Spectrum assets are fundamental for facilities-based mobile operators, perhaps only interesting for some fixed network operators. That perceived value drives prices buyers are willing to pay for spectrum licenses.

But some mobile operators in some markets apparently place a much-higher value on mid-band spectrum licenses than others.

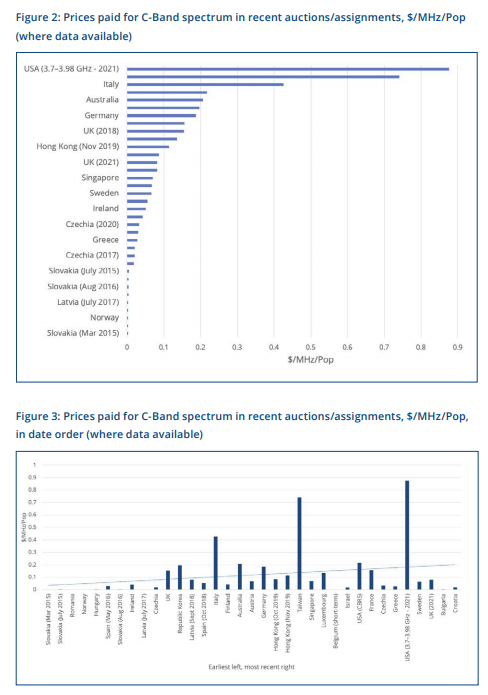

The prices paid for the C-band spectrum have varied widely, according to the Global Mobile Suppliers Association. As with all purchases of any sort, perceived value directly affects prices buyers are willing to pay.

“The amount operators are prepared to spend depends on the degree of competition, the amount of suitable spectrum they already hold, the length of license available, the extent of the coverage/performance requirements that are attached to the license and the economic value of (the amount of money spent by) each mobile end user in the country/territory concerned,” GSA says.

Of the 2021 auctions that GSA has data for, only the U.S. auction achieved a higher than recent average price. It would be a reasonable conclusion that, using the GSA criteria, U.S. mobile operators valued the C-band assets highly.

The U.S. market remains competitive and the amount of mid-band assets for two of three major providers was exceedingly limited. Also, U.S. spectrum licenses are essentially perpetual. Unlike the situation in some other countries, mobile service providers do not have to bid again for their licenses, once awarded.

So the ability to “pay once” creates more perceived value, compared to a “buy every X number of years” regime.

The 2021 US auction of 3.7 GHz to 3.98 GHz spectrum delivered a record high price for C-band spectrum of $0.875/ MHz/Pop, significantly higher than the recent average price of $0.120 per MHz-Pop.

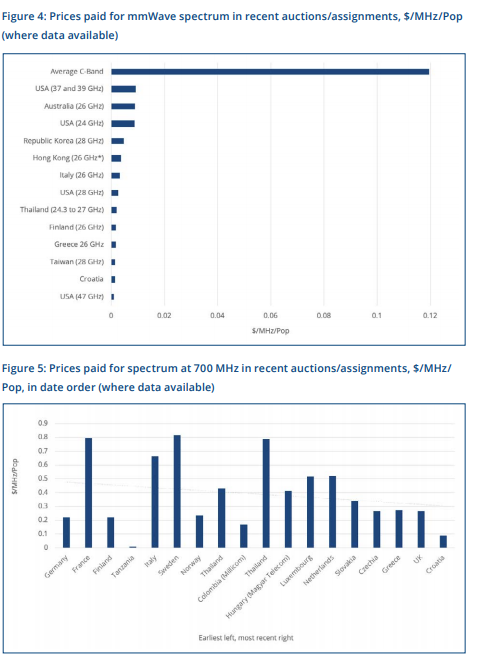

But U.S. mobile operators also place higher value on millimeter wave spectrum, compared to most other countries. Perhaps that is because U.S. operators expect huge increases in end user demand that millimeter wave assets will address.

Mobile operators are expected to run out of capacity in at least half of sites in many parts of the developed world within the next four to five years, as traffic density, particularly in dense urban areas, is expected to steadily increase, McKinsey has forecast.

That is a safe prediction, demand for mobile data always has grown over time.

In fact, the value of 5G is in large part driven by the value to mobile operators who can use it to increase capacity. Mobile data consumption is rising everywhere, meaning mobile operators must plan for extensive investment in capacity.

“More” is the trend in every region. Within a half decade, by some estimates, demand will grow by three to four times current levels. In fact, one good argument for adopting a next generation mobile network about every decade is precisely that doing so helps mobile operators lower their “cost per bit” in an environment where it is very difficult to raise prices enough to cover much-higher usage.

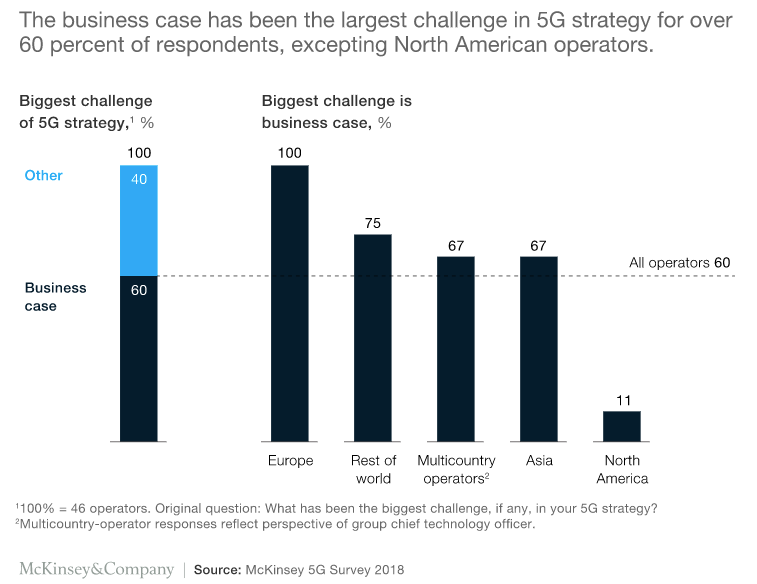

A survey conducted by McKinsey a few years ago showed a disparity in operator attitudes, however. In most regions, return on investment was a big issue. North American mobile operators were significantly less concerned about ROI.

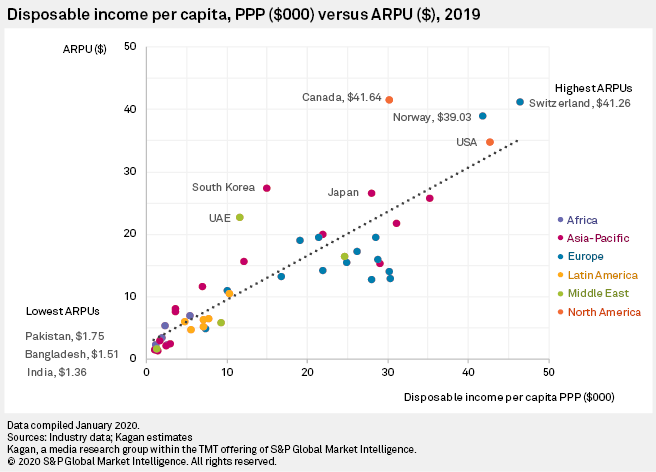

Perhaps the simple reason is that North American average revenue per account and per user is among the highest in the world. Simply, North American mobile operators can expect higher revenue per unit when they invest.

source: S&P Global Market Intelligence