Cowen Group equity analyst Jim Friedland estimates that Google is generating $7 per year from each smart phone and tablet now used by mobile consumers globally.

Cowen Group equity analyst Jim Friedland estimates that Google is generating $7 per year from each smart phone and tablet now used by mobile consumers globally. That figure includes both search and display advertising in mobile apps on both Android and iOS (iPhones and iPads).

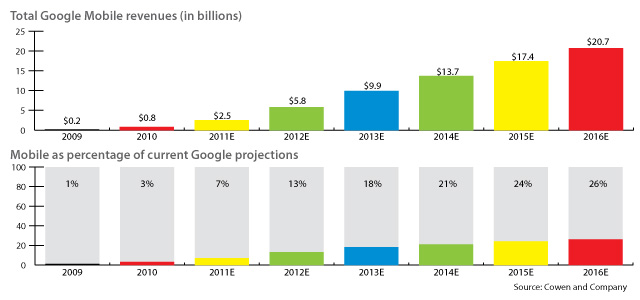

Active smart mobile devices worldwide reached 509 million in 2011, and are projected by Friedland to reach 914 million in 2012.

Based on that figure, Google’s mobile ad revenues could more than double from an estimated $2.5 billion in 2011 to $5.8 billion in 2012.

As a percentage of Google’s total revenues, Friedland estimates that mobile grew from three percent in 2010 to seven percent in 2011 and will almost double again to 13 percent in 2012.

By 2016, he expects mobile to be a $20 billion business for Google, and represent 26 percent of its total revenues. Google’s mobile ad revenue $5.8 Billion in 2012?

That suggests the magnitude of the challenge facing mobile service providers who generally consider mobile advertising one of a small handful of growth opportunities lucrative enough to contribute significant incremental revenue once mobile broadband the current growth driver, starts to saturate.

If any mobile operator were to do as well as Google now does, that would work out to about $1.17 a month of incremental revenue per smart phone user, per month, at a $14 annual run rate. Consider that current revenues for voice, texting and data can run $75 per user, per month.

Of course, the problem is that some current revenue contributors, especially voice and messaging, slowly are declining. And some observers think capital investments and operating costs actually could go negative, in many markets across Europe, North America and the Asia-Pacific region as early as 2015.

Mobile advertising, mobile payments or machine-to-machine services, as well as cloud computing and other initiatives simply will not contribute significant revenues over the next five to 10 years, during which mobile service providers will have to rely on mobile broadband to fuel revenue growth.

Though not every mobile service provider will face such issues, many mobile executives will be facing huge profitability challenges between now and 2016, according to Juniper Research, which forecasts that mobile service providers face potential capital investment and operating costs that actually exceed revenues by about 2014, Juniper Research says.

Separately, analysts at Analysys Mason concluded that carriers in many regions around the world face the risk of an "end to profit" in 2015 if not before.

A study carried out by mobileSquared surveyed 31 global mobile operators and found that one third of operators already see traffic and revenue decline, while 75 percent of are worried about losing revenues to mobile application providers.

The research confirmed that over-the-top apps already are affecting traffic and revenues. Some 32 percent of respondents thought operator traffic from messaging, voice and video calling would decline between 11 percent and 20 percent over the next five to 10 years. About 20 percent of respondents estimated revenue would fall 31 percent to 40 percent over the next five to 10-year period.

The problem, according to Juniper Research, is that profit margins are running between 15 percent and 20 percent, which means many service providers are at about break even.

By 2015, costs will exceed revenues slightly, and fall below capital and operating expense by about 2016.

Separately, analysts at Tellabs also predict that revenue could fall below costs "within four years."

The Analysys study assumes a continuation of current cost and revenue trends, especially the current pricing of bandwidth. The findings also suggest the immediate need mobile service providers have for changes in retail packaging and pricing to keep revenues above cost.

In the near term, increasing data revenue per subscriber is about the only way mobile service providers will avoid a dangerous turn towards sustained financial losses.

![[GOOGAD]](http://si.wsj.net/public/resources/images/MK-BR741A_GOOGA_NS_20120119181203.jpg)