For as long as I can remember, special access rates, conditions and terms of service have been contentious, for obvious reasons: there are sellers and there are buyers . The former want more freedom, the latter want less. The sellers are opposed to price controls, the buyers want them.

What might be sort of interesting in the latest round of discussions about regulating of special access is that Verizon, to a certain extent, is more concerned about being a buyer than a seller, as is Sprint, and virtually all competitive local exchange carriers.

There are some obvious nuances. Some might question the wisdom of prolonging a legacy service, in decline, when IP substitutes could be made available, and when a shift to Ethernet-based access is under way, in any case.

To a large extent, technology shifts are at issue here. Special access traditionally has been a set of products (T1, DS3) using specific protocols. Ethernet is the next generation protocol that is displacing the older forms of special access.

And among the issues is the degree of choice buyers have in the Ethernet access market, as distinct from the legacy T1, DS3 markets. Other issues, such as competitive dynamics, are in play as well.

Traditionally, cable operators, now the dominant suppliers of data access in the U.S. consumer Internet access market, can sell Ethernet connections, not just telcos. And then there are new competitors as well (Google Fiber, other independent ISPs).

In fact, many who sell access to smaller business accounts would note that sales of T1 lines for business phone systems are declining, in favor of other options such as SIP trunking, while Ethernet makes most sense for data connections.

“It's important to note that DS1 and DS3 lines are legacy products that are at the end of their technological life,” says consultant Roger Entner. Still, the direction is towards Ethernet.

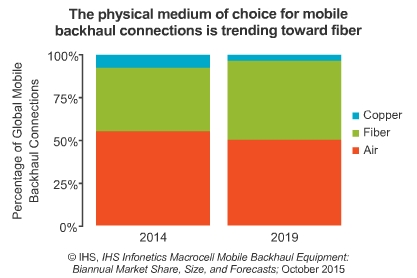

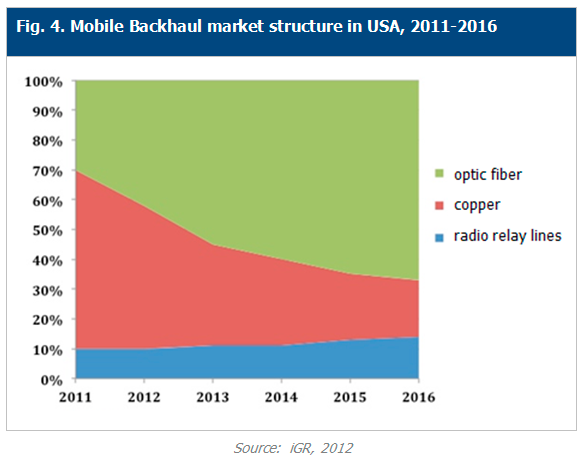

Network element and transmission sales, of course, are different than backhaul services purchased, but the trend is clear enough: fiber and wireless are growing, copper special access is shrinking.

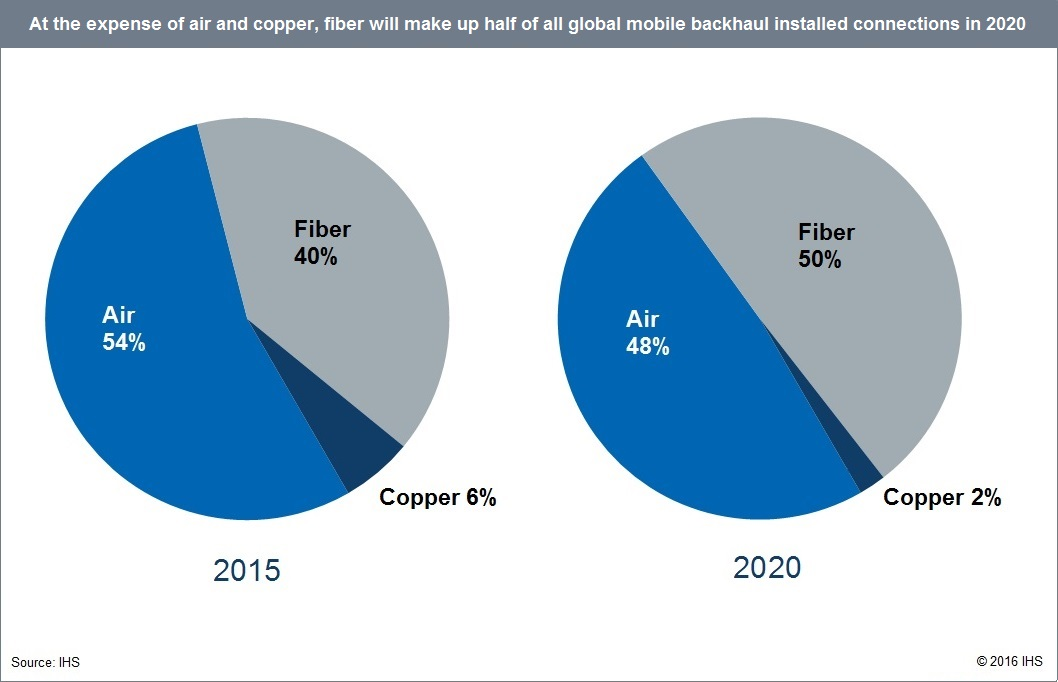

In 2012, Ethernet based mobile backhaul accounted for 40 percent of global physical connections of all types of mobile/cellular backhaul (e.g., TDM, IP). Ethernet was projected to be 95 percent of the mobile backhaul connections market by 2015. As with all such forecasts, nobody would be too surprised if the actual magnitudes differed from projected levels.

In 2015, wireless backhaul and optical connections vastly outnumbered copper connections typically used for special access, on a global basis. The U.S. market traditionally has favored fixed network connections, though.

Still, end user demand is shifting towards Ethernet, and new platforms (cable access, fixed wireless), even as new options are coming (millimeter wave fixed wireless), Google Fiber, independent ISPs, municipal broadband).

To be sure, there still is demand for legacy T1 or DS3 connections, but Ethernet rapidly is eroding and replacing that demand. To the extent that a faster shift to all-IP networks is desirable, does it make sense to subsidize the legacy access methods?

Zayo, for example is one of the leading suppliers of backhaul circuits of these types in the U.S. market. “The number of DS3s sold by Zayo has declined from 3,569 in September 2013 to 2,772 in June 2015, a 23 percent drop in less than two years,” Entner notes. “For DS1s, that decline has been even more pronounced--from 3,569 to 2,772--a 38 percent decline from September 2013 to June 2015.”

That said, the Federal Communications Commission still argues that the product “special access” in all its forms represents between $25 billion and $40 billion in annual sales.

The new argument is that special access regulation is needed to support coming 5G and small cell networks. Others would argue Ethernet connections are going to be needed even there.

Some would argue that represents both retail sales to business customers as well as the smaller backhaul market (mobile tower backhaul, for example) that is much smaller, representing perhaps $8 billion worth--perhaps less--of annual revenue.