Thosse of you who are developers, or at least "technical," will enjoy this detailed analysis of why mobile apps are destined to underperform mobile web apps for quite some time.

Thosse of you who are developers, or at least "technical," will enjoy this detailed analysis of why mobile apps are destined to underperform mobile web apps for quite some time. Saturday, July 13, 2013

Why Web Apps are Slow

Thosse of you who are developers, or at least "technical," will enjoy this detailed analysis of why mobile apps are destined to underperform mobile web apps for quite some time.  Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Why Does AT&T Want to Buy Leap Wireless Now?

Why does AT&T want to buy Leap Wireless now? That’s a different question than asking why AT&T might want to buy additional assets.

AT&T has been among the list of potential Leap Wireless acquirers for some time, along with T-Mobile USA and Sprint.

There are lots of reasons for the expectations of further acquisitions by the U.S. market leaders. Organic growth has become quite difficult in a saturated market, making acquisitions within the core market, and acquisitions in new markets, the fastest way to obtain additional subscribers and revenue growth.

And though top-tier mobile service providers are not unduly enamored of prepaid accounts, as opposed to postpaid, prepaid remains one of the few places in the domestic market where growth is expected.

And since the major carriers have tended to favor separate brands when participating in the prepaid business, the Cricket business works for AT&T.

One motivation that was behind the ill-fated bid for T-Mobile USA--spectrum assets--also is an attraction here. Getting additional customers is helpful, but spectrum assets also are helpful, especially when complementary to AT&T’s current holdings.

Still, there is the issue of timing. Assuming regulatory issues are not an issue, and market conditions are neutral to favorable, why make the bid now?

Maybe because other potential rivals are preoccupied. T-Mobile USA continues to digest MetroPCS, while Sprint has combined with SoftBank and Clearwire. Verizon Wireless has little interest in becoming a bigger force in prepaid.

But there is Dish Network.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Friday, July 12, 2013

AT&T to Buy Leap Wireless

AT&T is buying Leap Wireless, including its five million subscribers, the Cricket brand and spectrum, network and retail assets, though the deal is subject to regulatory approval.

Leap's network covers 96 million people in 35 U.S. states, most of whom use Leap’s CDMA 3G network. But Leap also has a 4G Long Term Evolution network covering 21 million people.

AT&T says it will retain the Cricket brand name, provide Cricket customers with access to AT&T's 4G LTE mobile network, use Cricket's distribution channels and expand Cricket's presence to additional U.S. cities.

The move arguably offers the primary advantage of a new platform to gain share in the prepaid market.

But the proposed acquisition also includes spectrum in the PCS and AWS bands covering 137 million people and is largely complementary to AT&T's existing spectrum licenses.

AT&T says that Immediately after approval of the transaction, AT&T plans to add Leap's unutilized spectrum, covering 41 million people, to AT&T’s LTE network.

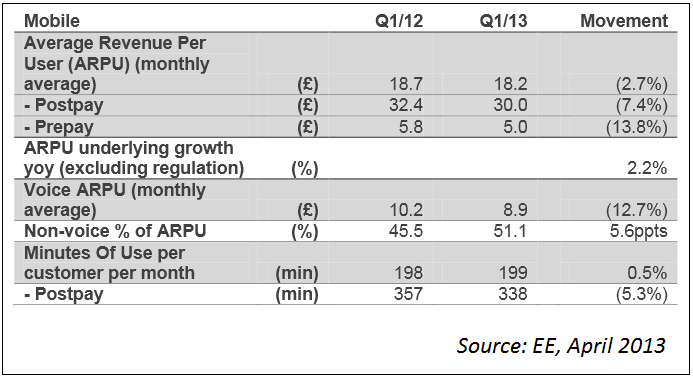

Regulatory approval might take as long as nine months, if past precedent applies. The deal would not change U.S. market share in a material way, one might argue. Leap Wireless has market share of less than two percent, and lower average revenue per user than typically is the case for a postpaid service provider.

EE in the United Kingdom typically sees postepaid average revenue per user that is as much as six times the value of a prepaid account.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

One Immediate Benefit of New Competition in Myanmar: SIM Cards 2 Orders of Magnitude Cheaper

Competition is supposed to bring new consumer benefits. And that appears to be what new mobile service providers have planned for their new networks in Myanmar.

