Bharti Airtel, India's largest telecom company by market capitalization and revenues, has entered into an infrastructure sharing deal with the telecom arm of Reliance Industries.

Bharti Airtel, India's largest telecom company by market capitalization and revenues, has entered into an infrastructure sharing deal with the telecom arm of Reliance Industries.

.

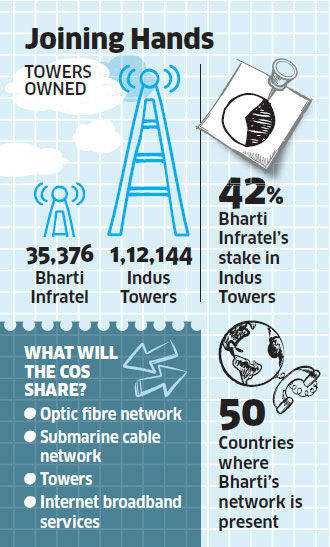

The deal will give Reliance Jio pan-India access to Bharti's nationwide tower and radio infrastructure while giving Bharti access to the optical fiber backhaul capacity created by Jio in the future.

In April of 2013, the two fierce competitors had signed an agreement under which Bharti provided capacity on its i2i submarine cable to Reliance Jio.

The companies said the deal preserves capital and avoids duplication of investment. Bharti will gain lease revenue while Reliance Jio gets to market faster.

Also, Reliance is building a fiber backhaul network at a time when Bharti has only about 10 percent of its tower locations connected by optical fiber.

It has been clear for some time that ownership of mobile cell sites is not necessarily “strategic” for a mobile service provider. Carriers often lease space on towers owned by third parties, sharing those sites with rivals.

In India and some markets in Africa, mobile service providers have agreed to share the cost of tower facilities. Some service providers outsource actual operations of their radio networks as well.

So it isn’t unusual anymore for a group of mobile operators to agree they will share tower site passive elements.

In another such example, mobile carriers Cellcom Israel Ltd., Pelephone Communications Ltd., and Golan Telecom Ltd. have agreed to build and operate a shared Long Term Evolution fourth generation radio network.

Cellcom and Pelephone also signed an agreement for the sharing of passive elements of cell sites for existing networks and an Indefeasible Right of Use (IRU) agreement with Golan Telecom for Cellcom's 2G and 3G networks.

The infrastructure sharing also might save Cellcom and Partner Communications as much as $57 million a year, according to an estimate of the brokerage unit of Ramat-Gan, Israel-based Excellence Nessuah Investment House.

What might be more unusual is cooperation in obtaining spectrum for the 4G network. Though the language is open to interpretation, and the sharing deals might require regulatory approval, it also appears the consortium will attempt to acquire common 4G spectrum as well.

That would be unprecedented, if it happens.

So the longer term issue is what else some mobile service providers might in the future decide is “strategic,” and must be owned, and what is increasingly tactical, and can be shared or outsourced.

Granted, spectrum is essential for a mobile operator. But it is not clear sole ownership of such spectrum is necessary. Under some conditions, mobile service providers might be better off reducing investment risk by jointly securing necessary spectrum.

That would a historically rather unprecedented development, but is possibly no different, in principle, from the practice of sharing backhaul, towers or radio infrastructure, or outsourcing the network operations and maintenance.

But such moves also would illustrate that the “unique core competence” for a mobile service provider might not necessarily lie in the actual full ownership of access assets, including spectrum.

No comments:

Post a Comment