Much discussion about network neutrality seems to assume that the issue is bit or application "blocking," and from one perspective that is correct. The existing Federal Communications Commission rules about a users' right to use all lawful applications already prohibit blocking of legal applications on wired networks. The issue is whether those rules, and the other "Internet Freedoms" principles also should be extended to the wireless domain.

In another sense, popular perceptions are misguided or worse. There is a separate issue, that of whether it ever is permissible, for any legal reason, to shape traffic, either to maintain network performance, provide an enhanced service to a user, or create a new level of service.

Some will maintain there are other ways of maintaining end user experience aside from traffic shaping. That is arguably correct, but might cost so much that the entire consumer access pricing regime has to change in ways people will find objectionable.

Some argue that any traffic shaping of legal bits should be banned, because such practices have undesirable business impact. "No bits should have any priority," that line of reasoning suggests.

One might simply note that about 60 percent of video bits--almost universally served up by media companies--already enjoys such "unequal treatment." Indeed, that is the purpose of a content delivery network: to expedite the delivery of some bits, compared to others, so that a better end user experience is possible.

In fact, about $1.4 billion was spent in 2008 precisely to deliver such expedited bits. The U.S. market currently generates an estimated 55.8 percent of the global CDN traffic, though international traffic is now increasing at a faster rate than its domestic counterpart, according to Research and Markets.

And though video delivery historically has been the CDN staple, new growth areas include whole site delivery, dynamic content, "live" video, high-definition video, mobile and smartphone applications, other non-PC devices and adaptive bit rate streaming, Research and Markets notes.

Of the 22.5 billion professional video views served during 2009, Akamai delivered 31.9 percent, Limelight Networks 12 percent and Level 3 11.2 percent, says Research and Markets.. Additional CDNs active in the market include CD Networks, Velocix, Liquid Compass, Abacast, Mirror Image, Edgecast Networks, Highwinds, BitGravity, Cotendo and Internap, the firm notes.

The point is that preferential delivery of bits already is an established part of the way the Internet works. Private network users, especially businesses, also commonly set up traffic priority systems for their internal communications and content, as well.

The ability of a consumer end user to choose to use such services and applications is one of the implications of the network neutrality debate that often is lost. To reiterate, preferential treatment of bits already is happening on a wide scale, and for very good reasons: to preserve end user experience. Perhaps we ought not to be in such a rush to foreclose practices and capabilities of obvious value.

Sunday, November 29, 2009

Content Delivery Networks and Network Neutrality: Net Is Not Neutral

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Friday, November 27, 2009

Gartner Drops "Unified Communications" from 2010 "Top 10" List

Unified communications, which was on Gartner's "top 10" trends list for 2009, has been dropped from the 2010 list, which moves "cloud computing" to the top spot.

People will disagree about what that means, but no trend remains "top of mind" forever. Nor is the ranking an indication that UC is unimportant, simply that it might not be among the most-important priorities for the coming year.

It might simply indicate that most enterprises have figured out what they want to do, for the moment.

It might indicate that computing architecture, and issues related to computing architecture, which always are top concerns for enterprise IT staffs, once again have moved to the forefront, and that "voice" issues related to IP telephony are largely in an advanced stage of deployment.

In fact, four of the top-six issues are directly related to remote computing capabilities.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Tuesday, November 24, 2009

Users Say They Want ISPs Offering Both Wireless and Fixed Broadband

Specifically, more than 60 percent of survey respondents indicate a strong interest in mobile Internet, and 45 percent state that for their next broadband purchase they will choose an ISP that offers mobile service.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Do Usage Caps for Wireless and Mobile Broadband Make Sense?

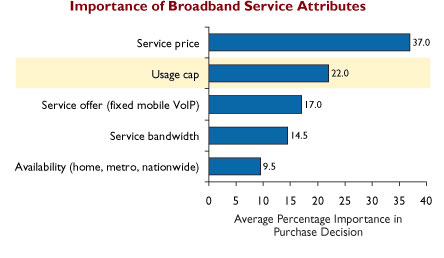

Consumers say 60 percent of the wireless broadband decision is based on two factors: monthly recurring charge and existence or size of a usage cap. For that reason, "data caps" are a particularly unfriendly way to manage overall traffic, says Yankee Group analyst Philip Marshall.

A better approach, from a service provider perspective, is to offer unlimited usage and then manage traffic usingreal-time, network intelligence-based solutions like deep packet inspection and policy enforcement, Marshall argues.

Some would argue that fair use policies that throttle maximum speeds when policies are violated is no picnic, either. But temporary limits on consumption, only at peak hours of usage, arguably is more consumer friendly than absolute caps with overage charges.

To test consumer preferences, Yankee Group conducted a custom survey that included a "choice-based conjoint analysis," which allowed Yankee Group analysts to estimate the relative importance to consumers of key wireless broadband service attributes. The survey was taken by 1,000 mobile consumers who also use broadband access services.

From the conjoint analysis, "we found that, on average, 59 percent of a wireless broadband purchase decision depends on two factors: service price, and the presence or absence of a 2 GByte per month usage cap," Marshall says.