Norway's Telenor and Qatar's Ooredoo say they will charge around 1,500 kyat ($1.53) for a SIM card. Consider that, at present, SIM cards can cost more than $200 each. So SIM cards will be available at two orders of magnitude less than at present.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Thursday, July 11, 2013

What Does Google See in Chromebooks?

Google’s Chromebook initiative initially was derided by many as “too little, too late,” coming at a time when the market was turning to tablets as the growth category in computing devices.

Google obviously did not agree then, and sales results now suggest Google was on to something. Though Chromebooks still represent a small portion of the total U.S. market for laptops and netbooks, Chromebook market share, and apparently growth rate, is increasing.

The devices had about four percent to five percent market share in the first quarter, though that was up from one percent to two percent in 2012, according to Mikako Kitagawa, Gartner analyst.

On the other hand, there is little question that tablets are leading consumer interest in computing devices at the moment. Global PC shipments dropped to 76 million units in the second quarter of 2013, a 10.9 percent decrease from the second quarter of 2012, according to preliminary results by Gartner.

This marks the fifth consecutive quarter of declining shipments, which is the longest duration of decline in the PC market’s history, Gartner says.

“We are seeing the PC market reduction directly tied to the shrinking installed base of PCs, as inexpensive tablets displace the low-end machines used primarily for consumption in mature and developed markets,” said Mikako Kitagawa, Gartner principal analyst.

“In emerging markets, inexpensive tablets have become the first computing device for many people, who at best are deferring the purchase of a PC,” Kitagawa says.

What does Google see in the PC market that others might not? As with Android, Google’s revenue model benefits from increasing the ways Google can steer users to its own apps, devices and operating systems.

Though it might be hard to quantify directly, the more touchpoints Google has, the more places and times it can display ads that underpin its current revenue model. That is the same reason Google has been so proactive in pushing for faster broadband access, lower cost broadband access and ubiquitous access.

In addition to the “always connected” angle, future web apps might act much like launch “native apps” on devices, even when those devices momentarily are not connected.

Chromebook might seem like a distraction. But it is a piece with Google’s support of Android, maps, office suites, YouTube and other apps, devices and operating systems. All of that contributes to creating an ecosystem where the ability to sell ads based on detailed knowledge of people, their behaviors and activities is possible.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Internet Users, Everywhere, are Sophisticated Consumers of Access

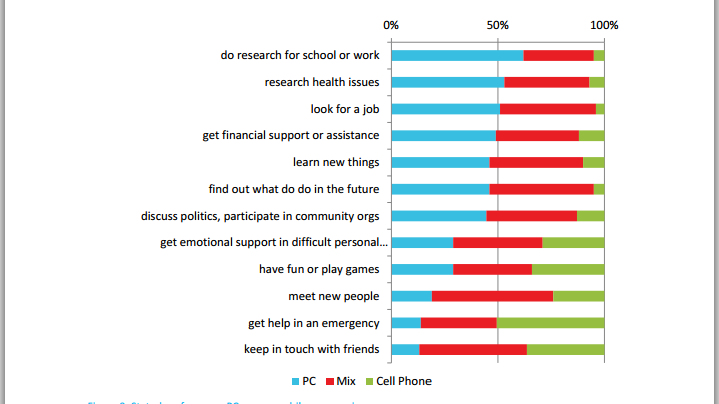

Teenage users in South Africa, for example, use their mobiles and fixed network access in ways that minimize costs, maximize convenience and use the strengths of each method at different times and places.

Among low-income users, free use (such as that in a library) supports resource-intensive content creation or work operations where storage, time, bandwidth and bigger screens are key requirements or at least more conducive to achieving the Internet session goals.

But users avail themselves of their mobiles for Internet access for time-sensitive pursuits, interpersonal communication and low-bandwidth media consumption.

Shared access venues are seen as better for consumption of media and working with large-format documents, while mobile access supports everyday social connections and messaging.

