How much of what matters in life is simply this?

Sunday, December 1, 2019

Much of What Matters in Life is Pretty Simple

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

How Much Share Does 5G Fixed Wireless Have to Shift to be Meaningful?

How much market share does 5G fixed wireless have to shift before it affects the profitability of the fixed network consumer internet access market? Not much.

In recent quarters, for example, U.S. fixed network internet access net additions have totaled about six tenths of one percent of the installed base, with cable gaining eight tenths of one percent while telcos lost about two tenths of one percent.

In other words, a shift of about two-tenths of one percent per quarter halts the telco decline. A shift of perhaps six-tenths of one percent--from cable to telco--actually causes cable share to begin a decline.

That is what the stakes realistically are: a chance for telcos to halt, and perhaps reverse, the long-term decline of their market share in internet access.

Cable TV executives in the U.S. market naturally express as much skepticism about the dangers 5G fixed wireless services pose for their consumer broadband business as telco execs say they are optimistic. Basically, it will no scale, or will scale too slowly to keep up with cable’s own planned bandwidth plans, cable execs tend to say.

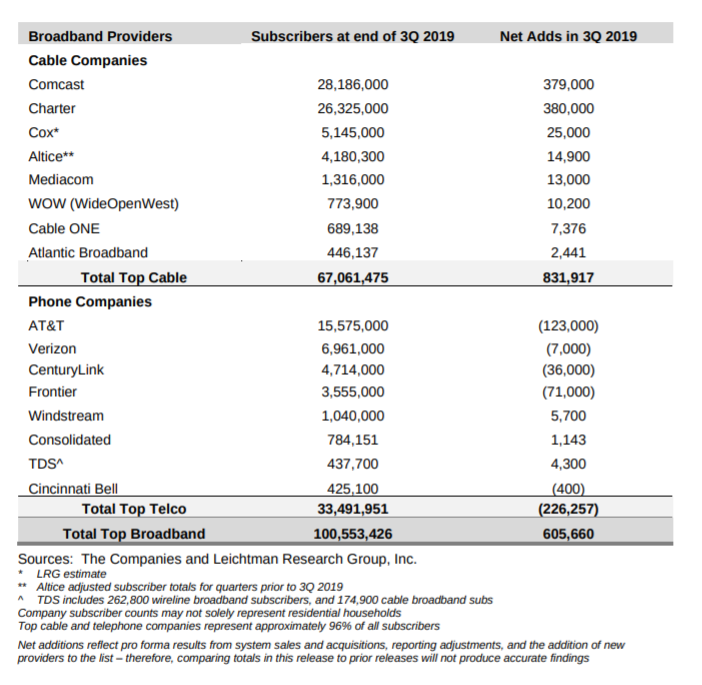

There is reason for the cable views. The threat of optical fiber to the home has existed for a few decades, but has not dented cable’s emergence as the leading supplier of consumer internet access connections using fixed networks. Cable has about 67 percent of the installed base and has essentially gotten more than 100 percent of the net new account additions for a couple decades.

In fact, over the last 20 years, it would be hard to find a single year where cable broadband net account gains were not about 60 percent to 70 percent of all net gains.

But the impact of 5G fixed wireless is not that it dramatically upsets the market. 5G fixed wireless might be the only way telcos collectively can halt a long-term decline of their market share.

It might be prudent not to envision any scenario where 5G fixed wireless actually upends the market share structure. Instead, 5G fixed wireless probably is relevant because it might shift just enough share to choke off the cable growth model, reverse the telco share loss trend, and then change profit margins.

It is very subtle stuff. Verizon, for example, only has to gain about 7,000 5G fixed wireless accounts per quarter to halt its customer losses. T-Mobile US and Sprint have virtually zero fixed network market share, so even smallish gains represent new accounts with average revenue possibly double what they get from mobile internet access accounts.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Thursday, November 28, 2019

Why 5G, Why Now?

There is a very simple reason why 5G networks must be built, and the numbers from the U.S. market illustrate the concept nicely. By design, 5G will increase capacity and speed a minimum of 10 times. That has been the case for every mobile platform since 2G.

Since observers expect a 10-fold increase in mobile data consumption over the next decade (perhaps even sooner), 5G simply represents a way to supply customer demand for mobile data. Everything else--new use cases to drive revenue--is a bonus.

The same argument explains why 5G is needed: cost per bit really has to fall at least 10 times over the next decade.

Since observers expect a 10-fold increase in mobile data consumption over the next decade (perhaps even sooner), 5G simply represents a way to supply customer demand for mobile data. Everything else--new use cases to drive revenue--is a bonus.

The same argument explains why 5G is needed: cost per bit really has to fall at least 10 times over the next decade.