The results also indicate that 14.5 percent of a typical purchase decision is affected by service bandwidth, and that the implied average revenue per user lift when increasing bandwidth from 768 Kbps to 2 Mbps ranges between $5 and $10 per month.

The results also indicate, however, that there are diminishing returns for service plans that offer speeds above 3 Mbps, though speed increases might be useful for other reasons, such as competitive positioning.

"Our price elasticity analysis implies that consumers are willing to pay $25 to $30 more per month for plans that offer unlimited usage, compared to plans that have a 2 GBytes a month usage cap," says Marshall.

"In a competitive operating environment, consumers will tend to migrate toward higher bandwidth services, all else being equal, but they are not necessarily willing to pay a significant premium for the added performance capability," says Marshall.

Our most recent survey results indicate that consumers require 2 Mbps to 3 Mbps bandwidth for their broadband service. This is likely to increase dramatically over the next two to three years, but the consumer survey suggests dramatically-higher bandwidth does not affect decisions as much as recurring price and existence of bandwidth caps.

For example, when offered a choice between one package featuring a 2 GByte per month usage cap with 6 Mbps bandwidth, and another package with unlimited monthly usage but just 2 Mbps service speed, 63 percent of consumers opted for the 2 Mbps service with no cap.

Even when the choice is between an unlimited package offering only 768 Kbps bandwidth, compared to an alternative plan with 6 Mbps bandwidth and a 2 GByte per month usage cap, 57 percent preferred the 768 kbps package.

Service providers still must manage bandwidth demand though, with or without usage caps

Usage caps work to regulate demand, but users do not like them.

The other approach is not to impose the usage caps, but instead to use policy managment and deep packet inspection to manage traffic flows.

If such solutions are implemented in a non-discriminatory manner, so that all like services are treated equally, they can be implemented irrespective of network neutrality regimes currently under consideration, Marshall believes.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Small Business Commits to Social Media, Email, Search

The findings might not suggest small businesses are spending wildly. In most cases the firms likely are testing new media. But the testing seems very widespread.

Almost all businesses with 500 or fewer employees will use email marketing next year, the company says. Only 3.8 percent of small business executives say they will not be using email marketing in 2010.

More than 70 percent also indicated they would not use TV or radio advertising.

Search advertising is used by about 72 percent of small businesses, but banner advertising is used by about 40 percent of small businesses, VerticalResponse says.

Facebook, Twitter and YouTube, as well as other social media sites, are used by about 78 percent of small businesses, the firm says.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Monday, November 23, 2009

Best Buy Sells Phone Power Nationwide

Best Buy now is distributing the "Phone Power" VoIP service nationwide. That's a pretty big boost for any retailer, and especially so for an independent VoIP provider aware that the market is consolidating and that scale is sorely needed.

Phone Power costs $19.95 per month with no contract, $16.95 with a one-year contract and $14.95 for a two-year contract. The service offers unlimited calling within the United States and Canada and 60 international minutes in 88 countries.

The Best Buy offering includes a two-line home adapter as well as a USB travel adapter. It sells for $79.95, and comes with a $79.95 instant service credit to be applied when the customer activates service on an eligible one or two year service plan.

It isn't clear yet whether Best Buy also will be actively selling Phone Power business packages, which come in both multi-line and single-line versions, offering unlimited inbound calling and 5,000 minutes of outbound calling with auto-attendant feature, and other popular business features, included on multi-line packages.

Phone Power costs $19.95 per month with no contract, $16.95 with a one-year contract and $14.95 for a two-year contract. The service offers unlimited calling within the United States and Canada and 60 international minutes in 88 countries.

The Best Buy offering includes a two-line home adapter as well as a USB travel adapter. It sells for $79.95, and comes with a $79.95 instant service credit to be applied when the customer activates service on an eligible one or two year service plan.

It isn't clear yet whether Best Buy also will be actively selling Phone Power business packages, which come in both multi-line and single-line versions, offering unlimited inbound calling and 5,000 minutes of outbound calling with auto-attendant feature, and other popular business features, included on multi-line packages.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Apple And Android Dominate U.S. Smartphone Web Traffic

AdMob’s October, 2009 measurements show that the iPhone/iPod Touch and Android phones account for 75 percent of mobile Web traffic in the United States.

Apple devices continue to dominate, with 55 percent share, but Android users in October represented 20 percent of all activity, up from 17 percent in September, 2009.

The iPhone and iPod Touch grew their share from 48 percent to 55 percent share over the same period.

The Blackberry ’s mobile Web traffic share went down from 14 percent to 12 percent, and Palm’s webOS shrank from 10 percent to five percent.

On a global basis, the iPhone operating system now accounts for 50 percent of all mobile traffic, up from 43 percent the month before.

Android has an 11 percent global share, which makes it third globally after Nokia/Symbian’s 25 percent share.

Since Verizon launched the Droid about two weeks ago, Droids now make up 24 percent of all Android mobile Web traffic. The HTC Dream, which is the oldest Android device on the market, is the only Android device with more share, at 36 percent of Android traffic. Give it a few more weeks. The Droid is shaping up to be the most-popular Android device so far.

The data suggests that the BlackBerry, though a worthy enterprise device, continues to lag as a smartphone choice for users whose key applications lean to the Web.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Comments (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...