Voice accounts for about 30 percent to 40 percent of FNB Connect total revenue, the firm says. FNB launched its own mobile service in 2015. That points out a salient fact for the telecom industry: voice once generated the bulk of revenues, but now is an essential function, but less a revenue generator.

In 2016, for South Africa as a whole, mobile operators made about 53 percent of total revenue from voice services. Mobile data services contributed 38 percent of total revenue, text messaging about seven percent of total revenue.

But voice revenue is declining fast, globally. Using 2008 as a baseline, by 2013, five years later, a number of tier-one service providers had lost between 20 percent and 55 percent of legacy voice revenues.

Looking back over a longer time frame, in the U.S. market, one can see that 2000 was the year of “peak voice” for long distance revenue earned by local telcos. The usage drop over about a decade from 2000 was more than 50 percent. The revenue drop tracked usage decline.

Mobile service providers in Asia might face similar pressures on revenue. My general rule on revenue earned by service providers is that telcos must expect to lose about half their legacy revenue every decade. The U.S. experience with revenue loss provides one example, but each nation and market should be able to find similar changes.

That of course creates the necessity of developing big new revenue sources to replace those lost revenues, and in turn reflects the product life cycle in general. Intel, for example, seems to exhibit that same general pattern.

Im 2012, for example, Intel earned nearly 70 percent of revenue from “PC and mobile” platforms. By 2018, PC/mobile had dropped to about half of total revenue. By 2023 or so, Intel should generate 60 percent or more of total revenue from sources other than PC/mobile.

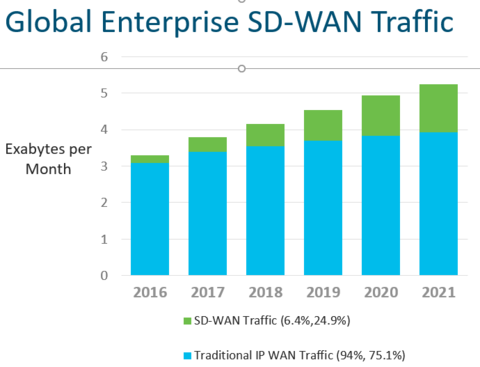

The point is that any service provider that intends to make a living “sticking to its knitting” and selling connectivity products has to account for the shrinking demand curve. To be sure, new connectivity products are being created. Software-defined wide area networks provide one example.

But that will not be nearly enough. The challenge is to replace half of total revenues from legacy sources. SD-WAN revenues available to service providers presently do not exceed a couple billion dollars a year. Total global revenue is about $1.5 trillion. That implies a need to discover or create as much as $750 billion worth of new revenue over the next decade, globally.