In South Africa, of 8.5 million Internet users in South Africa, 7.9 million accessed the Internet on their phones in 2011, and that 2.48 million of these used only mobile phones for their Internet access.

Also, among a population of 49 million people, ITU estimates suggest there are 725,000 fixed broadband subscriptions, but over 50 million mobile subscriptions.

One possible conclusion is that Internet users, rich or poor, are sophisticated consumers of Internet access services. In developed nations, end users likewise mix use of mobile Internet and fixed network access (Wi-Fi, typically) during the course of a day, in ways that similarly provide value at lower cost.

But it appears cost is not the only dimension upon which consumers are sophisticated.

Internet access speed might be a major reason large number of developing market public access users use shared computing services, even when they also have computers and Internet connections at home, a study suggests.

In other words, people are smart. They use Internet access tools the way they might use other tools, each with a purpose.

In Brazil, home Internet penetration at home among shared venue users was 40 percent, compared with the 24 percent national average. In other words, a significant percentage of people with at-home connections still use shared Internet access centers.

In Chile, 33 percent of public access users had Internet connections at home, as

did about 25 percent of users in Ghana and the Philippines.

Users said “better equipment,” “faster connections,” and availability of “help” were key reasons for using a shared center.

In other words, the Global Impact Study of Public Access to Information & Communication Technologies study suggests users are aware of the benefits of using different access networks and services, in different ways, for different reasons that provide higher value.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Projections of Developing World Internet Adoption are Wrong, as Voice Projections were Wrong

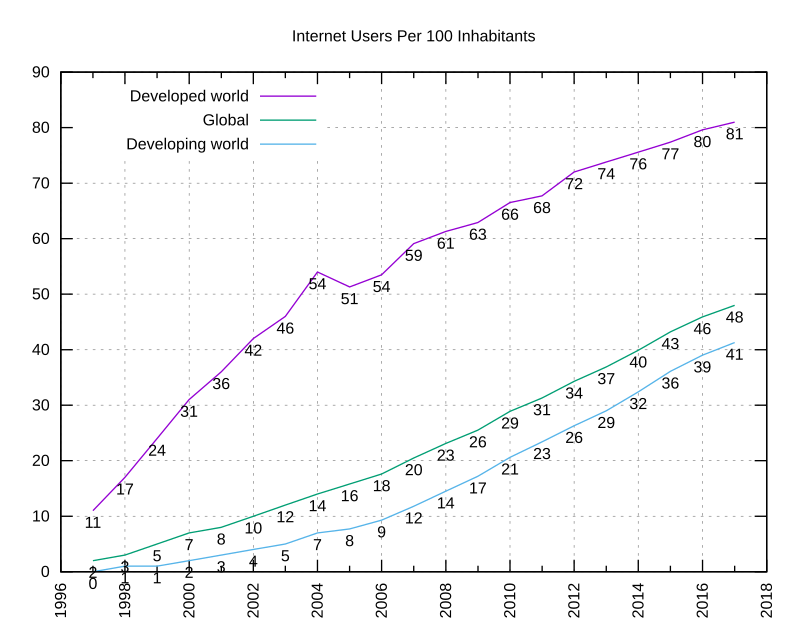

Current projections about developing world use of the Internet generally feature a linear growth pattern. That is a rational way of think about it.

Current projections about developing world use of the Internet generally feature a linear growth pattern. That is a rational way of think about it. But it also is likely to be wrong. Forecasters looking at use of voice communications in the developing world likewise were linear.

But those forecasts were quite wrong. Why they were wrong is a story about deregulation, competition, using "capital-rational" networks and changing consumer perception of value.

Voice communications, provided by mobile networks, became non-linear and exponential over a brief period of not even a decade.

Based on that precedent, one also would predict that Internet adoption in the developed world also will be non-linear. It is hard to predict, as the impact of mobile communications was hard to predict.

But one clear implication is that the massive adoption wave happened only when service providers switched from expensive fixed networks to more-affordable wireless networks. In fact, from 1997 to 2007, world fixed lines were up relatively slightly.

As with voice, mobility and wireless are likely to be the foundations for a similar upsurge of Internet access in developing nations.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Subscribe to:

Posts (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...