Most observers sense an inflection point for streaming video has been reached. Most observers would agree that potentially large shifts of revenue, market share, profit margins and market size are possible, as the transition gains momentum.

That perhaps is the counterpoint to trends showing that ESPN, for example, has lost subscribers over the last year; some 3.2 million accounts, leaving a current base of about 93 million households.

That matters for Disney since ESPN is expected to make up 25 percent of Disney’s total profit in 2015.

But who the winners and losers are, and how much they stand to gain or lose, is a big question.

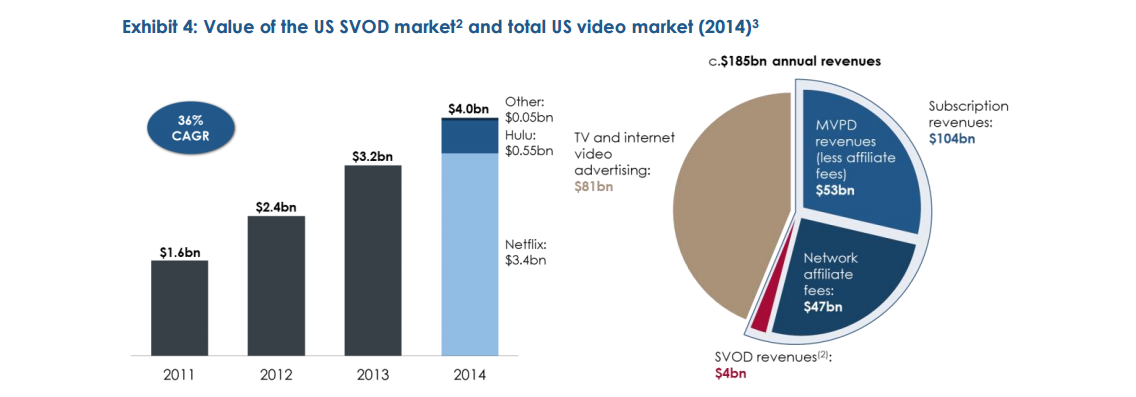

Less contentious is the idea that streaming revenues are about to grow rapidly. Premium OTT revenues are expected to grow from $4 billion in 2014 to between $8 billion and $12 billion in 2018, with Netflix remaining the largest single mass-market provider, according to industry executives polled by MTM on behalf of In May 2015, Ooyala and Vindicia.

Beyond that, there is great uncertainty. Industry participant say it is difficult to determine which services will be successful. There also is a general expectation that the mass market will remain dominated by a small number of major service providers.

There was a strong consensus that Netflix will remain the largest single subscription OTT video provider in the United States (a reasonable and likely safe prediction).

But many expect Netflix market share to dip from the 85 percent market share Netflix held in 2014 to around 50 percent market share in 2018.

The issue is how many other significant providers can exist. A common thought is that the number will be few, for any number of reasons, including the time and expense of aggregating a critical mass of content.

Most industry participants believe that the market will continue to be dominated by a small number of major OTT service providers, most likely the existing incumbents with established subscriber bases and strong positions in the market.

The reason is that the main barriers to entry for new entrants are believed to be access to large volumes of differentiating, exclusive premium film and TV content, an ability to attract new customers, and an ability to sustain substantial investment over time. The leading linear distributors have all that.

In that view, today’s major linear video providers have the inside track. They have the financial assets, content and customer relationships, distribution economies and brand names to succeed in what is expected to be a highly-competitive and expensive business.

Also, as the market becomes more crowded and competitive, new entrants will find it increasingly difficult to differentiate their services from the market leaders. Fundamentally, streaming or linear businesses are about unique content.

Most industry participants believe that developing a critical mass of premium content with mass-market appeal, such as original content or early-window film and TV content, is now harder.

Existing content libraries have largely been licensed and the cost of new premium content is growing as well.

With increased competition, premium content costs additionally are widely believed to be rising.

Upstarts will have to spend heavily to catch up. And many studios are locked into long-term content deals, making it harder to quickly license a critical mass of attractive content.

But integration, multi-platform client development and high-quality user interfaces also are essential.

Just the task of acquiring and creating unique content will be expensive, time-consuming and difficult, especially for later entrants.

Even price differentiation--a common and effective positioning--will be difficult, given the low price at which Netflix sells.

The issue is whether today’s leaders can manage the new business without simultaneously destroying the legacy business.

On the other hand, Niche services, perhaps as many as 15 to 20 entities in total, each will have an opportunity to acquire audiences of 100,000 or more paying subscribers by 2018, with many more attracting smaller numbers of subscribers.

Those services, in other words, will not scale.

Logical candidates in the niche segment are services selling into existing fan bases. Many of these services are likely to be bundled with wider subscription or membership offerings and marketed and retailed through third-party distribution platforms.

Some of the potential categories reflect the similar niche audiences in linear TV: sports, kids, anime, foreign drama, expat and ethnic services (e.g. Korean, Hispanic) and personality-based offerings (music, performing arts).

Still, the economics of niche services are likely to remain challenging. Profit margins will be relatively low, while technology, content and marketing costs will tend to be relatively high.

The study aimed to ascertain prospects for streaming video subscription services in the United States, as seen by industry executives in the business.

As multiple new OTT services launch in 2015 and 2016, industry participants believe that content

No comments:

Post a Comment