Since the late 20th century, U.S. market contestants have argued about the need for regulation of special access services. We are still arguing.

But the U.S. Federal Communications Commission is planning to act, broadening the rules and extending them to cable TV operators and Ethernet services for the first time.

The particulars of the proposed new policy are not yet available. Debate will be vigorous, but Chairman Tom Wheeler has the votes to do what he wants, no matter how many in the marketplace might object.

One reason some competitors and policymakers want stronger regulation of special access services is the claimed advantage incumbent carriers have over most other competitors (other than cable TV companies, which also have ubiquitous networks), in terms of network facilities coverage.

The stated problem: “competitive carriers reaching less than 45 percent of locations where there is demand,” according to FCC Chairman Tom Wheeler.

On the other hand, AT&T has argued that “facilities-based competitors are serving 95 percent of all MSA census blocks (on average, about one seventh of a square mile in an MSA) nationally where there is demand for special access services, and, second, that 99 percent of all business establishments are in those census blocks.”

For the first time ever, the U.S. Federal Communications Commission also is seeking to extend some special access obligations to cable TV networks for the first time.

And some argue that it is impossible to fully do a data-driven analysis because the FCC is not releasing the full results of its earlier survey of facilities, an exercise intended to provide some rationale for assessing the existence of facilities-based competition.

Some might find the emphasis on extending regulation to a declining service curious.

So the issue is application of older rules, shaped in an era of limited competition, to Ethernet access markets that already are largely competitive, and getting more competitive.

“The new approach must be technologically neutral. Rules need to reflect today’s economy and the differences between products, places or customers, and can’t be based on artificial distinctions between companies or technologies,” Wheeler argues.

Some argue new rules, or more-extensive rules are needed in the special access market because a few incumbents still are able to exercise market power to extract higher profits.

The Consumer Federation of America, for example, argues in a study that incumbents have “overcharged” business customers about $75 billion between 2010 and 2015 as a result of market power.

But some argue the reverse case, that ubiquitous networks now mean stranded assets that are a disadvantage in competitive markets, where cable TV and other competitive local exchange carriers have higher profit margins.