The issue is how high mobile data consumption might go. Ericsson believes it is possible U.S. mobile customers could be consuming 39 GB each, per month, by about 2024. In a “typical” household of 2.5 people, that implies potential “household” mobile data consumption of nearly 98 GB per month.

source: Ericsson

Here is one way of looking at the required increases in mobile capability. By the end of 2018 average (“mean,” I believe) U.S. household data consumption on fixed networks was 268.7 gigabytes (I believe the figure is “per month”), according to Openvault, up about 19 percent from mid-year and up 33 percent from 2017 levels. So it seems likely that consumption will have grown at least 33 percent in 2019, and most likely higher.

So one "high end" scenario is that mobile networks theoretically might have to carry the same amount of data as delivered by a fixed network, where 5G fixed wireless competes for home broadband accounts directly with fixed networks.

The "typical" expectation might be that mobile networks must satisfy mobile data demand for about 2.5 users per household (about the U.S. average household size).

So one "high end" scenario is that mobile networks theoretically might have to carry the same amount of data as delivered by a fixed network, where 5G fixed wireless competes for home broadband accounts directly with fixed networks.

The "typical" expectation might be that mobile networks must satisfy mobile data demand for about 2.5 users per household (about the U.S. average household size).

Assume an average of 2.5 persons per household, each using the average amount of data. That suggests a mobile data consumption per household around 27 GB per month. But spreading use of “unlimited usage” plans likely will push consumption higher.

Customers on unlimited plans consume 67 percent more mobile data than consumers on usage-based plans in 2017, according to NPD.

Average monthly mobile data usage is around nine gigabytes per month. In a “typical” U.S. household of perhaps 2.5 people, that works out to about 27 GB per month of mobile data consumption, “per household,” on the mobile networks.

Others believe consumption is lower, at perhaps six gigabytes per user, per month, according to Strategy Analytics.

The implication is that mobile networks will have to be designed to carry between a quarter and a third of the data now expected in a typical U.S. household. That is a big jump from present levels. If the typical mobile user consumes 9 GB, and a household 268 GB, then mobile traffic is about three percent of fixed network levels.

That, in turn, implies an increase of mobile data capability by about an order of magnitude by 2024.

Hence 5G, which will increase capacity by a minimum of 10 times over 4G networks.

Hence 5G, which will increase capacity by a minimum of 10 times over 4G networks.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Wednesday, November 27, 2019

Telefónica to Shed Most Latin America Assets

Telefónica is unwinding a significant portion of tis “grow by acquisition” portfolio in an effort to reignite growth. Among the key moves, Telefónica will:

- Prioritize Spain, Brazil, the UK and Germany

- Spin off most of its Latin American assets

- Launch Telefónica Tech, supplying enterprise customers with cybersecurity, IoT, big data, and cloud services

- Create Telefónica Infra, intending to be a supplier to other service providers.

José María Álvarez-Pallete, Telefónica chairman and CEO, talks about the changes.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Sometimes Rankings do Not Matter Much

Sometimes international rankings on various measures of connectivity quality are less important than you might think. Consider voice adoption, where the best the United States ever ranked was about 15th globally, for teledensity (people provided with phone service).

Does anybody really think that was any kind of impediment to economic growth? That might also be the case for video entertainment quality of experience.

To the extent that video quality of experience is becoming a criteria for mobile service, operator policies, usage and bandwidth supply have a big impact. In fact, bandwidth alone does not dictate video quality of experience, Opensignal suggests, as some countries with good downstream bandwidth lag on video experience scores.

You might think that sheer download speed mostly or exclusively is key to experience rankings, but Opensignal tests suggest this is not the case.

South Korean users’ experience ranked first for download speed yet 21st for video, while Canadians’ were third fastest for download speed, but just 22nd for video.

Those results happen because mobile operators manage video traffic to preserve experience for other apps as well.

Experience also is a function of deliberate policy: carriers often automatically convert the picture quality of video from 1080p full HD, down to 720p, or even to just standard definition quality. Also, some service providers might offer standard quality or 720p image quality as a part of policies that offer unlimited or zero-rated video access.

Also, customers on unlimited usage plans might not have the same incentives to switch to Wi-Fi connections as do other customers with more-limited data usage plans.

The point is that a combination of circumstances--high video consumption, unlimited usage plans, limited spectrum and retail packaging--combine to reduce image quality scores.

What is not so clear is the importance of image quality for consumers, compared to usage allowances and rating policies. In other words, customers might accept or prefer lesser image quality in exchange for ratings policies that save them money, in the same way they often will tolerate advertising if it saves them money.

The value proposition is especially important if access to mobile video entertainment is a key part of the marketing. In the U.S. market, for example, T-Mobile U.S. includes Netflix on its Magenta plans; Sprint includes Hulu and/or Amazon Prime on a number of its plans; Verizon advertises 5G as suitable for 4K video quality on mobile and bundles Disney+ with its 5G wireless home broadband plans; and AT&T offers one of HBO, Starz, Cinemax, or Showtime as part of its Unlimited and More Premium plan.

Mobile video importance can be seen in advertising as well. The Internet Advertising Bureau says 62 percent of total video ad starts are happening on mobile devices, for example.

