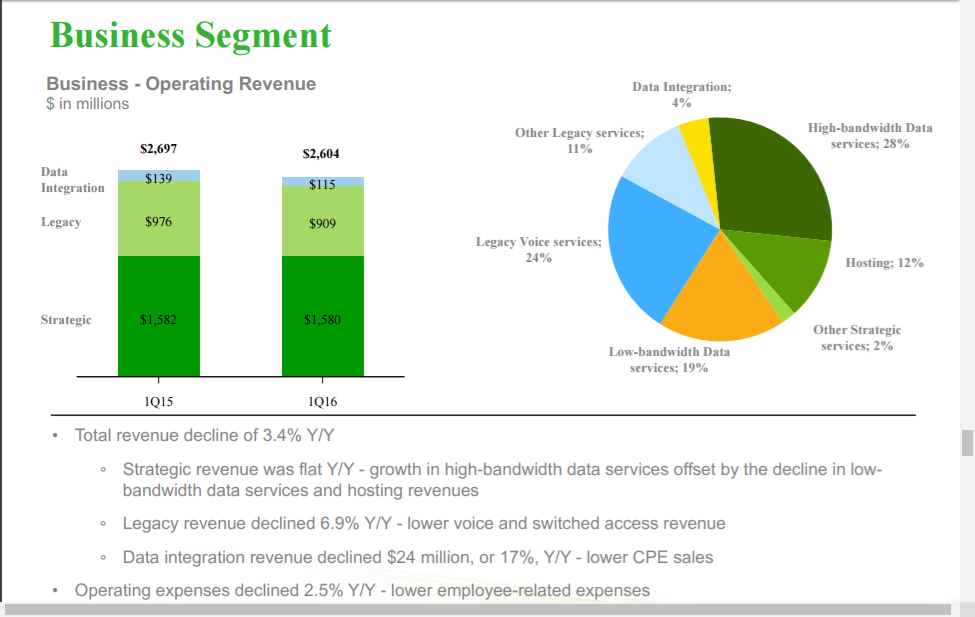

CenturyLink "Between a Rock and a Hard Place"

CenturyLink, the third-biggest “telco” fixed network services provider is "caught between a rock and a hard place,” according to Jennifer Fritzsche, Wells Fargo senior analyst for telecommunications services.

Basically, CenturyLink is not competitive with cable TV offers, so it either must step up investment or admit defeat and hope to make up revenue losses elsewhere.

Operating revenues for first quarter 2016 declined to $4.40 billion, compared to $4.45 billion in first quarter of 2015.

In its business customer segment, revenues of $1.58 billion declined 3.4 percent year over year. Total consumer segment revenues of $1.49 billion declined 0.5 percent, year over year.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

FCC Says Set-Top Monopoly is a Big Issue; Consumers Might Not Care

As the U.S. Federal Communications Commission moves towards requiring third party supply of decoders used to receive linear TV programming, a survey by Leichtman Research suggests consumers do not care too much about renting decoders.

“Pay-TV subscribers tend to express little enmity toward set-top boxes,” Leichtman Research suggests.

Some 20 percent of respondents to a Leichtman Research poll agree that “set-top boxes from TV companies are a waste of money.” On the other hand, 44 percent of respondents disagree with the statement.

About 42 percent of respondents agree that set-top boxes from TV companies provide features that add value to the TV service. Some 16 percent disagree that the boxes add value.

The study also found that 77 percent of TV sets in pay-TV households have a service provider set-top box, with a mean of 2.2 boxes per pay-TV household.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Virgin Media to Add 1 Million FTTH Connections; BT to Add 2 Million

Virgin Media, owned by Liberty Global has said it will use fiber to home to connect about a million U.K. homes by 2019. That is historically unusual, as cable operators have insisted loudly that the hybrid fiber coax network is extensible enough to underpin the business.

The Virgin Media decision is a rather major step towards use of a physical media platform suggesting Virgin sees an end to HFC as a market-leading platform.

To be sure, there is a key difference between the protocols telcos normally run when deploying FTTH and what Virgin Media will do. Virgin Media will use a technique known as Radio Frequency over Glass (RFoG).

The advantage is quite simple. Doing so allows Virgin Media to retain use of the same modulation techniques used to support HFC customers. That means a single set of headend resources can support either access method.

RFOG also means the same mix of services can be provided to all customers, no matter which network they are served by. That is important for marketing consistency, as it means Virgin Media will not risk confusing customers about what services they can get, depending on which network they use.

The big change: Fiber to the home is described as the “best and most modern” access technology. That is an extremely rare statement for any cable TV executive to make.

Of course, it might also be possible to infer the migration path. At some point, the primary advantage of RFOG (backwards compatibility) becomes a disadvantage (the full bandwidth of a passive optical network cannot be tapped).

But cable operators are big on “hybrid,” gradually evolving access networks. Still, at some point, HFC will run out of gas. In a strategic sense, that always has been true. But it never has been a tactical necessity.

It still is not, in this case. Comcast seems to be taking a different tack in its U.S. operation, planning to make use of FTTH to support symmetrical 2-Gbps access networks across perhaps 85 percent of its current footprint. Those networks will not use RFOG.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Comments (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...