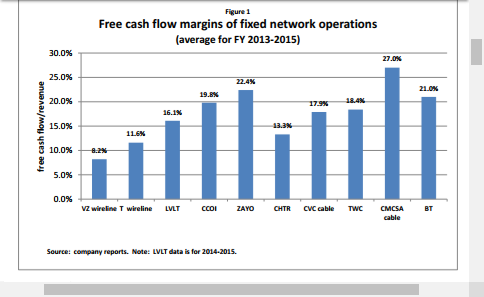

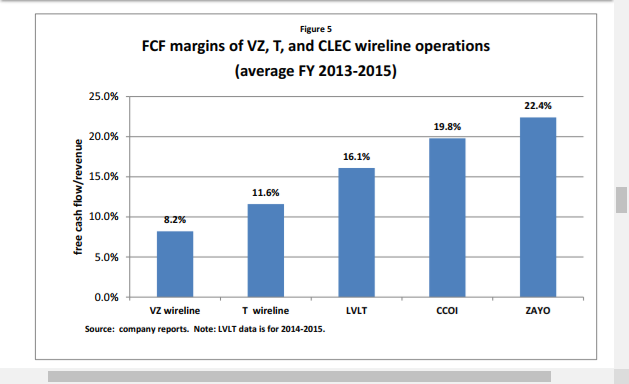

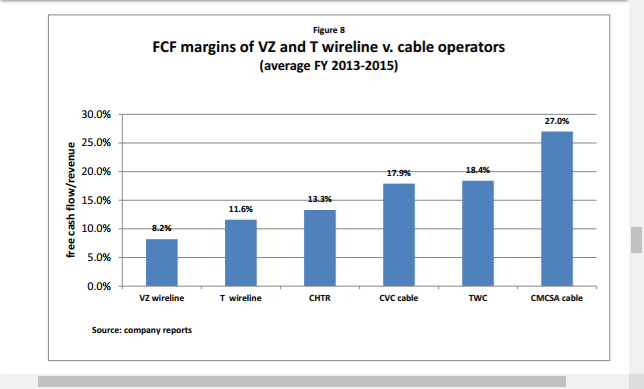

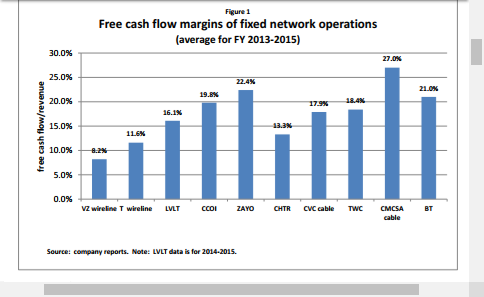

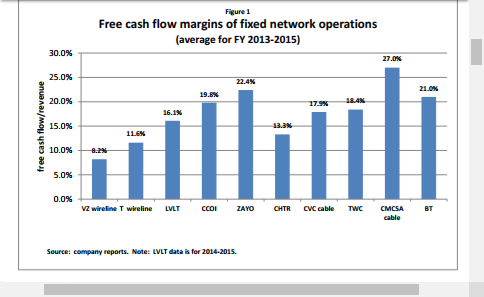

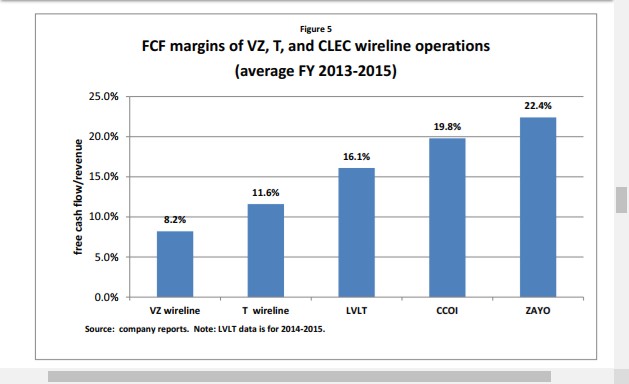

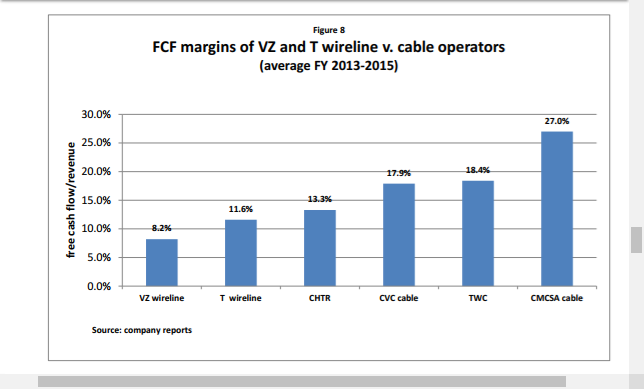

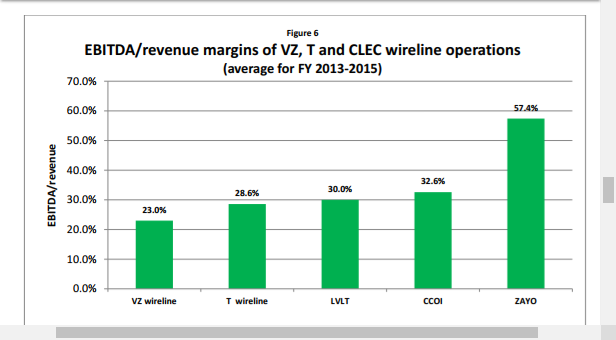

Both the traditional U.S. CLECs and the cable companies who have entered the business broadband market are in good financial health and are generating higher free cash flow than the wireline segments of the largest ILECs, says Anna-Maria Kovacs, Visiting Senior Policy Scholar at the Georgetown Center for Business and Public Policy.

CLECs and cable operators also have higher stock valuations, says Kovacs. Stranded assets, one might argue, are a large part of the problem.