The Opensignal methodology takes picture quality, video loading time and stall rate into account to create a score on a scale of 0 to 100, reflecting users’ perceived mobile video quality.

While there was an improvement in U.S. customer video experience, it remains in the “fair” category. U.S. customers had the lowest video experience score of any of the G7 countries as “U.S. carriers struggle with the combination of enormous mobile video consumption and insufficient new spectrum.”

U.S. mobile service providers face two key challenges not seen in many other countries: U.S. consumers watch a lot of mobile video, while spectrum is limited.

Opensignal has found that 39 percent of U.S. consumers watch TV programs on their smartphones, and similarly, 38 percent watch movies. Also, 28 percent of consumers sometimes switch to mobile connections in order to watch video.

Some 38 percent of consumers watch video on their smartphone at home on a mobile connection (compared with 71 percent that watch at home on Wi-Fi).

International rankings can be useful. At other times they are interesting, but perhaps not indicative of pressing business problems.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Tuesday, November 26, 2019

Spectrum Policy is the Latest in a Long String of "U.S. is Falling Behind" Claims

Over the past few decades I have often heard observers expressing great worry about one or another divides or gaps that have U.S. service providers and consumers behind users and customers in other regions.

U.S. consumers were “behind” Europe and Japan in mobile phone use, text messaging, 3G use, internet access, broadband adoption and speeds, and always are “paying too much” for their services.

The U.S. is falling behind meme never goes away, where it comes to communications. The latest assertion is that the United States is falling behind in 5G. That claim has been made many times in the past, and always has proven wrong.

In the past, it has been argued that the United States was behind, or falling behind, for use of mobile phones, smartphones, text messaging, broadband coverage, fiber to home, broadband speed or broadband price.

It is an old pattern of claims. Consider voice adoption, where the best the United States ever ranked was about 15th globally, for teledensity (people provided with phone service). Does anybody think that was any kind of impediment to economic growth?

With the caveat that some rural and isolated locations never got fixed network phone service, not many would seriously argue that the supply or use of fixed network voice was an issue of any serious importance for the nation as a whole, though it is an issue for rural residents who cannot buy it.

Some even have argued the United States was falling behind in spectrum auctions. What such observations often miss is a highly dynamic environment, where apparently lagging metrics quickly are closed.

The latest candidate is 5G spectrum policy.

Over the past year there have been many shouts of alarm about the “choices” being made for 5G spectrum. Millimeter is the wrong spectrum, it has been said. Mid-band spectrum is the “right choice,” many have argued.

Those criticisms are rather off point. Different countries are making different immediate choices largely because--of a range of permissible frequencies--mid-band is available.

For historical reasons, the mid-band is not immediately available in the U.S. market, forcing early movers to rely on millimeter wave spectrum sooner than they might have preferred, even if the 5G standards clearly point to millimeter wave as the future of 5G, and subsequent platforms as well, simply because that is where most of the unencumbered spectrum exists.

The U.S. Federal Communications Commission is not ignorant. It knows what resources can be made available now, and what has to happen to clear more mid-band spectrum. It is doing so. Clearing part of the C-band is among the actions the FCC is taking. But that takes time.

Verizon, in particular, has had to rely on millimeter wave. Among the top four national carriers, it has the least spectrum, per customer. And after weighing its options for bandwidth, Verizon concluded that upgrading its terrestrial network with dense optical fiber, enabling small cells and hence millimeter wave radio networks, made more sense than bidding for lots of new spectrum.

That does not mean Verizon or the other service providers will be shy about bidding on additional spectrum. “More” is always the answer, longer term.

Still, Verizon believes the cost of its dense fiber network approach will work for capacity expansion. Verizon surely will rely on mid-band for coverage. AT&T initially relied on millimeter wave for its business-focused services, especially for fixed network substitution.

Its consumer 5G will use 850 MHz low-band spectrum, and AT&T will acquire more mid-band spectrum when it is made available.

T-Mobile, with relative plentiful new 600-MHz assets, will rely on low-band for its 5G launch. Sprint has lots of mid-band spectrum licenses, which will eventually be put to work by whatever company winds up owning it.

The larger point is that no dangerous or wrong spectrum choices have been made by the FCC or service providers. Specific firms have made choices congruent with their assets and strategies. Long term, there is no “choice” to be made between millimeter wave and mid-band spectrum or low-band. All will be used.

But different service providers in different countries have differential access to low-band or mid-band spectrum. So the initial strategies and deployments will reflect those immediate realities. Longer term, all the choices will be in play.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

5G is How the Industry Copes with 300% Consumption Increase in 6 Years

If mobile data consumption globally grows by 300 percent, as Ericsson now predicts, the value of 5G is that it allows mobile operators to support that consumption growth. Compared to all other operating networks (2G, 3G and 4G), 5G is the network that will handle most of the growth, while also allowing mobile operators to supply that demand while preserving a profit margin.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Subscribe to:

Posts (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...