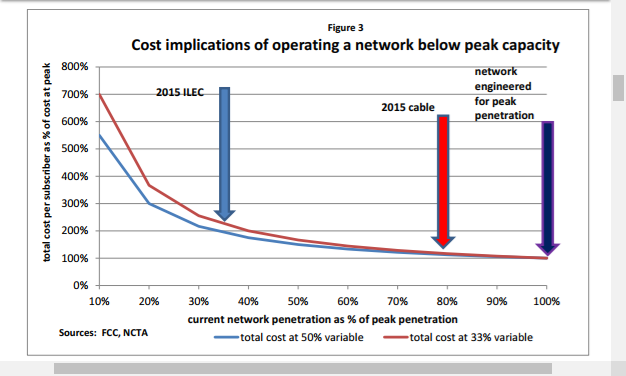

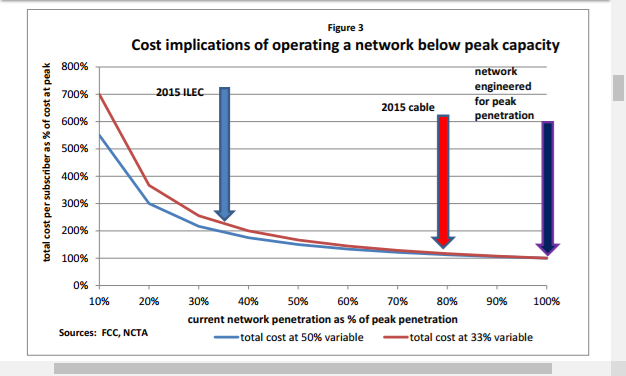

“The ILECs’ low cash flows reflect the continuously increasing cost of sustaining a ubiquitous network that is now serving roughly a third of the lines for which it was engineered,” Kovacs argues. In other words, 66 percent of the deployed network does not actually generate revenue.

Traditional CLECs have focused on the business market exclusively and built out only in areas where high-density makes construction-cost relatively low and attainable-revenue relatively high.

Oddly, the “data provided publicly by U.S. CLECs and cable operators confirms the few facts that have so far emerged from the FCC’s special access data collection, i.e. that there is extensive facilities-based competition in the business broadband market,” Kovacs notes.

Stranded assets are a big business model problem that has become far worse as the number of fixed networks in any market have increased, and as traffic has moved off the fixed networks and onto mobile and other networks.

“At the 2015 ILEC penetration level of 35 percent of peak, total network cost per remaining subscriber has essentially doubled and the networks passed the inflection point beyond which penetration losses result in catastrophic cost increases,” Kovacs notes.

By way of contrast, cable TV networks still are operating in the flat part of the cost curve. That means any cost-per-subscriber increase due to penetration loss is minimal.

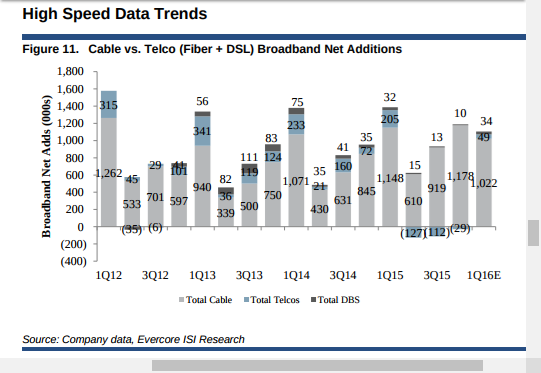

Cable companies also are gaining share in the business communications market. Business revenues constituted roughly 11 percentof the combined revenues of Cablevision, Charter, Comcast, and Time-Warner Cable in 2015.

Their combined $9.5 billion in business revenues were up 42 percent in just two years and MoffettNathanson Research projects that by 2019, cable business revenues will nearly double from their 2014 total.

Some argue the issue is not the existing special access market, but a maneuver by the FCC to extend regulation to more parts of the fast-growing Ethernet services market.

The U.S. Ethernet market grew 20 percent in 2015, according to Kovacs. Gartner Group estimates that enterprise spending over the 2014 to 2019 period on leased lines will decline by 18.6 percent annually.

As a result, leased lines will amount to only $3 billion, or six percent of enterprise spending by 2019.

Legacy packet services will disappear by 2016, and even IP VPN will begin to decline by 2.3 percent annually. Spending on Ethernet services, on the other hand, is estimated to grow by 9.1 percent annually and reach $18.6 billion by 2019.

At the same time, while the prices of TDM-based services are essentially flat, Gartner expects the price of Ethernet access to fall by about nine percent per year over the 2015 to 2018 period.

The price of Ethernet WAN services will drop by about five percent per year over that timeframe.

Substitution of Ethernet for legacy leased lines makes it possible for an enterprise to increase bandwidth while cutting cost.

For example, a 45 Mbps T-3 that costs $1,400 to $2,200 could be replaced by a 100 Mbps Ethernet that costs $850 to $1700.

Savings are even greater at higher bandwidths: a 622 Mbps OC12 that costs $15,000 to $25,000 could be replaced by a 1 Gbps Ethernet that costs $1,500 to $5,200.

Given the combination of savings with greater bandwidth and better performance, it is not surprising that Gartner Group recommends that its enterprise clients replace legacy TDM with Ethernet services